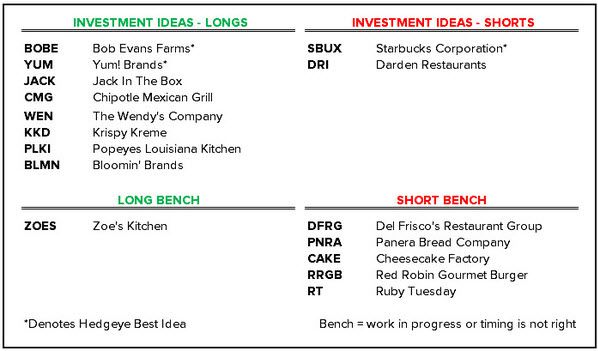

Key Points

- Casual Dining, Family Dining, Fine Dining, and Sandwich two-year comps are expected to accelerate throughout 2015.

- Coffee, Fast Casual, and Pizza two-year comps are expected to decelerate throughout 2015.

- Comp estimates, in aggregate, appear aggressive perhaps driven by recent encouraging reports from Black Box and Knapp as well as declining gasoline prices.

- For this reason, we believe we are well-positioned to identity several opportunistic shorts next year.

Casual Dining Consensus SSS Expectations (3Q14-4Q15)

- Casual Dining two-year accelerating 100 bps to 1.7%

- BJRI two-year accelerating 200 bps to 1.1%

- BLMN two-year accelerating 30 bps to 1.8%

- BBRG two-year accelerating 240 bps to -2.8%

- BWLD two-year decelerating 60 bps to 4.5%

- CAKE two-year accelerating 35 bps to 1.7%

- CHUY two-year decelerating 50 bps to 2.6%

- DIN (Applebee’s) two-year accelerating 60 bps to 1.3%

- DIN (IHOP) two-year decelerating 95 bps to 2.1%

- DRI two-year accelerating 230 bps to 1.6%

- EAT two-year accelerating 160 bps to 2.0%

- IRG accelerating 225 bps to -0.1%

- KONA two-year decelerating 5 bps to 2.6%

- RRGB two-year decelerating 65 bps to 2.7%

- RT two-year accelerating 660 bps to 1.5%

- TXRH two-year accelerating 55 bps to 4.9%

Coffee Consensus SSS Expectations (3Q14-4Q15)

- Coffee two-year decelerating 156 bps to 3.4%

- DNKN two-year decelerating 130 bps to 1.9%

- KKD two-year decelerating 60 bps to 2.9%

- SBUX two-year decelerating 95 bps to 5.1%

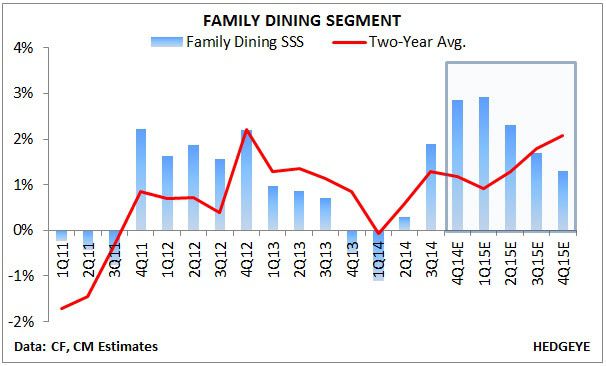

Family Dining Consensus Expectations (3Q14-4Q15)

- Family Dining two-year accelerating 78 bps to 2.1%

- BOBE two-year accelerating 225 bps to 1.3%

- CBRL two-year decelerating 20 bps to 2.9%

- DENN two-year accelerating 30 bps to 2.1%

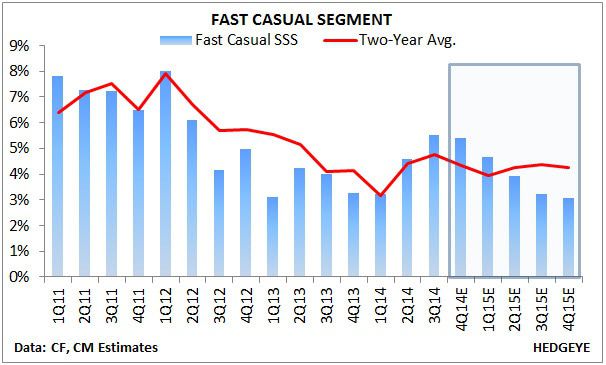

Fast Casual Consensus Expectations (3Q14-4Q15)

- Fast Casual two-year decelerating 52 bps to 4.3%

- CMG two-year decelerating 230 bps to 10.7%

- FRGI (Pollo Tropical) two-year decelerating 160 bps to 4.6%

- FRGI (Taco Cabana) two-year accelerating 55 bps to 3.2%

- NDLS two-year accelerating 20 bps to 2.1%

- PBPB two-year accelerating 30 bps to 1.8%

- PNRA two-year accelerating 130 bps to 2.7%

- ZOES two-year decelerating 210 bps to 4.7%

Fine Dining Consensus Expectations (3Q14-4Q15)

- Fine Dining two-year accelerating 52 bps to 1.9%

- DFRG two-year accelerating 75 bps to 2.5%

- RUTH two-year decelerating 105 bps to 3.5%

Pizza Consensus Expectations (3Q14-4Q15)

- Pizza two-year decelerating 173 bps to 3.9%

- DPZ two-year decelerating 160 bps to 5.0%

- PZZA two-year decelerating 185 bps to 2.8%

Sandwich Consensus Expectations (3Q14-4Q15)

- Sandwich two-year accelerating 44 bps to 2.6%

- BKW two-year accelerating 55 bps to 2.2%

- JACK (JIB) two-year accelerating 120 bps to 2.1%

- JACK (Qdoba) two-year accelerating 155 bps to 6.4%

- MCD two-year accelerating 145 bps to 0.3%

- PLKI two-year decelerating 230 bps to 3.9%

- SONC two-year decelerating 220 bps to 3.1%

- WEN two-year decelerating 15 bps to 1.8%

- YUM two-year accelerating 340 bps to 1.4%

Howard Penney

Managing Director

Fred Masotta

Analyst