EVENTS TO WATCH

COMPANY HIGHLIGHTS

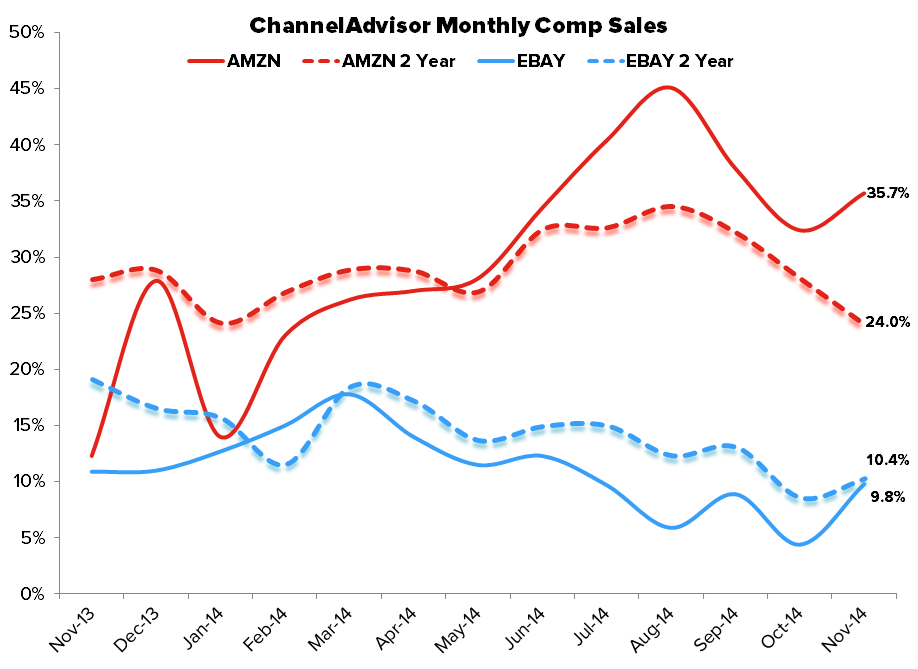

AMZN, EBAY - Growth Gap Narrows, AMZN Trials New Pricing Model

Takeaway: After a noticeable divergence between AMZN and EBAY comps from ChannelAdvisor throughout the year, we saw the gap close some in November, particularly on a 2year basis. Interestingly, this week Amazon announced a new "Make an Offer" feature where shoppers can offer a price below listed selling prices and proceed to barter with sellers. It is being trialed in the collectibles and fine art categories, and though different than an EBAY auction, it is a clearly a competing marketplace.

KSS - Kohl’s to keep stores open Dec. 19-24

(http://www.chainstoreage.com/article/kohl%E2%80%99s-keep-stores-open-dec-19-24)

"Kohl’s Department Stores will keep its doors open for more than 100 hours straight from 6 a.m. on Friday, Dec. 19 through 6 p.m. on Christmas Eve, Wednesday, Dec. 24."

Takeaway: Kohl's did this same marathon session last year, staying open from 6am Friday Dec. 20 to 6pm Dec. 24. This year they are adding an extra day likely just due to the calendar shift. We think that this is more of a cost event than it is a revenue event. The fact is that KSS needs to pay employees 2-3x hourly wages to work in the middle of the night, and we don't think that the market for buying $20 sweaters at 4am is particularly large. If KSS were confident in its merchandising and growth plan for this holiday, staying open all night wouldn't be part of the equation.

ANF - CEO Mike Jeffries retiring, effective immediately

(http://www.abercrombie.com/anf/investors/investorrelations.html)

Takeaway: This was probably the most anticipated CEO departure in all of retail. While it's great that the Board is now much higher quality and ANF can be run like a real company, the reality is that investors are still left with Abercrombie and Hollister -- brands that simply don't have the cache that they used to, or need to. There will likely be a time to load up on this name. But it will be when the brands, product, and distribution are re-positioned. That takes #time.

HERE ARE SIGMAS FOR TODAY'S EARNINGS

COST - 1Q15 Earnings

VRA - 3Q15 Earnings

FRAN - 3Q14 Earnings

OTHER NEWS

LULU - Lululemon's Innovative New Store Design

(http://www.retail-insider.com/retail-insider/2014/12/lululemon)

ANF - "Mr. Jeffries’s departure doesn’t open up the possibility of a sale of the company."

(http://www.wsj.com/articles/abercrombie-ceo-jeffries-to-retire-1418133344)

AMZN - Amazon-owned Twitch buys eSports agency GoodGame

(http://www.geekwire.com/2014/amazon-owned-twitch-acquires-esports-agency-goodgame/)

AMZN - Workers at Amazon Warehouses Won't Get Paid for Waiting in Security Lines