Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

Today's Focus: November Pending Home Sales Index

The National Association of Realtors (NAR) today released its Pending Home Sales Index for the month of November.

Pending Home Sales increased +0.8% MoM (vs. -1.2% prior), accelerating to +4.1% on a year-over-year basis. Home Sales increased across all regions with YoY growth accelerating across each as well. Compares continue to ease from here.

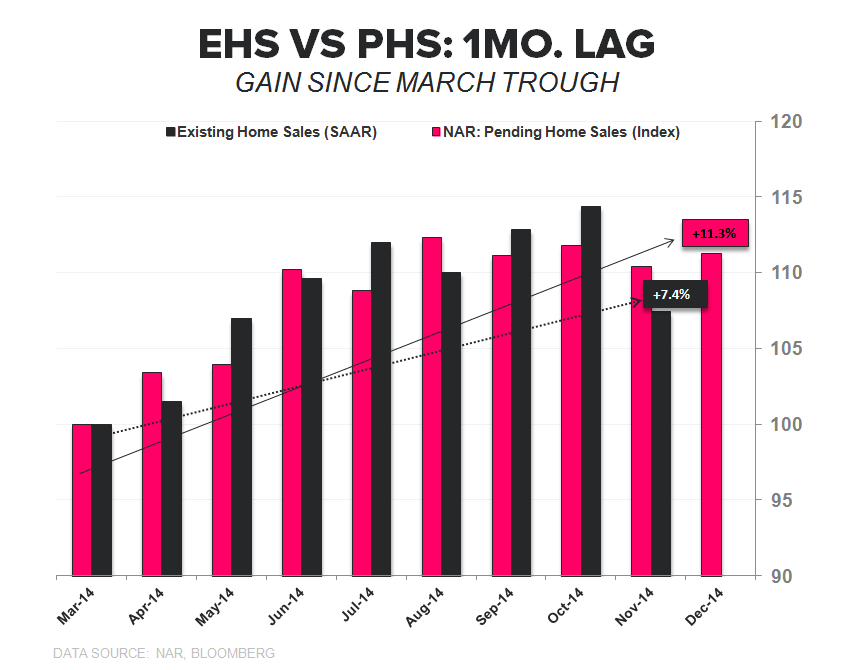

EHS Acceleration? PHS is a leading indicator for EHS with an R-square of 0.86+ between the two series (lagged 1-month) over the history of the data. Thus, the EHS release is typically uneventful as both the direction and magnitude of change in existing sales is well-telegraphed by the Pending Home Sales report a month earlier.

However, we’ve seen rising volatility/divergence between EHS & PHS on a month-to-month basis since the series troughed in March. Summarily, and as the 1st chart below illustrates, EHS began to diverge from the more modest gains in PHS in September and October. We posited that unless PHS saw a significant positive revision or showed material acceleration, reported gains in EHS would likely retreat.

We saw this materialize in November with reported EHS dropping -6.1% sequentially, falling below the gain in PHS and taking the cumulative gain from trough to +7.4%. Now the setup has essentially reversed with the balance of risk for EHS to the upside with cumulative growth in PHS at a premium to EHS and showing incremental strength in November.

RoC Improvement..Early Evidence: A core (albeit simple) underpinning to our positive view on housing for 2015 is the progressively easier demand comps as we traverse the peak negative impact of rates/weather/credit tightening into 2H15. We are seeing early evidence of 2nd derivative improvement with Pending Home Sales rising +4.1% YoY in November, marking a 3rd straight month of positive growth (following 11-months of neg. growth) and accelerating 200bps vs. the +2.1% growth reported last month. In the intermediate term, demand compares continue to ease into February with Dec-Feb comps of -8%, -9%, -10%, respectively.

About Pending Home Sales:

The Pending Home Sales Index is a monthly data release from the National Association of Realtors (NAR) and is considered a leading indicator for housing activity in the US. It is a leading indicator for Existing Home Sales, not New Home Sales. A pending home sale reflects the signing of a contract, but not the closing of the transaction, which occurs 1-2 months later. The NAR uses data from the MLS and large brokers to calculate the Pending Home Sales index. An index value of 100 corresponds to the average level of activity during 2001.

Frequency:

The NAR Pending Home Sales index is released between the 25th and the 31st of each month and covers data from the prior month.

Joshua Steiner, CFA

Christian B. Drake