Nobel Laureate Joseph Stiglitz is out this morning saying the stock market recovery is "ïrrationally exuberant" as it relates to an economic recovery. Mr. Market seems to vehemently disagree with Mr. Stiglitz, as the futures are solidly in the green this morning across the board in the U.S. While we certainly wouldn't disagree with Mr. Stiglitz's assessment that employment will be a drag on a recovery in the U.S. and that the market has moved very quickly, we continue to play the game in front of us. So far the game is simply this, dollar down equals stock market up.

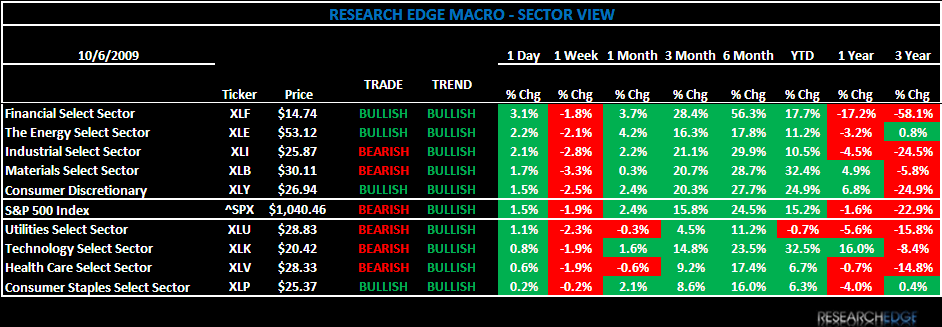

On Monday, the S&P 500 closed at 1,040, up 1.5% on the day. Yesterday’s move was on very low volume, as the S&P 500 broke a 4-day losing streak. For the S&P 500 the TRADE remains bearish, while the TREND is bullish.

The MACRO calendar offered an upside surprise yesterday, as the ISM non-manufacturing index rose to 50.9 in September from 48.4. This was the first reading of the ISM non-manufacturing index in the expansionary territory since September 2008. Consensus expectations were for a reading of 50. New orders jumped to 54.2 from 49.9 in August, the highest level since July of 2007, while business activity rose to 55.1 from 51.3.

Monday’s portfolio moves included selling the EWA and shorting KR, BAC and DRI. We also re-shorted the DIA. We are shorting more of the financially leveraged old economy companies in the DIA, which remains the worst performing major equity index globally year-to-date.

The dollar index fell 0.4% on the day, as the inverse correlation between the U.S. dollar and U.S. equities continued to be the primary factor in equity market performance. The VIX fell 6.4% on Monday and is now up 6.6% over the past week, but at 26.8 still remains solidly below the 30.0 level it broke in early July.

Five of the nine sectors outperformed the S&P 500, with every sector positive on the day. The three best performing sectors were Financials (XLF), Energy (XLE) and Industrial (XLI), while Technology (XLK), Healthcare (XLV) and Consumer Staples (XLP) were the bottom three. We are currently long the XLV.

The Financials (XLF) was the best performing sector on the back of Goldman raising its view on the group. Goldman highlighted the earnings power at the large banks vs. regionals, upgrading WFC and adding COF to its Conviction Buy List.

Today, the set up for the S&P 500 is: TRADE (1,021) and TREND is positive (983). The Research Edge quantitative models have 9 of 9 sectors in the S&P500 positive on TREND and 4 of 9 sectors are positive from the TRADE duration. Yesterday, the XLE, XLF and the XLY moved back to being BULLISH on the TRADE duration.

Right now the Research Edge models suggest that there is 2% downside and 1% upside in the S&P 500. At the time of writing, the futures pointed to a meaningfully higher open with Dow +72, Nasdaq +14, and S&P+9.

Howard Penney

Managing Director