KEY POINTS

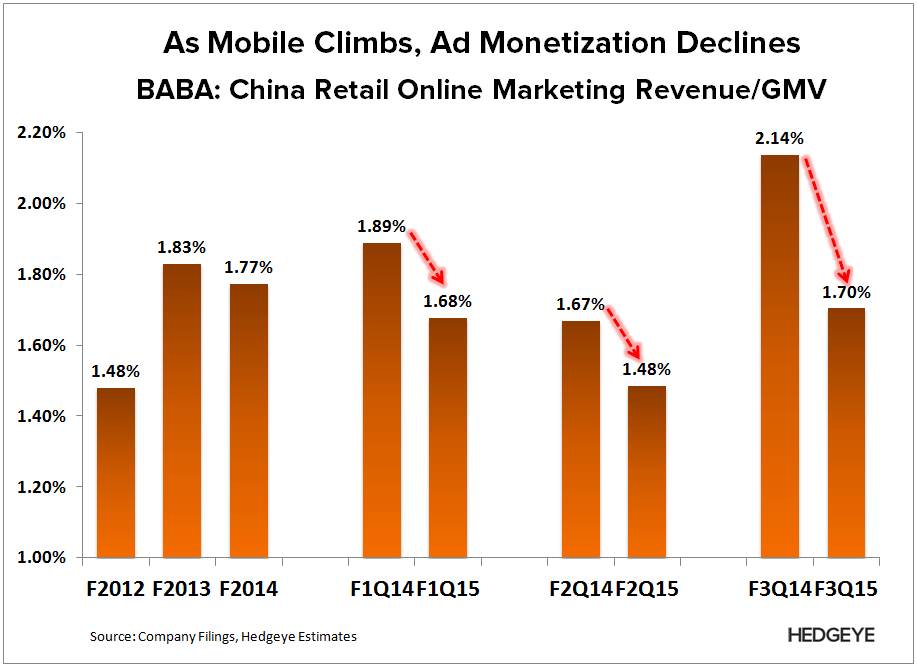

- The Mobile Hammer: BABA's mobile GMV percentage experienced its sharpest y/y growth in its reported history. In turn, BABA's ad monetization rates got hammered, and its y/y revenue growth in its core marketing segment decelerated precipitously to 19% vs. 32% in the prior quarter. There will be a lot of sell-side noise about mobile being a long-term opportunity. It's not, it's a secular headwind.

- The Tmall Nail (in the Coffin): The key metric that we were keying in on, and the only thing that was keeping us on the sidelines on the short side was growing Tmall GMV mix shift, which had been propelling Commission revenue growth well in excess of GMV growth. That sputtered out this quarter, suggesting Tmall mix shift is no longer a secular tailwind, which means its growth prospects are now more dependent on its GMV, which is where we are decidedly bearish.

THE MOBILE HAMMER

BABA's mobile GMV percentage experienced its sharpest y/y growth in its reported history. In turn, BABA's ad monetization rate (GMV take-rate) got hammered on a y/y basis, and estimated y/y growth on its core marketing segment decelerated precipitously to 19% vs. 32% in the prior quarter.

So why is mobile a headwind? BABA’s ad prices are determined through on online auction platform, which means its vendors set the price. Vendors are not willing to pay comparable rates for mobile ad clicks as they are for desktop clicks.

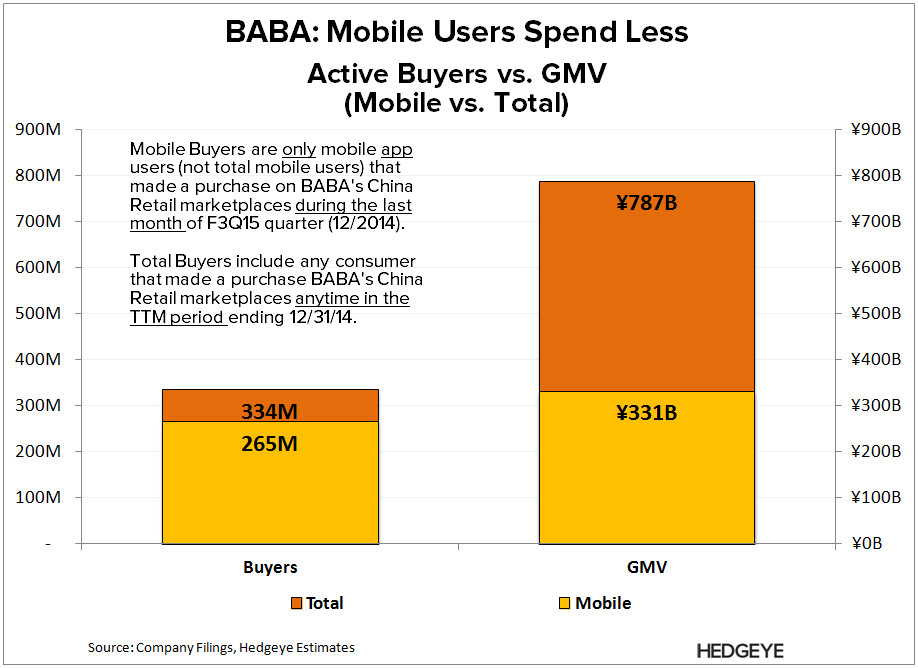

We suspect the reason why mobile ad rates are lower is because vendors are getting a lower ROI on that ad spend, likely mobile is how China's less affluent access the internet access, and those consumers must be inherently more selective with their purchases. BABA's own metric suggest as much, with mobile representing the majority of buyers, but the minority of GMV

Moving forward, BABA's next wave of user growth will come from a less-affluent consumer, meaning the pricing pressure across its core marketing segments will only get worse. So while there will be some sell-side noise touting mobile as a long-term opportunity, it's because they don't understand who that mobile consumer is. Mobile is not an opportunity, it's a secular headwind. See notes below for more detail.

BABA: Model Facing Secular Pressure

12/04/14 09:17 AM EST

BABA: What the Street is Missing

11/26/14 08:03 AM EST

THE TMALL NAIL (IN THE COFFIN)

The key metric that we were keying in on this quarter was Tmall GMV mix shift, which had been propelling Commission revenue growth well in excess of GMV growth.

The reason is that BABA charges commissions on Tmall transactions, so if a greater percentage of GMV flows to Tmall, BABA has more GMV to tax. In turn, even if BABA's core marketing segment is under pressure, commission revenues could compensate alongside growing Tmall mix. That is what has kept us on the sidelines on the short side.

However, that sputtered out this quarter. Tmall GMV mix only increased by 2.6 percentage points y/y vs. its historical tend of 5+ percentage point. In turn, commission revenue growth slowed precipitously, exposing the weakness in BABA's core marketing segment.

In short, we don't see Tmall Mix Shift as long-term secular tailwind. That means BABA's growth prospects are now even more dependent on its GMV, which is where we are decidedly bearish.

Let us know if you have any question, or would like to discuss in more detail.

Hesham Shaaban, CFA

@HedgeyeInternet