This note was originally published at 8am on December 24, 2014 for Hedgeye subscribers.

“Twas the night before Christmas, when all through the house

Not a creature was stirring, not even a mouse;

The stockings were hung by the chimney with care,

In hopes that St. Nicholas would soon be there.”

-Major Henry Livingston Jr.

Whether you celebrate Christmas or not, undoubtedly many of you are familiar with the poem “Twas The Night Before Christmas”. It is the classic story of children waiting for the mythological character Santa Claus to show up on Christmas Eve.

A side note on this poem is that there is some serious controversy surrounding the author. The poem was originally published anonymously in 1823, but then attributed to Clement Clarke Moore, who acknowledged authorship in 1837.

A graduate of Columbia University, Moore was an interesting character. Among other things, his father officiated at the inauguration of George Washington, he was opposed to the abolition of slavery, he was also a vocal opponent to Thomas Jefferson for mostly religious reasons, and, ironically enough, founded the Chelsea area of New York City.

Despite claiming authorship, Professor Donald Foster of Vassar, who is considered of the top forensic linguists in the world, has concluded quite definitely that true author was Henry Livingston, Jr. Livingston was also a New Yorker, though primarily a gentleman farmer as opposed to being a political and religious activist, and wrote the poem for his seven children.

Admittedly, this story of disputed authorship, jolly men in suits bringing presents and a red nosed flying rein deer leading the way, remind us a little of the global stock markets. On Nasdaq, on Dow, on Yen and on Ruble ! (Ok, not on Ruble.)

Back to the Global Macro Grind...

Yesterday, the market mildly cheered on not the arrival of St. Nicholas, due to a meaningful upward revision in GDP for Q3. The most prominent area of revision from the initial GDP estimate was a +0.70% increase in consumption to +3.2% from last quarter. But across the board, the other key components were revised higher as well.

The challenge with GDP for stock market operators, of course, is that it is often rightfully considered a lagging indicator. Case in point is that we are just now getting the final GDP number for Q3 when we are seven days before the end of Q4 2014. The key questions from here to ask are: a) Did GDP just peak? and b) How is Q4 and beyond shaping up?

On the first point, to us it certainly looks like Q3 GDP was the peak, or close to it. On a sequential basis, GDP was up +5%, which was the best sequential increase since Q2 2011. On a year-over-year basis, it was the second best print since Q2 2011. Most importantly, on a two and three year average basis this was the best year-over-year growth rate since Q2 2011. The question from here, of course, will the rate of change accelerate or decelerate, on the margin?

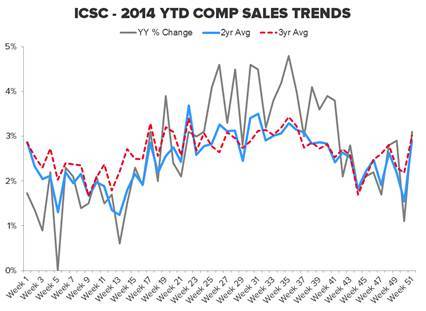

Staying on the theme of consumption as a big driver of Q3 GDP, our Retail Sectorhead Brian McGough circulated a chart of “ICSC (International Council of Shopping Centers) YTD Comp Sales Trends”, which is in the Chart of the Day, and according to McGough:

“A big rebound in sales for the week, but this follows two big weekly declines in the context of an intermediate term downtrend. The point there is that with sales trending down so much into the biggest holiday week, it makes sense that retailers would really turn the discounting machine into overdrive to have any shot at hitting numbers and prevent a glut of inventory in January. Online sales trends per Channel Advisor are downright sobering.”

Certainly, this data doesn’t guarantee that Q4 GDP will slow from Q3, because it is still possible that old St. Nicholas has some last minute shopping to do!

It won’t all be coal in our stockings heading into 2015. One area that we recently highlighted as likely to see improvement and outperformance in 2015 is U.S. housing. A headwind to housing has been the inability, by some, to get credit. Aside from the potential easing of down payment rules, another key area that might provide a credit tailwind is the improvement in subprime mortgage market.

According to an analysis by Barclays, subprime mortgage bonds have gained 12% this year, which is more than 6x the return of junk rated corporate debt. In aggregate, subprime bonds have returned more than 75% since 2010. To be fair, 30% of the subprime mortgages tied to these bonds are more than 60 days delinquent, but that too is an improvement from 41% in 2010.

Certainly, we aren’t hoping for a return to the days when mythical characters like Santa Clause took out mortgages with no paperwork, but incremental improvement in the ability to get financing for the younger and less wealthy demographic is a real positive.

As it relates to real-time data on housing, my colleague Christian Drake wrote a note yesterday that looked at new home sales and recent pricing data. While in his words new home sales was still a bit muddling, on the pricing front FHFA Home Price Index accelerated to +4.4% in Oct from +4.2% in Sep. All three primary price series are telling the same (2nd derivative) stabilization story.

So really what we are saying is that if your loved ones were really well behaved in 2014, this is probably a very good time in the cycle to buy them a house!

Our Global Macro Risk Ranges are now:

UST 10yr Yield 2.04-2.27%

SPX 1957-2110

RUT 1125-1208

VIX 13.17-24.35

USD 89.08-90.66

YEN 118.43-121.18

WTI Oil 52.87-59.23

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research