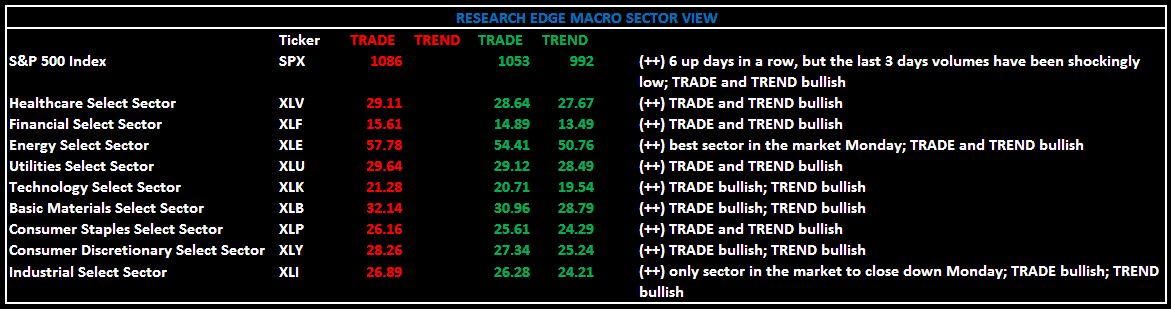

On Monday, the S&P 500 closed at 1,077, up 0.4% on the day; day six of the S&P 500’s rally, but the last three the volumes have been shockingly low. The six day rally is the longest streak since June 2007. The market attention has shifted squarely to a few earnings releases due out over the next few days. In Healthcare and Technology, JNJ, ALTR and INTC all report today. Other notable companies reporting today are DPZ and CSX. .

Friday’s portfolio activity included shorting more USO and covering our short in AZO. Yesterday, WTIC Oil was trading just north of our overbought line. With the US Dollar hitting another higher-low this morning, we are shorting more of oil's curve.

Yesterday’s market action was another “Outside Reversal” (See Keith McCullough note “Another outside Reversal”). An Outside Reversal is an intraday breakout to new YTD highs, followed by an intraday reversal (selloff), and a market closing price that sits below the prior YTD closing high. After we saw the Outside Reversal in the S&P500 a few weeks back, the index corrected by over 4% in the days that followed that reversal.

The dollar index was down 0.2% in very quiet trading. The VIX has declined for the sixth (0.5%) straight day and is now down 14% over the past week.

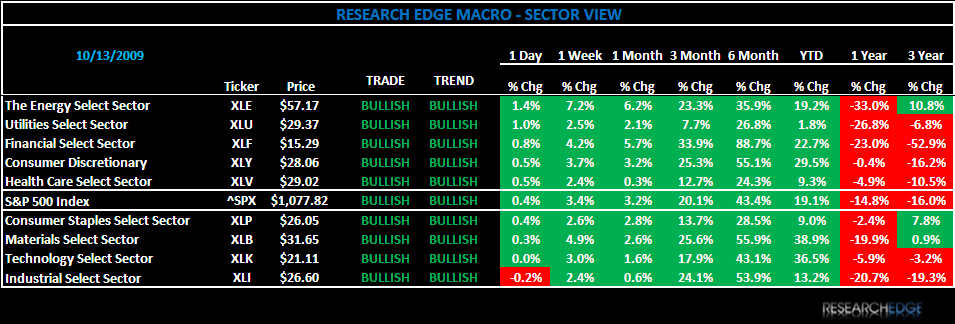

On Monday, five of the nine sectors outperformed the S&P 500, with every sector positive except the Industrials (XLI). Within the XLI, Ryder (R) climbed 9.9% after the company said it would pay a cash dividend of $0.25, while the Aerospace and Defense names were notable weak on the day.

The three best performing sectors were Energy (XLV), Utilities (XLU) and Financials (XLF), while Industrials (XLI), Materials (XLB) and Technology (XLK) were the bottom three. We are currently long the XLV.

Today, the set up for the S&P 500 is: TRADE (1,053) and TREND is positive (992). Day 2 of perfection - the Research Edge quantitative models have 9 of 9 sectors in the S&P500 positive on TREND and 9 of 9 sectors are positive from the TRADE duration.

Equity futures are currently trading mixed with the S&P 500 trading 1.25 points below fair value; NASDAQ trading in line to fair value and the DJIA trading 12.52 points above fair value.

Howard Penney

Managing Director