All else being equal, I thought the Casual Dining group held up well yesterday. I continue to think the FSR stocks are ahead of themselves given that demand is still very sluggish and we are nearing the end of the rope for many companies that have relied on cost cutting.

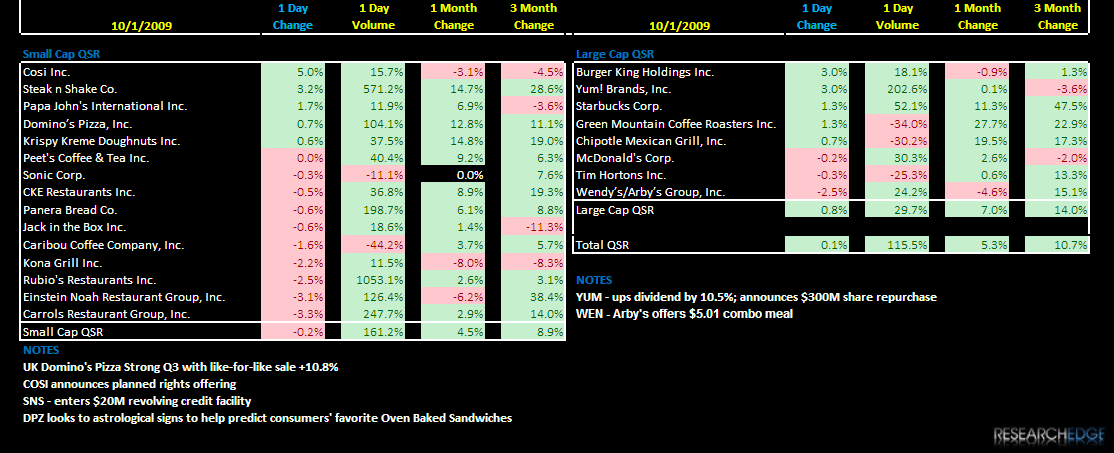

The next two big data points for the Restaurant Industry will be YUM’s 3Q09 EPS, which will be released after the market closes on Tuesday October 6th. Also, on Wednesday RT releases its FY1Q EPS after the market closes. We will have more to say shortly on each company, but I am not looking for any positives surprises out of either company.