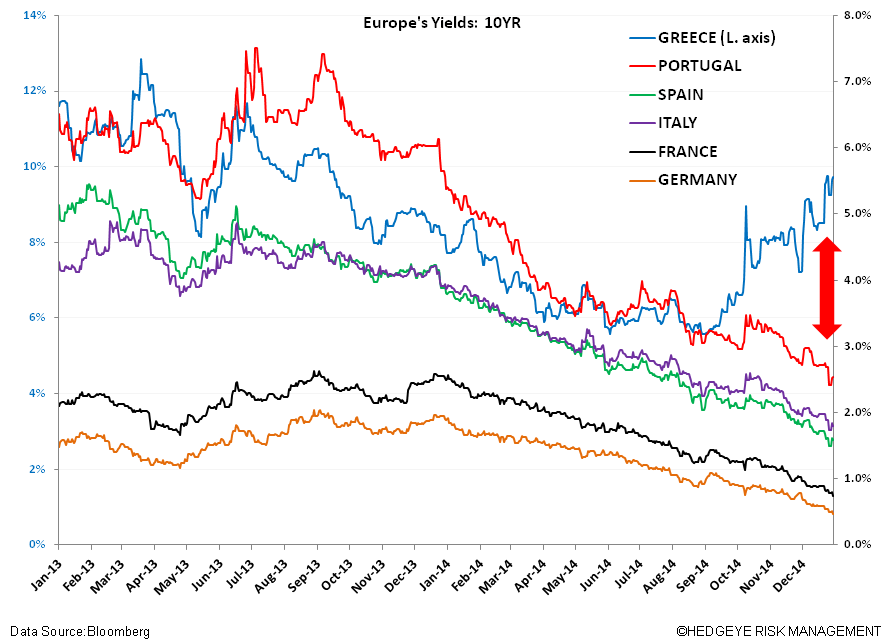

Constipation over Greece? You bet! The political indecision leading to a call for snap general elections on January 25th has sent Greek bonds down -7.4% and Greece’s Athex Index down -24% over the last month.

There’s also spillover talk this week of Greece exiting the Eurozone as a result of an article in the German publication Der Spiegel over the weekend. The article cited an unnamed German government source who said both German Chancellor Angela Merkel and her Finance Minister Wolfgang Schaeuble have a contingency plan for a Greek exit, labeling it manageable.

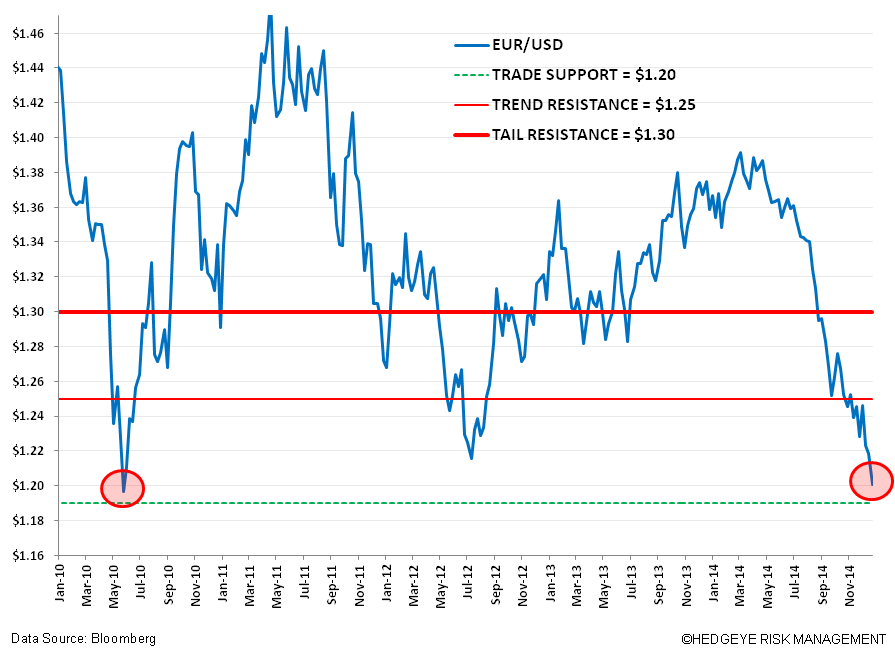

The story helped send the EUR/USD to a 9 year low near $1.1865; however, Merkel’s government was quick to counter the article by saying it will continue to support Greece in the Eurozone.

What can we as investors believe as the fate of Greece?

Below we give the puts and takes on why we believe it’s unlikely that Greece exits the Eurozone. While elections on January 25th threaten to increase global market risks over the next weeks (into and out of the event), the recent trend suggests downside risk is much more concentrated in Greek markets (rather than the broader Eurozone markets). WE EXPECT THIS TREND TO PERSIST.

This new dynamic, where Greek news and events do not drag down international markets (or at least to a much lesser extent), may in fact suggest that Greece’s risk profile is different this time as is the sovereign community and banking industry who are much more prepared for the potential of a fallout.

That said, we assign less than a 10% chance that Greece exits the Eurozone, as we believe both the Greek and Eurozone/international community will be incentivized to make concessions where needed (regardless of how a coalition forms after elections) so as not to rock the cradle of the Eurozone project.

We continue to expect weakness in the EUR/USD (the cross remains broken across its TRADE, TREND and TAIL duration levels). Eurozone headline risk mixed with the prospect of QE with which ECB President Mario Draghi continues to tease the market (along with outlining for a Q1 2015 release). We’re not buyers of Greek or European equities here. Note that both the STOXX50 and STOXX600 are broken across our TRADE and TREND levels.

The Political, Cultural, and Financial Climate Spell NO Exit

Eyes on January 25th – the date of the Greek snap general election: keep in mind that despite polls suggesting that the far left anti-austerity Syriza party (headed by Alexis Tsipras) leads in polls (by around ~3% ahead of the ruling conservatives New Democracy) his party stands far from an absolute majority even if it takes the top spot.

Some Key points that suggest the likelihood of No Exit:

- Tsipras will have to form a coalition and his potential partners are decidedly against an exit. Based on a survey poll by Rass conducted on December 29-31, Syriza is holding a 3.1% lead at 30.4% vs 27.3% for New Democracy. This compares to a 3.4% lead in a poll carried out a week prior.

- Tsipras/next government must play to an electorate that is decidedly against an exit: a recent poll by Rass last month showed 74.2% of Greeks said the country must stay in the Eurozone at all costs, while 24.1% disagreed.

- Tsipras himself has moved away from a past position that Greece should exit the Eurozone. In fact in the last weeks he’s been very vocal suggesting that Greece should stay in the Eurozone, which makes sense given populous sentiment in favor or staying.

- Tsipras/next government wants to play ball with Troika (The EU, IMF, and ECB): Despite numerous bailouts (public and private) since the sovereign ‘crisis’ began in 2010, the public debt load remains a monster €317 billion (~ $386.7 billion) or about 175% of Greek GDP. If Tsipras/next government can strike a deal with them on a “path to reform” they may forgive some of the country’s debt.

- Troika Wants to play ball with Greece: most of Greece’s debt, around €250 billion, is held by the official sector: the IMF, the ECB, the European Financial Stability Facility (EFSF) and bilateral loans by Eurozone member states. This means there is a strong incentive to not see these loans default, nor any investor ripple effects that may bring further downside to the broader European markets.

- Eurozone officials remains committed to Greece: in late December the board of the European Financial Stability Facility (EFSF) granted Greece a 2-month extension of funding from originally December 31, 2015 to an extended February 28, 2015 cutoff. This allows an additional/remaining €1.8 billion of funds to be disbursed. This “charity” further shows the commitment of the Eurozone to Greece and its ability to amend/make compromises on fiscal matters.

Risk Rising – This Time Is Different?

The dynamic around Greece may in fact be different this time. While in past years since the crisis began, the smallest of Greek news had the power to tank global markets.

If we look to our European Financial monitor as an indicator, this time around we see a major spike in Greek banks' CDS (widened between 159 and 229 bps last week), whereas Bank CDS throughout the region was flat to slightly down, on the whole. Additionally the big downside moves in the Greek equity and debt market since PM Samaras called an early presidential election were largely contained domestically. Surely these are partly indications that governments and market participants are more comfortable with the prospect of a Greek exit.

However, we believe the political, cultural, and financial points mentioned above spell the very unlikely probability that Greece exits the Eurozone anytime soon. Given the interconnectedness of markets and also the still very bloated and weak sovereign and fiscal state of Greece, it appears that any gains that could be realized by its own currency and central bank to set interest rates are trumped by fears of weak growth and the inability to pay down its debt and raise credit if were to go at it alone.

Once again it appears that the Eurocrats will continue to trumpet their Eurozone project and the Greeks believe their own prospects are better if they stay IN rather than OUT of the union.

We’ll be waiting and watching (with an investment in Greece on sidelines) as we approach elections on January 25th.

Matthew Hedrick

Associate