After a few cold weeks in the Northeast, we’re thinking about warmer places.

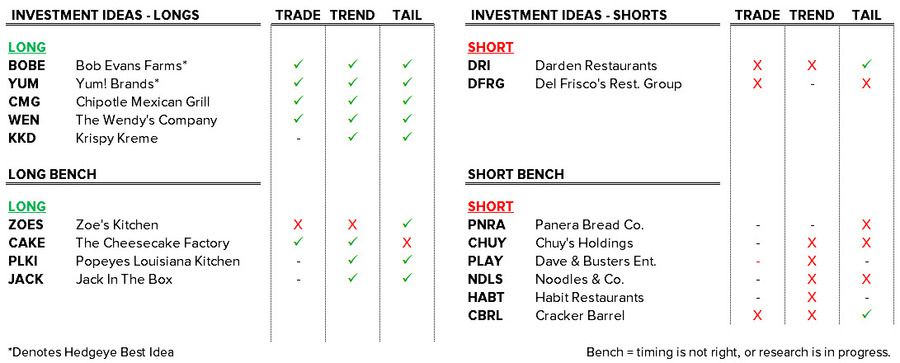

Following Brinker’s earnings release this morning, we decided to make two changes to our Investment Ideas list.

- Remove BLMN from the Long List

- Bump up DFRG to the Short List

Inflation is the common theme for both of these names. Red meat inflation, in particular, is the one commodity we believe will limit upside to earnings – despite strong sales trends. On the EAT call, management cited “unfavorable commodity pricing stemming from a greater than anticipated increase in the price of burger meat, cheese and avocados,” as a significant headwind to EPS during the quarter. We suspect that won't change anytime soon. Next quarter, EAT will be rolling a difficult comp, when cost of sales were down 93 bps y/y in 3Q14.

BLMN: All Good Things Must Come to an End

BLMN has enjoyed a nice run since the end September of last year, when we added it to our Long List. The stock is up 6% and 31% over the past one and three months, respectively. Unfortunately, we believe the stock has a lot of good news baked into it ahead of the quarter. Given the recent stock move and earnings estimates that have remained flat, the stock is finally trading in-line with the group. If we thought there was significant upside to earnings, we’d stay long the name – but we don’t believe that to be the case. There has never been a significant amount of leverage in the BLMN business model, which has traditionally relied on pricing and productivity, to offset commodity inflation, to protect margins. In addition to the aforementioned, the overwhelmingly positive sentiment gives us incremental cause for concern.

Recent Notes

11/04/14 BLMN: Notable Progress, Still Bullish

10/02/14 BLMN: Bullish on Bloomin’

09/25/14 BLMN: Same As It Ever Was

Source: FactSet

DFRG: Hello Darkness, My Old Friend

The bottom line on DFRG is a little more sinister, because the business model is broken. In our view, DFRG should not open another Del Frisco’s Grille for the foreseeable future – never mind six this year! Please refer to the Black Book we published back in July 2014 for additional details. Perhaps more importantly, however, is the fact that the company will not grow EPS 17% in 2015 and it certainly won’t accelerate to 23% in FY16.

Trading at 20x an inflated NTM EPS estimate, the stock looks like a good value. Alas, consensus reflects a recovery that will not happen. The optimism in DFRG’s earnings estimates is a direct reflection of the 100% buy rating on the stock. The target price of $27.60 suggests 37% upside from current levels. If we set price targets here at Hedgeye (we don't), ours would be closer to $10 (~50% downside).

Recent Notes

10/16/14 DFRG: Timing is Critical

10/09/14 DFRG, EAT: Covering Our Shorts Given Strong Knapp Sales

07/22/14 DFRG: Inflated Multiple Deflating

07/21/14 DFRG: Thoughts into the Print

07/02/14 DFRG: A Castle-in-the-Air

06/16/14 DFRG: Running Through Our Thesis

06/05/14 New Best Idea: Short DFRG