Here's a quick look at some of the top videos, cartoons, market insights and more from Hedgeye this past week.

HEDGEYE TV

IS UA THE NEXT NKE?

On December 18, the Hedgeye Retail Team hosted a Black Book call on the athletic apparel and footwear space. On Wednesday we released this excerpt, in which Sector Head Brian McGough explains how his opinion of athlete endorsements has evolved (which is particularly relevant given $UA's recent signing of Andy Murray) and reveals what Under Armour needs in order to become the next Nike.

This institutional conference call focused on Athletic footwear and apparel space. Specific names included Nike (NKE), Adidas (ADDYY), UnderArmour (UA), Foot Locker (FL), Hibbett (HIBB), Dick's Sporting Goods (DKS), and Finish Line (FINL) - which collectively offer up a good mix of LONGS and SHORTS.

HEDGEYE CEO KEITH MCCULLOUGH SHARES THE TOP THREE THINGS IN HIS MACRO NOTEBOOK MONDAY MORNING.

DETECTING DECEPTION

In December our Restaurants Team held a conference call for institutional investors Statement Analysis - Putting Companies Through a Linguistic Polygraph Test with former U.S. Deputy Marshall Mark McClish.

Mark McClish is the author of I Know You Are Lying and the creator of the Statement Analysis method. In this brief excerpt Mark explains how to identify signs of deception and dissects an excerpt from HAIN’s Q1 earnings call as an example.

Reading conference call and analyst meeting transcripts is a key part of the analyst’s job. We all use words to define our reality, and our choice of words can be revealing. The premise of Statement Analysis is that a person’s choice of specific words can reveal when there might be an attempt at deception. This Statement Analysis exercise looks exclusively at a company’s written and verbal statements. Using these hidden clues, we can dig deeper into a company’s public pronouncements for signals of potential concerns in a company’s reporting.

CARTOON

Oil Plunge!

Oil prices slumped almost 50% in 2014, set for the biggest annual decline since 2008. "It's flat out ugly for whoever is long inflation expectations in Energy terms," says Hedgeye CEO Keith McCullough.

The Sound of Deflation

That sound you're hearing around the globe? Deflation.

CHART

Real- Time Alerts: Historical Closed Position Return Distribution

The brief excerpt below is from Tuesday's Morning Newsletter written by Hedgeye U.S. macro analyst Christian Drake.

We’ve #TimeStamped 2,969 signals in Real-Time Alerts since 2008. The historical data is there to see and download on our website and in the Chart of the Day below we show the return distribution across RTA’s 6+ year history. In our attempt to further the evolution towards an investing meritocracy, we feel we’ve built a better Risk Management mousetrap.

As always, you are free to disagree. We happily accept and consider all (thoughtful) criticism as we work to continually evolve the process.

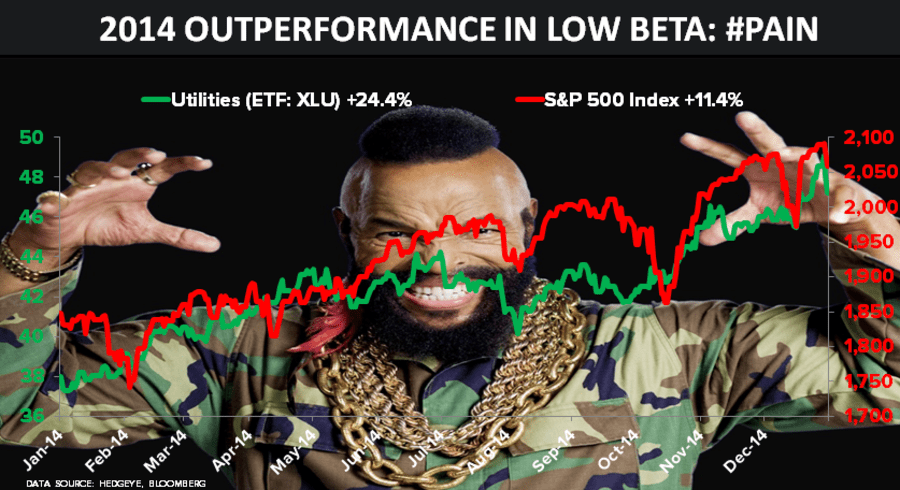

2014 Outperformance in Low Beta: #PAIN

This is a brief excerpt from Friday's Morning Newsletter by Hedgeye CEO Keith McCullough.

* * * * * * *

If you’re a U.S. equity only investor, the lower-volatility + higher-absolute-and-relative returns came in mostly slow-growth, lower-beta, #YieldChasing sectors:

- Number 1 (within the Top 9 S&P Sectors) for 2014 was Utilities (XLU) at +24.3% YTD

- Number 2 for 2014 was Healthcare (XLV) at +23.3% YTD

Yep, instead of being long #deflation (Energy stocks, XLE, DOWN -10.6% YTD), these slower-growth, lower-volatility sectors had similar returns to what? Yep – the Long Bond.