This note was originally published at 8am on December 26, 2014 for Hedgeye subscribers.

“I’ve seen George Foreman shadow boxing, and the shadow won.”

-Muhammad Ali

Traditionally observed by Commonwealth Nations like my homeland, today is Boxing Day.

Much to Muhhamad Ali’s chagrin, today has nothing to do with him beating up on Foreman or Frazier. It used to be the day when British servants received gifts from their overlords in a “Christmas Box.”

Now, barring any central plan you might receive from upon high, it’s just another day off for Canadians to drink beers and watch the World Junior Hockey tournament (which is being held in Toronto and Montreal this year).

Back to the Global Macro Grind…

Although its economy is getting speed-bagged, Japan doesn’t do Boxing Day. That said, their bureaucrats love central planning. In a holiday message to the people he is plundering via currency debasement, this is what the Prime Minister, Shinzo Abe, had to say:

“I want companies with high profits that are benefiting from the weak yen to raise wages, investment, and on top of that, consider the prices they pay their suppliers…”

Isn’t that just great – thanks for the pep talk, Shinzo.

In other news, the people of Japan don’t want to do what Abe is telling them to do. Not to be confused with the Policy To Inflate the Weimar Nikkei’s last price, here’s what’s cooking in Japan, economically:

1. As the Yen burns, Japanese Consumer Prices (CPI) are +2.7% year-over-year

2. But Japanese Household Spending (in Burning Yen Terms) is down -2.5% year-over-year

3. And the Savings Rate of the Japanese people just went negative alongside real wage growth

I know, this is all progressing so very well…

But as long as the Nikkei (which, by the way, we’ve been suggesting you be long, while short Yens vs USD) is up, the financial media that panders to central-planning-access is going to tell you that this Abenomics thing could actually work.

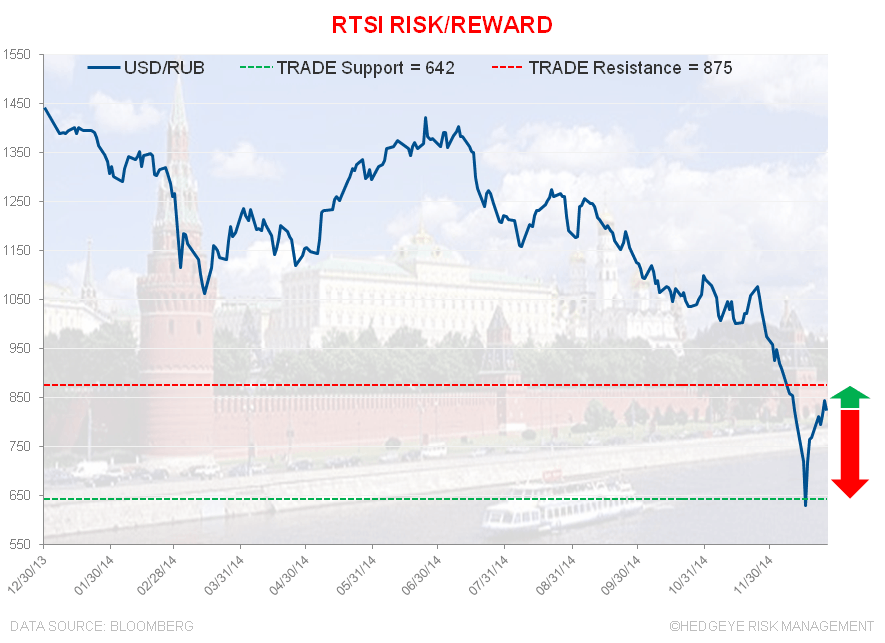

In other Global Macro news, other than getting to play Denmark in the 1st round of the 2015 IIHF World Junior Hockey Championship today, things for Russia still suck.

Despite “bouncing” off its lows, the Russian Trading System Index is:

1. Down -38.4% for 2014 YTD

2. And would only have to be +63% (from here) to get whoever “allocated assets” to it a year ago back to breakeven

3. With an immediate-term risk range of 642-875

In other words, with the RTSI (Russian Stock Market) currently trading at 847:

1. It has immediate-term upside of +3%

2. And immediate-term downside of -24%

#sweet

And so is worldwide #GrowthSlowing + #deflation risk, right? Maybe if you’re shadow boxing USA style with year-end performance chasing, or something like that. But I wouldn’t confuse that with trending global macroeconomic gravity.

Our immediate-term Global Macro Risk Ranges are now (I’ve added the our intermediate-term TREND view in brackets – you can get our Top 12 macro ranges and TREND views in our Daily Trading Range product):

UST 10yr 2.03-2.30% (bearish = bullish Long Bond)

SPX 1956-2110 (bullish)

RUT 1125-1220 (neutral)

Nikkei 17261-17995 (bullish)

VIX 12.95-24.11 (bullish)

USD 89.26-90.89 (bullish)

EUR/USD 1.21-1.23 (bearish)

YEN 118.23-121.11 (bearish)

Oil (WTI) 54.08-57.99 (bearish)

Nat Gas 2.91-3.47 (bearish)

Gold 1161-1197 (bearish)

Copper 2.83-2.93 (bearish)

Happy Holidays – best of luck and health to you and your families,

KM

Keith R. McCullough

Chief Executive Officer