Editor's note: This unlocked research note was originally published by Hedgeye Healthcare Sector Head Tom Tobin and analyst Andrew Freeman on December 23, 2014 at 09:43.

Tracker update

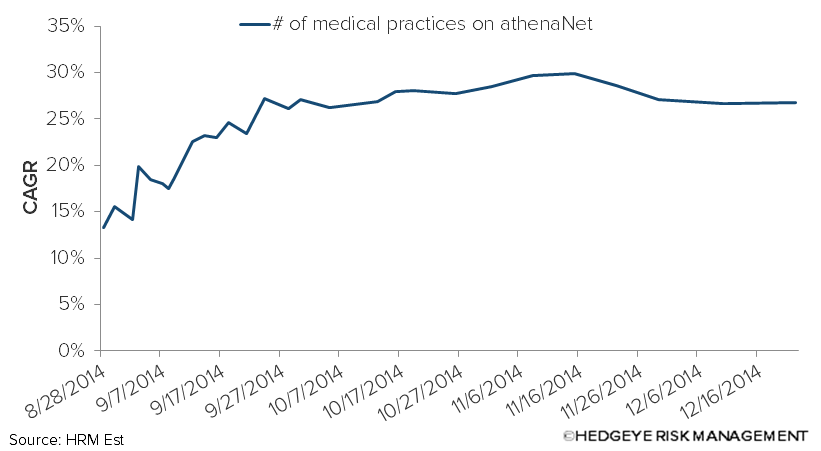

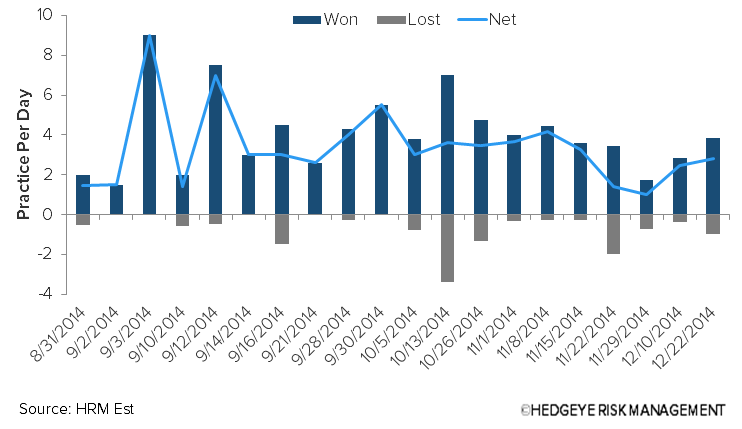

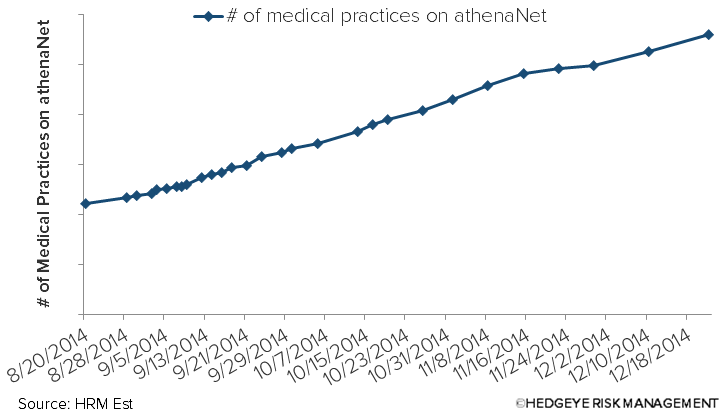

Update through 12/22 places the annual growth rate of new medical practices on athenaNet at 27%. In terms of attrition, net adds since 12/10 were 34, with 46 practices won and 12 lost. Sequential q/q growth is tracking 6.1%.

Please call or e-mail with any questions.

---

APPENDIX

Andrew Freedman

Analyst

203-562-6500

@HedgeyeHIT

Thomas Tobin

Managing Director

203-562-6500

@HedgeyeHC