Below are Hedgeye analysts’ latest updates on our six current high-conviction long investing ideas.

We also feature two pieces of content from our research team at the bottom.

*Note: We will send CEO Keith McCullough’s updated levels for each investing idea in a separate email.

CARTOON OF THE WEEK

IDEAS UPDATES

TLT | EDV | XLP | MUB

Does Your View on Rates Include the Risk of a "Reflexive Deflationary Spiral"?

Takeaway: We see amplified risk of a reflexive deflationary spiral over the NTM, strengthening our non-consensus bullish bias on long-term Treasuries.

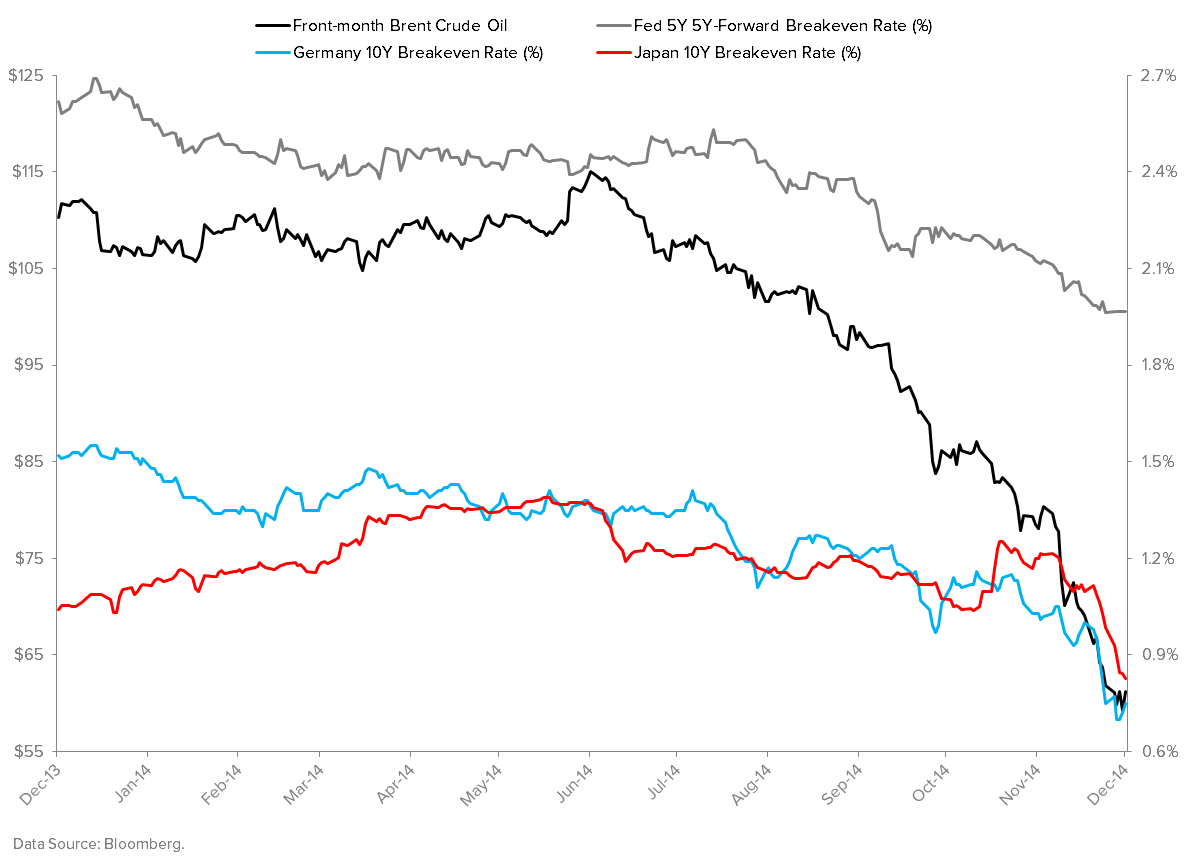

To start, please review slides 29-39 of our 12/16 presentation on Emerging Markets, which outlines a probable fundamental case for EUR parity and a re-test of the August ’98 lows on the JPY with respect to the intermediate term. Those just might be 11 of the most important ~20 charts in all over global macro by this time next year. CLICK HERE to access that presentation.

Moving along, let’s review where consensus is on rates:

- We know the sell-side is bullish on rates (i.e. bearish on Treasury bonds). Always have been; always will be. To my knowledge, there simply aren’t enough banking and trading fees associated with being bullish on long-term Treasury bonds in lieu of other asset classes. Along those lines, it’s worth noting that since the onset of the economic recovery, the start-of-year Bloomberg consensus forecast for the 10Y Treasury note yield at the end of the corresponding year has been off by an [astounding] average absolute value of 106bps! Sell-side consensus thinks rates put on +87bps from today’s price to close out 2015 at 3.05%.

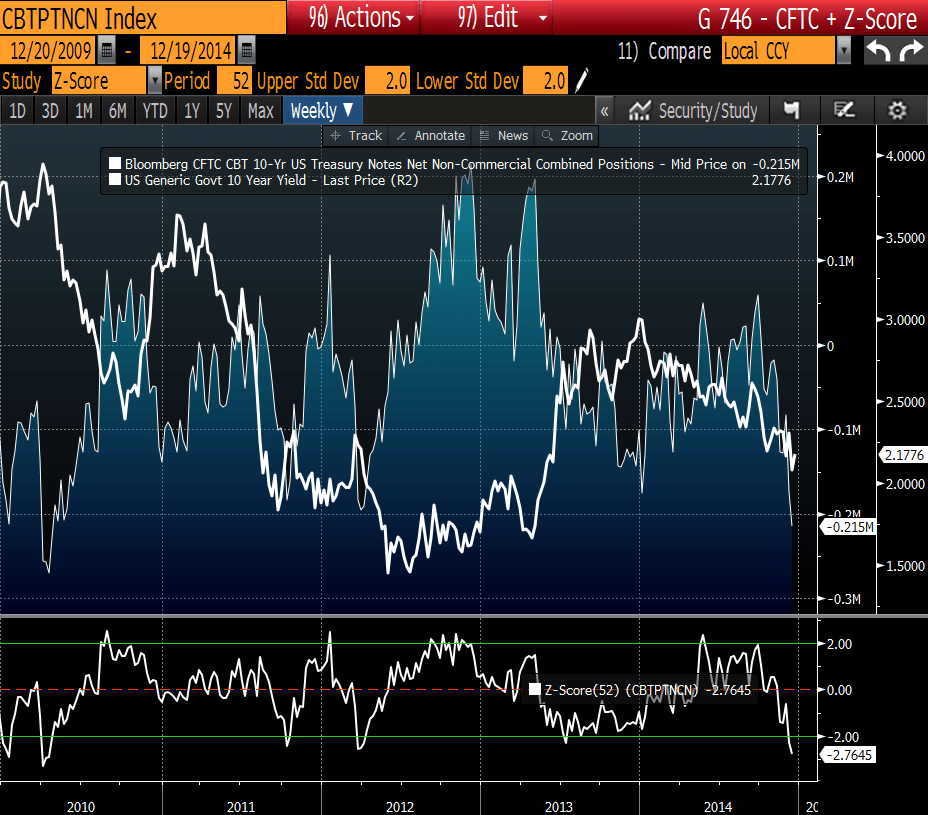

- The buy-side is perhaps even more bullish on rates (i.e. bearish on Treasury bonds) at the current juncture. The net SHORT position of 215k 10Y Treasury note futures and options contracts is the widest net SHORT position since April of 2010. On a TTM Z-Score basis, which we use to show deviations that are typically indicative of crowded trades, the buy-side hasn’t been this net SHORT of long-term Treasuries since March 2012, October 2011 and April of 2010. The subsequent draw-downs in the 10Y Treasury note yield from those peaks in bearish sentiment are -99bps, -45bps and -160bps, respectively.

Source: Bloomberg L.P.

Source: Bloomberg L.P.

So, is this time different? Will “the crowd” finally be right on long-term Treasuries? Having been appropriately bearish on rates (i.e. bullish on Treasury bonds) in 2014 (after having been bullish on rates in 2013), we are in an enviable position of lacking the kind of baggage that might cloud our judgment.

Regarding that judgment, we strongly believe the aforementioned dynamics in the currency market are likely contribute to a “reflexive deflationary spiral” whereby continued global macro asset price deflation and reported disinflation both contribute to rising investor demand for long-term Treasuries, at the margins.

Here’s how that process would work:

Step 1: Both the BoJ and ECB accelerate their monetary base expansion, at the margins, during a time where the Fed is on hold and deliberating [out loud] the appropriate timing of their first [and subsequent] rate hikes. Looking to our proprietary G3 Monetary Policy Model, which contextualizes trends across 10 key economic and financial market indicators, the ECB is clearly facing immense pressure to ease. The Fed should maintain a neutral-to-ever-so-slightly-dovish bias, while the BoJ should maintain a slight hawkish bias. That said, the BoJ’s current composite score is roughly equivalent to its late-October score, when Kuroda pushed through a contentious expansion of the BoJ’s QQE program. That signals to us that politics, not economics, are the primary driver of the BoJ’s current easing bias.

Current:

October 30

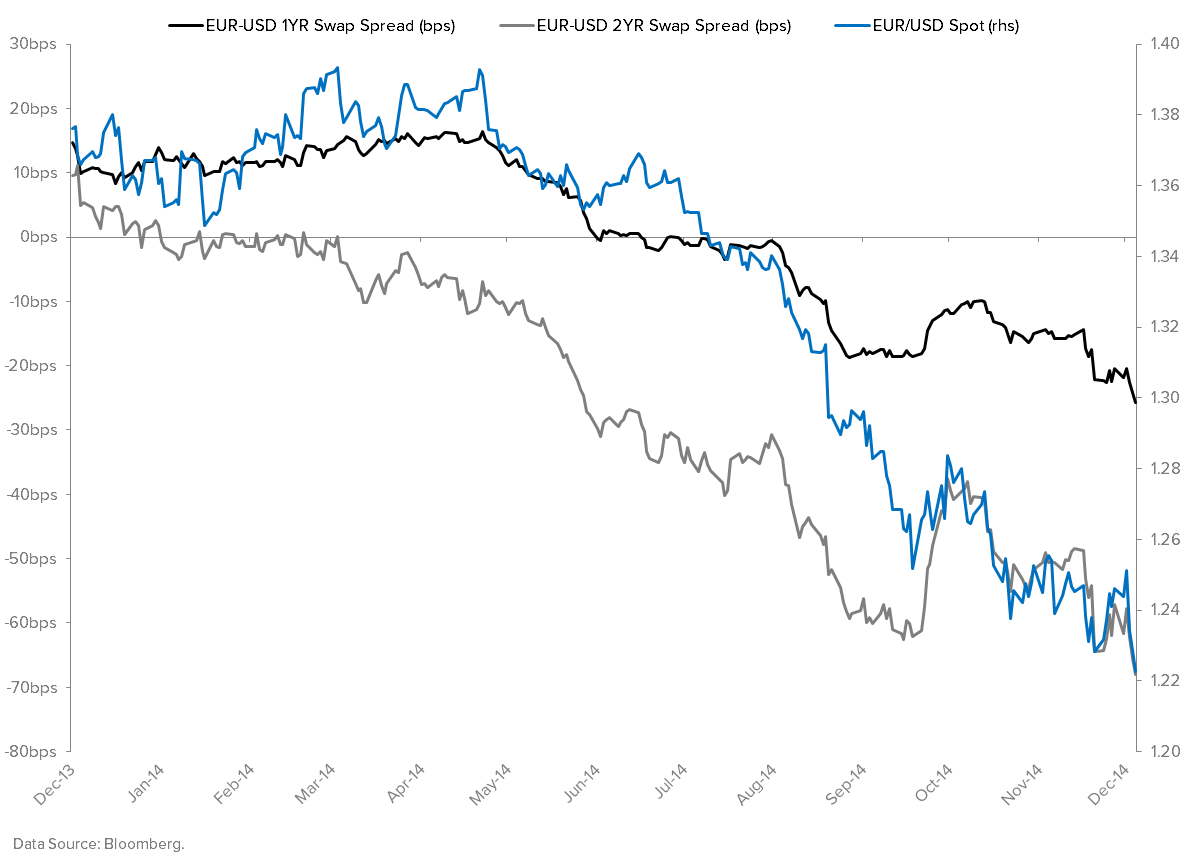

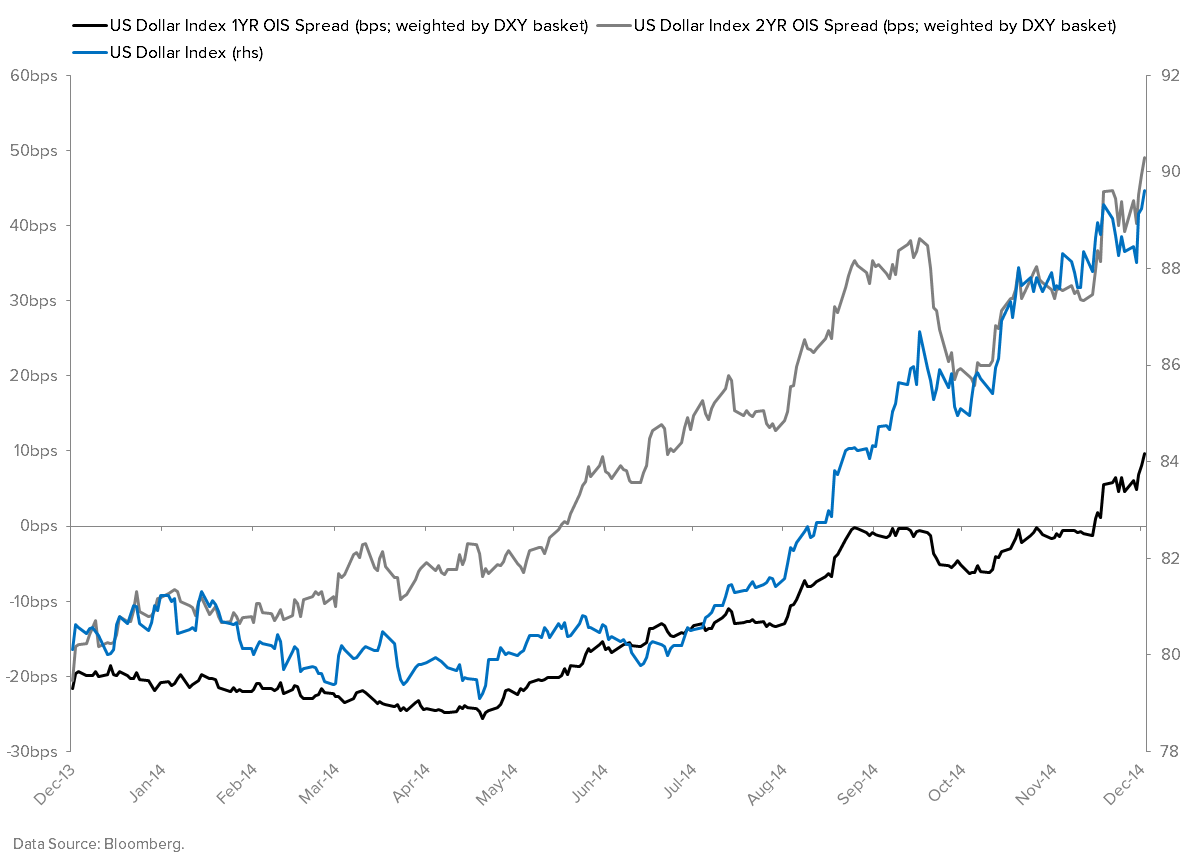

Step 2: As G3 monetary policy continues to diverge, the currency market responds by appropriately inflating the value of the U.S. dollar vis-à-vis peer and emerging market currencies. We think the implied ~3% appreciation of the U.S. Dollar Index through year-end 2015 as currently assumed by Bloomberg consensus is way off the mark. The DXY is up over +3% since the end of October alone!

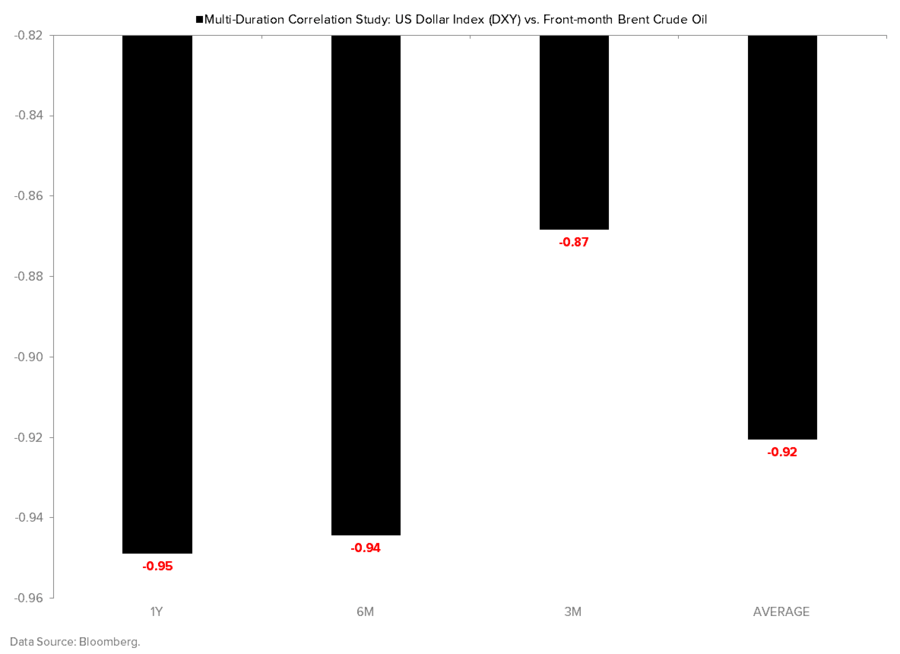

Step 3: As the dollar strengthens, commodity prices continue their deflationary descent.

Step 4: As commodity prices continue to fall, both expected and reported CPI readings continue to fall. At first, breakevens and headline CPI rates will bear the brunt of the aforementioned deflationary forces. We anticipate core CPI readings are likely to follow those rates lower on a lag.

Step 5: As reported inflation slows in all three of the world’s major economies, the pressure for each central bank to get marginally dovish will heighten. The central bank closest to achieving its mandate (i.e. “full employment” and “price stability” in the U.S., “price stability” in the Eurozone and “5% monetary math” in Japan) is likely to see its currency bear the brunt of global capital flows as investors anticipate relatively weaker monetary policy for longer in the other two economies. For now, that is undoubtedly the U.S. dollar.

Step 6: Repeat steps #3-5.

Scary stuff if you bought the dip in Russia (RSX) or domestic E&Ps (XOP)…

RH

Retail Sector head Brian McGough has no new update on Restoration Hardware this week. Shares of RH notched a new record high on Thursday trading over $100, before falling back a bit on Friday to finish the week up 3%.

RH is up almost 18% over the past month.

YUM

Counting on Creed

If there was one key takeaway from the analyst day we attended a couple of weeks ago, it is that new CEO Greg Creed is the real deal. The energy, creativity, and passion he brings to the business cannot be understated. He played an instrumental role in the Taco Bell turnaround and is now in a place to effect change across the whole organization. While Mr. Novak built a tremendous company, Mr. Creed was very clear that his vibrant personality will transpire throughout the organization. He will leave his mark, and we think it will be for the better.

As we mentioned in last week’s addition, the new global reporting structure allows for a clean split of YUM’s business units into multiple asset light models. What we failed to mention, however, is that this new structure should enhance brand focus across the portfolio. For this reason, we don’t necessarily need a restructuring or financial engineering event to occur to be comfortable with our long thesis. We genuinely believes the company, and its brands, are heading in the right direction.

In other words, there are multiple ways to win.

If an activist steps in, we win. If an activist doesn’t step win, we probably still win. All told, while an activist would likely create shareholder value rather quickly, we’re confident that this management team can be counted on to create value over the long haul. Looking one to two years out, under any scenario, we see the stock trading significantly higher than where it is today.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

just charts: eye-catching industrial data

Industrials Sector Head Jay Van Sciver shines a light on ten key developments.

DARDEN: recovery expectations are premature

We remain very cautious on DRI shares and believe expectations of a 2H15 recovery are not grounded in reality.