“L’enfer est plein de bonnes volontes et desirs (the road to hell is paved with good intentions).”

-Saint Bernard of Clairvaux

I’ve been in London all week grinding away at client meetings with my colleagues and decided to treat myself to a nice dinner last night so I went to NOBU. Now of course a small town Canadian lad like me eating at NOBU in London may indeed be the best sign that we are in an asset class bubble, but that aside, as I was eating my raw fish last night, it made me really think about the increasing parallels between the European and Japanese economies.

On our proprietary economic model, the U.S. has some chance of bouncing out of Quad 4 in Q1 2015, even if briefly, but not so much for Europe. The Europeans will be solidly mired in this decelerating growth and disinflation environment for much of 2015 based on our current projections. As the real time economic data increasingly reflects this, it will likely give ECB President Draghi the cover he needs to go full on Japanese style monetary intervention.

In the chart directly below, we show the U.S. 10-year yield versus the French and German 10-year yields. No surprise given the collapse in these yields, the question of what is going on in the European sovereign debt market has been a big point of discussion in our meetings in London this week. The answer is pretty simple: the bond market is basically front running decelerating growth and deflation and the stark reality that the ECB is likely to put Europe on the Japanese path to economic perdition.

The quote at the beginning of this note effectively sums up the mindset of many global central bankers. They believe they have the best of intentions, but don’t truly understand the path they are setting economies on.

There are actually a number of psychological studies that validate this old maxim. In fact Professor Theodore Powers from the University of Massachusetts concluded the following in a study entitled “Implementation Intentions, Perfectionism and Goal Progress: Perhaps the Road to Hell is Paved with Good Intentions”:

“The results of both studies revealed a significant backfire effect of the implementation intentions on goal progress for participants high on a particular dimension of perfectionism.”

So yes indeed, it seems the road to failure, if not hell, is paved with good intentions.

Back to the Global Macro Grind...

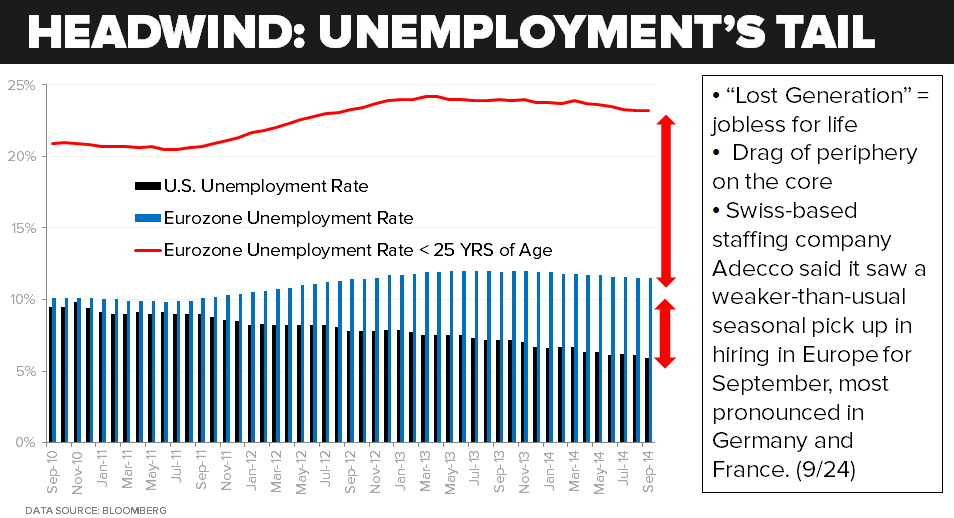

Staying on Europe for a second, one of the most glaring structural challenges we see at the moment is employment. In Chart of the Day below, we compare the U.S. unemployment rate with the Eurozone unemployment rate going back to September 2010, which very pointedly highlights that the U.S. has seen a marked employment recovery, while Europe has not. In effect, the European recovery remains a lot more slack, which will help amplify deflationary pressures.

The other key takeaway from the chart is the unemployment rate for people 25 or younger in the Eurozone. This rate is over 22% and climbing. So again like Japan, Europe has a longer term demographic challenge. In Japan, of course, it is the aging population, but in Europe it is the creation of a lost generation -- a generation that is grossly underemployed and unproductive.

In aggregate, there are 5.5 million people 25 and younger that are unemployed in Europe. To put that in context, it is roughly the population of Denmark. The numbers in some of the southern European countries are even more staggering. In Spain and Greece this cohort is 50% unemployed; in Italy it is 41% and in Portugal 36%.

Most social psychologists agree that the longer term issue with an inability to find a job when first entering the work force is a “scarring” effect. This lack of confidence or belief in oneself can, and does, lead to long term unemployment and under earning that can last decades. Because of this, the future in many parts of Europe does look extremely bleak.

Luckily for southern Europeans, their futures still aren't as bleak as Russia’s at $60 oil. For those that haven’t been watching, the Russian stock market is down-23% in the last month and now down -44% for the year-to-date. While perhaps there is now some value to be found in Russian stocks, the reality is that Russian economy is at risk of a major recession if oil stays at current prices.

Based on our math, the Russian economy shrinks by more than 1.25% for every $10 drop in the price of oil. So in aggregate, if oil stays at current levels the Russian economy can be expected to shrink 6 – 7% next year. When combined with a current inflation rate of +10%, you can easily see why one might be better off being young and unemployed in Spain!

Staying on the topic of oil, and to the benefit of the Russians, our commodities analyst Ben Ryan actually made the case for a bounce in oil in the short term. As he wrote:

“While we have been in front of the downside risk in oil in Q4, the expectation for lower prices (from here) is certainly becoming a psychological and consensus expectation, which we will fade when the time comes. The expectation for future volatility is blown-out. The commitments of traders report from the CFTC shows that the sum of aggregate positions in futures and options markets is between 1-2 standard deviations shorter than it has been over the last year. As a contra-indicator should work, the longest market positioning of 2014 was at the June highs in WTI.

We have a simple back-test model that tracks 60-day price performance in oil markets once contract positioning becomes +/- 1 standard deviation extended over different trailing durations. The result is that market positioning that chases price is a very obvious indicator to fade.”

With headlines now claiming OPEC is dead and traders leaning bearishly, there likely is reversion to the mean trade in oil waiting somewhere in the shadows.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr yield 2.12-2.24%

RUT 1151-1172

VIX 14.56-22.71

YEN 116.88-121.55

Oil (WTI) 58.41-64.72

Gold 1185-1236

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research