KEY POINTS

- 4Q14 LOOKED MUCH BETTER: Outside of the sputtering MAU growth metrics, we saw some marginal improvement across the metrics that were concerning us the most. TWTR is not out of the woods by any stretch, but it doesn’t appear to be getting worse.

- AND MANAGEMENT PLAYED IT PERFECTLY: Management explained away the MAU weakness, while pointing to a positive inflection 1Q15. Management also managed consensus expectations by explicitly quantifying its non-recurring 2014 tailwinds (e.g. World Cup).

- SHORT MAY BE PLAYED OUT, BUT TREAD CAREFULLY: We still do not believe TWTR can hit 2015 estimates without M&A support, and the additional $1.8B raise suggests that may be the plan. But without a hard catalyst in site, it may be time to walk away from this one. We'll be monitoring consensus estimates, and reassessing our position from here.

4Q14 LOOKED MUCH BETTER

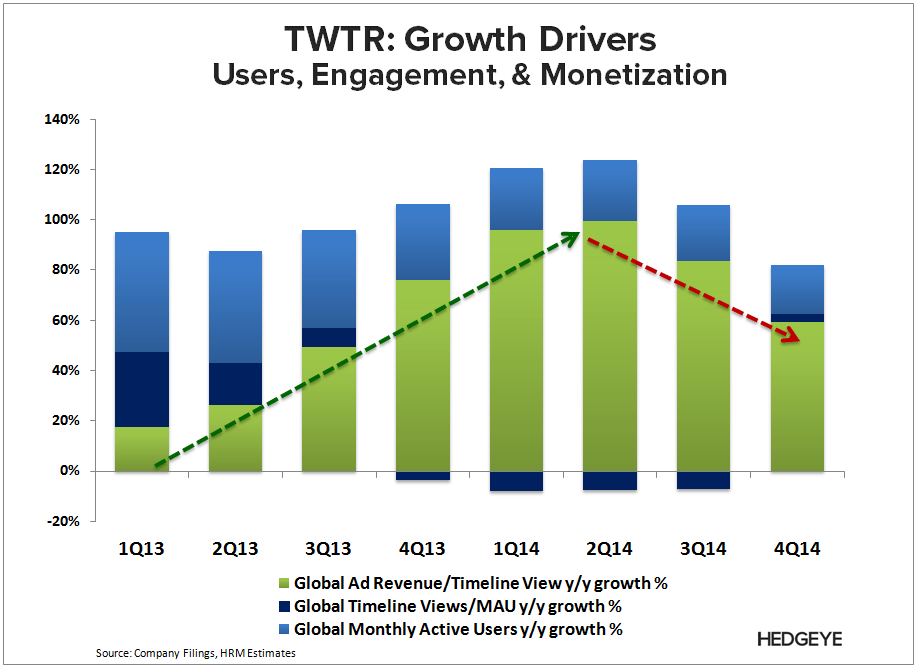

The biggest blemish from the quarter was the lack of US user growth. Outside of that we did see some marginal improvement in some of the key metrics that we concerning us the most.

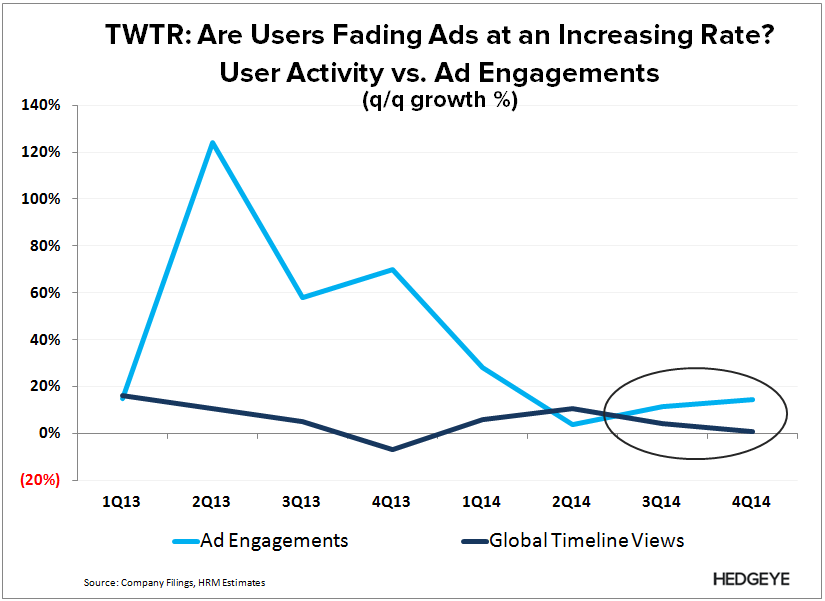

We also saw a widening spread between ad engagements and timeline views, which suggests improved targeting ability or increased ad load (management suggests both). We also saw both ad engagements and pricing both accelerate on a sequential basis (at the same time) for the first time in TWTR’s reported history; suggesting that TWTR may not be as dependent on surging ad load to drive its model (at least this quarter).

AND MANAGEMENT PLAYED IT PERFECTLY

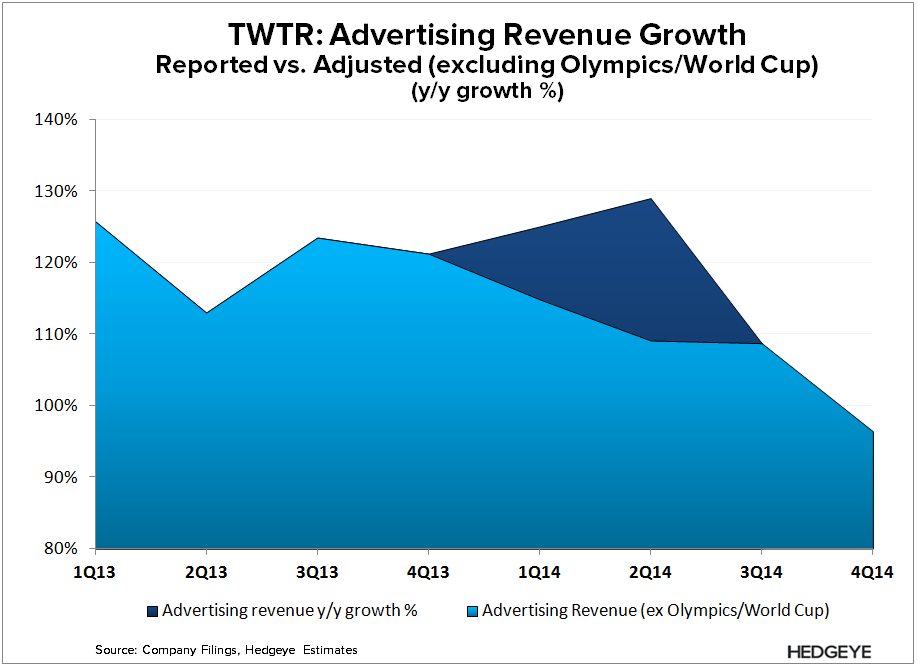

The MAU weakness was explained away by pointing to the iOS 8 integration that essentially cut third-party MAU metrics by 4M, while at the same time, pointing to a positive inflection in MAU metrics in 2Q15 to-date. Further, management approached 2015 guidance by quantifying the non-recurring tailwinds in 2014 (e.g. the World Cup essentially doubled its sequential revenue growth rate in 2Q14).

SHORT MAY BE PLAYED OUT, BUT TREAD CAREFULLY

Management essentially guided inline, with revenues at the midpoint of $2.33B vs. consensus of 2.30B. We were expecting $2.17B, and really haven't seen much to dissuade us form our estimates.

Despite the marginal improvement we highlighted above, TWTR still really hasn't shown us much to suggest that it's found an answer to comping past the 2Q13 Supply Shock; especially since we now realize how much of its 1H14 ad revenues were juiced by one-time events

However, the big variable is M&A. TWTR essentially doubled its cash balance after raising an additional $1.8B last quarter. With $3.6B in cash, mgmt attempt to fill the void inorganically. We're not sure the street will be willing to pay up for that (e.g. its 3Q14 release).

But without a hard catalyst in site, it may be time to walk away from this one. We'll be monitoring consensus estimates, and reassessing our position from here.

Let us know if you have any questions, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet