When your country’s central bank raises its interest rate a monster 650bps to 17% (as the Russian Central Bank did early this morning local time) and the currency still doesn’t go up, Houston, we have a problem.

By all accounts, we saw some of the most epic swings (ever) across Russian markets today. The whipsaw moves beg the important question: during these desperate times in Putin’s Russia, will we witness desperate measures taken?

In today’s Hedgeye Poll of the Day we asked: “Will Vladimir Putin take major military action in 2015?” The response was 65% “YES” versus 35% “NO”. Clearly, taking a “major” action to inflect the price of oil could be seen as desperate to some, or as a necessity to others.

We run though the current risk set-up impacting Russia below and offer accompanying charts illustrating current risks. While it remains unclear exactly how conditions will play out from here, the risk has markedly increased to the upside (over even just the last 24 hours).

Four factors worth considering upfront:

1) OPEC may have an agenda to tighten the screws on Russia and other countries with high break-even prices;

2) Currency crashes can be expedient and self-perpetuating;

3) Russia’s economic isolation and nationalism may extend the prospect of economic recovery;

4) The heavy ties of Russia’s largest companies to the State could expedite and heighten the sovereign risk profile.

A key news item to this entire story was released yesterday: the Russian government disclosed that state-owned Rosneft needed to raise capital, with help from the Central Bank, to cover $6.9Bn in a USD-denominated bridge term-loan due early next week. Rosneft issued $10.9Bn in new bonds at Friday’s exchange rate with large, State-owned banks buying the issue. The banks then deposit the bonds with the central bank, and Rosneft is financed with the printed Rubles. Rosneft, due to the current sanctions, is unable to roll the term loan with western banks, and so squarely looks like it desperately needed the money from the CB to foot the bill next week. Of note is that Rosneft CEO Igor Sechin is a close ally with President Vladimir Putin. The next unsecured USD-denominated debt from Rosneft is a $7.1Bn payment due February 2015.

While we look from the outside, on the streets the purchasing power of the Ruble is evaporating, quickly. Despite Putin’s popular approval rating still in the 80s, we’d be overweight the “YES” camp that in fact a crashing Ruble will propel him to take some form of desperate action.

We suggest you consider these risks to protect your portfolio during this downslide.

- Crash Mode 1: The USD/RUB is down -27% W/W and -56% YTD

- Crash Mode 2: The Russian Stock Market (RTSI) is down -28% W/W and -57% YTD

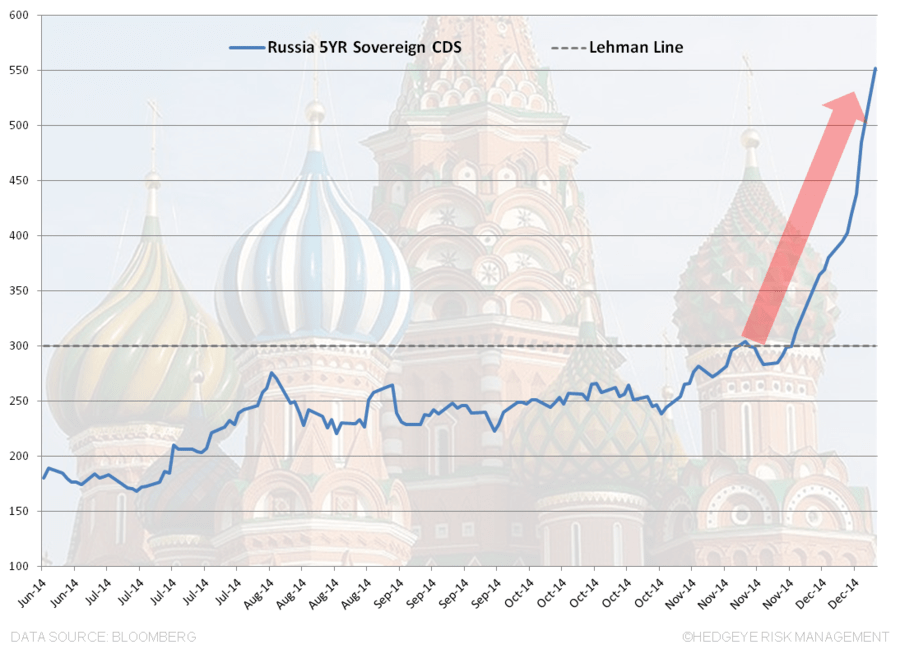

- Russia’s 5YR Sovereign CDS rose to 551bps (+67bps D/D) (above 300bps = Lehman breakout line).

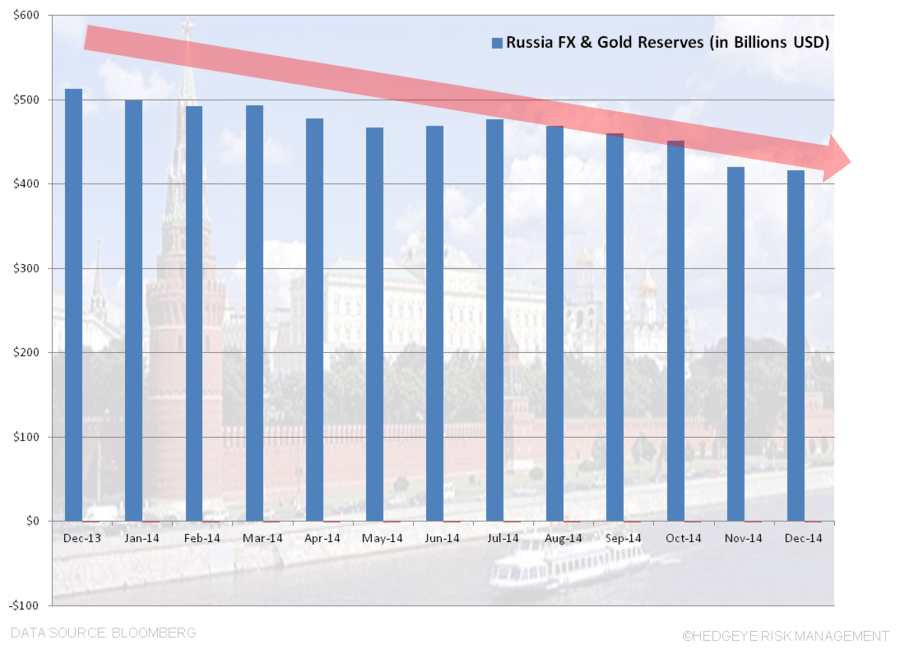

- The Russian Central bank has spent ~ $80 - $100 Billion on FX interventions to strengthen the RUB – but yet to no avail. The FX reserve is now at a 5YR low. Their total FX and gold reserve base is at $416.2Bn as of 12/05 (-18.50% YTD) and we’ll get an updated number from the CB on Thursday. They have already pumped dollars into the Russian banking system and bought Rubles (a move that would have been slightly reversed if there is any truth to the Rosneft debt bailout)

- The Russian Central Bank has raised the main interest rate 6 times this year; today’s 650bp increase to 17% follows last week’s 100bp hike. Here too there’s been no inflection in the currency or stock market.

- Brent Crude is down -46% YTD at $59.60. A close proxy for Russia’s Urals main export blend, according to Finance Minister Anton Siluanov the price needs to be at $90/barrel for the 2015 budget to balance (a level 51% above today’s price).

- Russia derives about 50% of its budget revenue from oil and natural gas taxes and 25% of its GDP is linked to the energy industry.

- The Russian Central Bank said today that 2015 GDP may shrink to 4.5% to 4.7%, the most since 2009, if oil averages $60 a barrel under a “stress scenario”. (We expect the 2015 GDP drag could be closer to -6% to -8%).

- The Russian Central Bank said net capital outflow may reach $134 billion this year, more than double last year’s total.

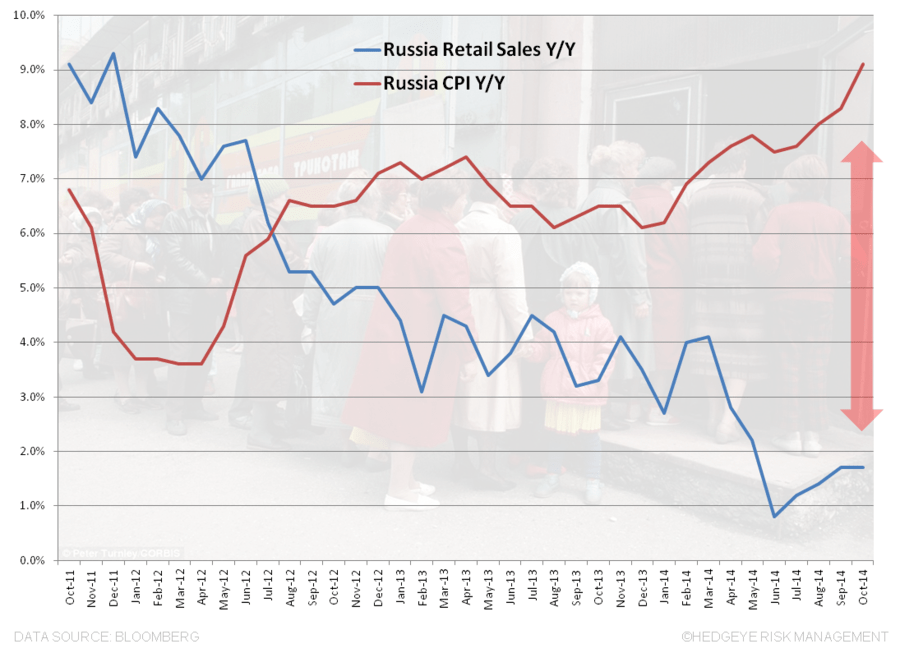

- Inflation is at a 3YR high at 9.1% while real wages are at a paltry 0.3%.

- Lower purchasing power via a depreciating currency + some higher local prices given import sanctions = the perfect cocktail for massive declines in consumer spending (beyond buying goods to lock in the “value” of the Ruble – evidence we’ve received anecdotally).

- Russian banking crisis risk is rising by the day: as a proxy, Sberbank, Russia's largest bank with 46% deposit share, has seen its CDS rise steadily since mid-year, up 50bps D/D to 576bps.

- Further, the CEO of Sberbank said back on November 14th that if the Russian economy were to decline by more than 1.2% in 2015 Sberbank would need the State to bail it out.

Matthew Hedrick

Associate

Ben Ryan

Analyst