Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

*Note - to maintain cross-metric comparability, the purchase applications index shown in the table below represents the monthly average as opposed to the most recent weekly data point.

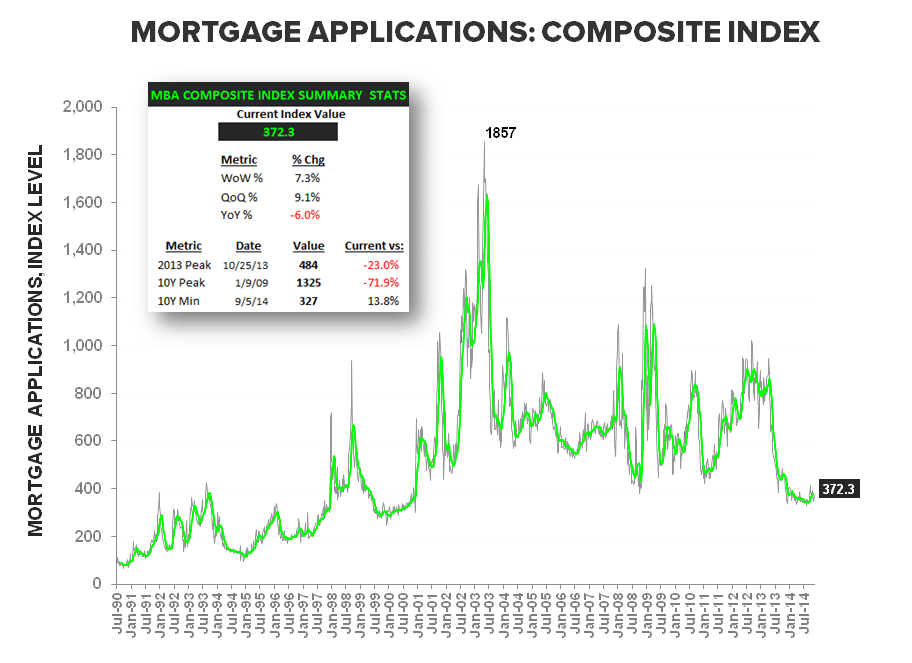

Today's Focus: MBA Mortgage Applications

The Mortgage Bankers Association today released its weekly mortgage applications survey data for the week ended December 5th.

The +7.3% increase in the Composite Index reflected a strong print from Refi and a modest uptick in Purchase.

- Purchase demand rose +1.3% WoW and the YoY rate of decline improved to -4.5% from -11% two weeks prior as the index held above the 170-level for the 4th straight week – the longest streak at that level since June. This is important as last week, while strong, was a holiday week, reducing the reliability of the data. The multi-week trend in place now shows steady, modest improvement. Compares ease further into the last few weeks of the year and take a second dive into the end of 1Q15.

- Refi activity popped +13.2%, essentially retracing the -13.4% print in the previous holiday week. Rates ticked up modestly to 4.11% from 4.08% in the week prior.

In short, “stabilization” remains the apt characterization for current HPI and purchase demand trends. Housing, like most things Macro, is more about better/worse than good/bad and while the data remains soft on an absolute basis, from a rate of change perspective, less bad is good.

About MBA Mortgage Applications:

The Mortgage Bankers’ Association’s mortgage applications index covers more than 75% of mortgage applications originated through retail and consumer direct channels. It does not include loans delivered through wholesale broker and correspondent channels. The MBA mortgage purchase applications index is considered a leading indicator of single-family home sales and construction. Moreover, it is the only housing index that is released on a weekly basis.

Frequency:

The MBA Purchase Apps index is released every Wednesday morning at 7 am EST.

Joshua Steiner, CFA

Christian B. Drake