Below is the detailed breakdown of this morning's initial claims data from Joshua Steiner and the Hedgeye Financials team. If you would like to setup a call with Josh or Jonathan or trial their research, please contact

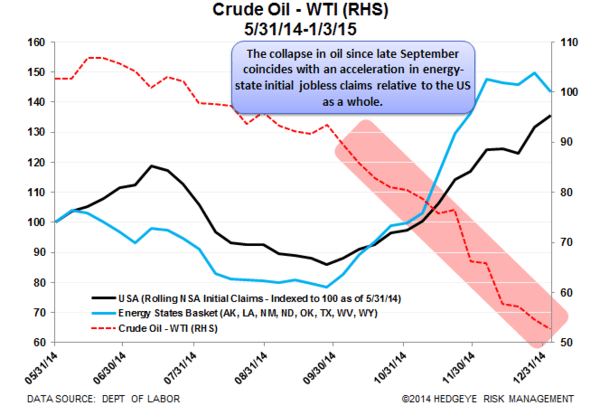

EYEING THE ENERGY STATES: The principal risk to the labor market's otherwise healthy disposition is the potential hit to energy-sector jobs from the collapse in energy prices. In an effort to stay vigilant and monitor the situation, we've been tracking weekly state-level filings for the eight energy-heavy US states relative the country as a whole. Those states include AK, LA, NM, ND, OK, TX, WV, WY and further details on them can be found here: Link.

What we've observed is that energy state initial claims are diverging from the country as a whole since the fall in oil prices began in earnest in late September last year. The first chart below illustrates. The black line represents US initial jobless claims, while the blue line represents the eight energy-heavy states (indexed into a basket). These are NSA claims so we’re interested in the divergence between the two series.

The Data

Prior to revision, initial jobless claims rose 22k to 316k from 294k WoW, as the prior week's number was revised up by 3k to 297k.

The headline (unrevised) number shows claims were higher by 19k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 6.75k WoW to 298k.

The 4-week rolling average of NSA claims, another way of evaluating the data, was -10.9% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -16.2%

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT