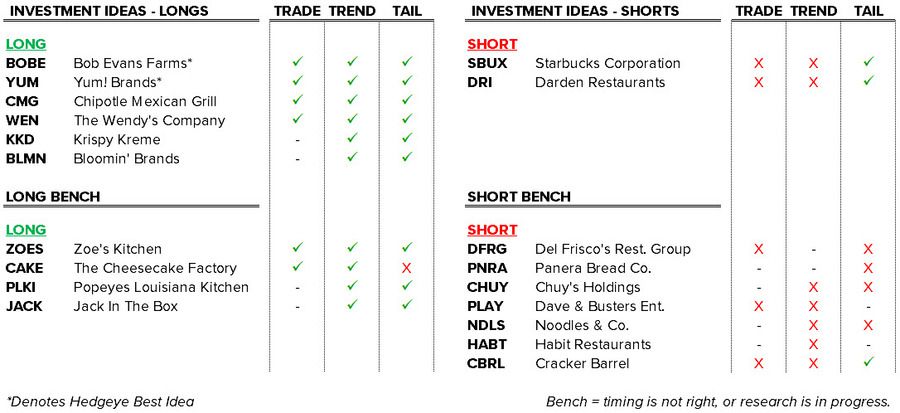

We made several changes to our Investment Ideas this week. In the coming weeks, we will be outlining these changes in more detail.

Perhaps the two most notable moves are the relegation of JACK and PLKI from the Long List to the Long Bench. We like both names longer-term, but believe the impressive recent outperformance means the street is beginning to understand the long thesis and incremental good news is likely baked-in.

We’ve also expanded our Short Bench with the addition of several casual dining names. We’re looking to get aggressive on the short side, after we roll easy comps, as we head into the spring.

recent notes

01/05/15 Monday Mashup: BWLD, SBUX and More

01/08/15 SBUX: Why We Think It’s a Short

01/08/15 Knapp Headlines Strong, But…

01/09/15 SBUX: Part of the Story is Going Untold

Events This Week

Monday, January 12th

- ICR XChange Conference: JACK, KKD, DNKN, DFRG, BBRG, FRSH, ZOES, PLKI, LOCO, SONC, FRGI, CBRL, GTIM

Tuesday, January 13th

- ICR XChange Conference: KONA, RRGB, JMBA, DENN, NDLS, HABT, DPZ, TAST, RUTH

Wednesday, January 14th

- DPZ Investor Day

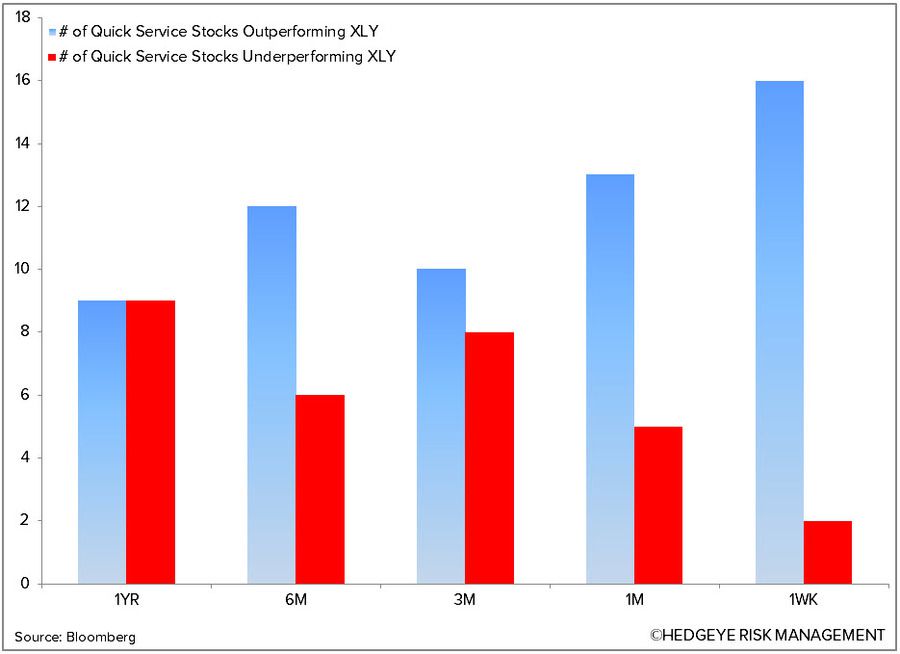

Chart of the Day

Recent News Flow

Monday, January 5th

- BOBE upgraded to buy at Janney Capital with a $60 PT.

- DPZ upgraded to buy at Janney Capital with a $110 PT.

- LOCO upgraded to outperform at RW Baird with a $34 PT.

- PBPB upgraded to outperform at RW Baird with a $17 PT.

- BWLD PT increased to $205 from $180 at UBS.

- BWLD downgraded to neutral at RW Baird with a $180 PT.

- SBUX downgraded to neutral at Janney Capital with an $85 PT.

- LOCO announced an extension of its Under 500 line with four new menu items, each under 500 calories. The new offerings include the Chicken & Shrimp Grilled Tostada, Double Chicken Wet Burrito, Grilled Chicken & Kale Salad, and Skinny Chicken Quesadilla.

- DFRG opened its newest Del Frisco’s Grille in Pasadena, CA. The restaurant spans more than 7,000 square feet and can entertain about 200 people between both indoor and outdoor seating.

Tuesday, January 6th

- LOCO announced the opening of three new franchised locations in California (Victorvile, Stockton, and Santa Paula) and one new franchised location in Nevada (Reno).

- DIN Applebee’s introduced its new Pub Diet menu which features fiber and protein rich dishes with less than 600 calories. The menu includes four dishes starting at $9.99: Pepper-Crusted Sirloin & Whole Grains, Cedar Grilled Lemon Chicken, Shrimp & Broccoli Cavatappi, and Savory Cedar Salmon.

- DNKN announced its intention to replace its senior secured credit facility with a new securitized financing facility, expected to be comprised of $2.3 billion of senior fixed-rate term notes and $100 million of variable funding notes.

Wednesday, January 7th

- FRGI announced the promotion of three of its top executives. CFO Lynn Schweinfurth was promoted to senior vice president, Chief Counsel Joseph Zirkman was promoted to senior vice president, and Chief Development Officer John Todd was promoted to vice president.

Thursday, January 8th

- DNKN announced expansion plans in China with the signing of a development agreement that calls for the development of more than 1,400 restaurants across China over the next 20 years as part of a joint venture between Jollibee Worldwide Pte Ltd. and Jasmine Asset Holding Ltd.

- LOCO celebrated the grand opening of its newest location in Goodyear, Arizona – its 19th restaurant in the state. The 3,000 square foot restaurant has room for 62 guests.

- SBUX announced COO Troy Alstead will take a leave from the company, effective March 1st. The company will provide detail on transition plans during the company Q1 earnings call on January 22, 2015.

Sector Performance

XLY Quantitative Setup

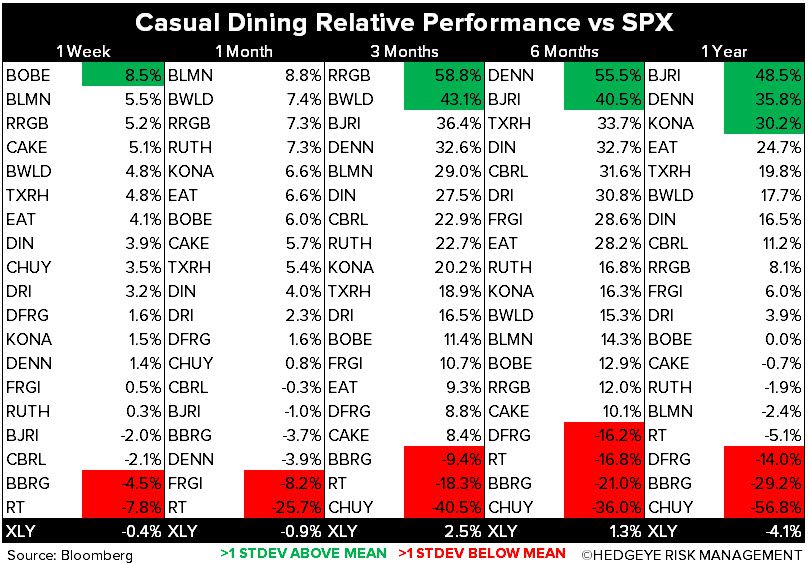

Casual Dining Restaurants

Quick Service Restaurants