TODAY’S S&P 500 SET-UP – December 8, 2014

As we look at today's setup for the S&P 500, the range is 41 points or 1.70% downside to 2040 and 0.27% upside to 2081.

SECTOR PERFORMANCE

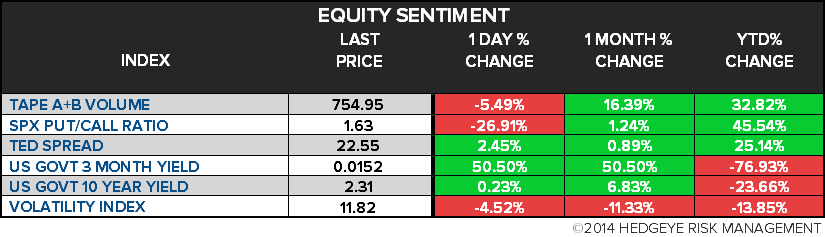

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.66 from 1.66

- VIX closed at 11.82 1 day percent change of -4.52%

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: Fed Labor Market Conditions Index Change, Nov. (pr 4)

- 12:30pm: Fed’s Lockhart speaks in Atlanta

- 11:30am: U.S. to sell $24b 3M bills, $26b 6M bills

- U.S. Rates Weekly Agenda

- FX Weekly Agenda

GOVERNMENT:

- President Obama hosts Prince William at White House

- 9:30am: Supreme Court issues orders on pending cases

- 11am: House Democrats hold conf. call briefing to discuss Trans-Pacific Partnership negotiations

- 2pm: Senate Foreign Relations Cmte hearing on authorization for use of military force against Islamic State

WHAT TO WATCH:

- Merck Said in Talks to Buy Cubist Pharmaceuticals for $7b

- CBS, Dish Reach Multiyear Content Distribution Agreement

- McDonald’s Nov. Comp. Sales Seen Falling for 6th Month

- Banks Urge Big U.S. Clients to Park Deposits Elsewhere: WSJ

- KKR, CVC Said to Lead Bidding for KFC Mideast Operator Americana

- Blackstone to Sell California Office Portfolio for $3.5b: WSJ

- Obama Tested for Sore Throat at Washington Army Hospital

- United Technologies CEO Left Amid Director Concern on Priorities

- Temasek to Buy Stake in High-Speed Trader Virtu Financial

- PetSmart Auction Said to Be Extended to Later This Week: NY Post

- China Blocks Review of Carbon Pledges Sought by U.S. at UN Talks

- Madoff Aide Hired in 1960s Will Be First to Learn Prison Fate

- China Rejects Arbitration of South China Sea Territorial Dispute

- Hostages Killed in Yemen During Rescue Mission by Special Forces

- NYC to Sell Public-Housing Stake to Developers: WSJ

EARNINGS:

- ABM Industries (ABM) 5pm, $0.57

- Diamond Foods (DMND) 4:02pm, $0.25

- H&R Block (HRB) 4:05pm, ($0.42)

- Photronics (PLAB) 4:30pm, $0.09

- Triangle Petroleum (TPLM) Bef-mkt, $0.14

- Vail Resorts (MTN) 8am, ($2.03)

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Commodity Benchmarks Seen Open to Manipulation, Law Firm Says

- Oil Slumps to Five-Year Low as OPEC Decision Spurs Forecast Cuts

- Gold Bulls Return as Wagers on Stimulus Accumulate: Commodities

- Hedge Funds Betting That OPEC-Led Oil Rout Is Near End: Energy

- Wheat Falls as Snow Seen Shielding Black Sea, U.S. Sales Slip

- Copper Drops for Second Day as Chinese Imports Unexpectedly Fall

- MORE: China Copper-Product Imports Rise to 7-Month High in Nov.

- Gold Rises for First Time in Three Days After Bullish Bets Climb

- Kuwait Plans $7 Billion Heavy-Oil Project Amid Cheaper Crude

- Trafigura Gross Margin Improves After Oil, Metals Volumes Climb

- Oil Slump Seen Driving M&A as Nordea Bank Monitors Valuations

- Algeria’s Sonatrach Says Lower Oil Price Won’t Delay Investments

- U.S. Gulf-Latin America Fuels Cargoes Rise to Record: Weber

- Rubber Rises Most in 2 Weeks as Yen at 7-Year Low Boosts Appeal

CURRENCIES

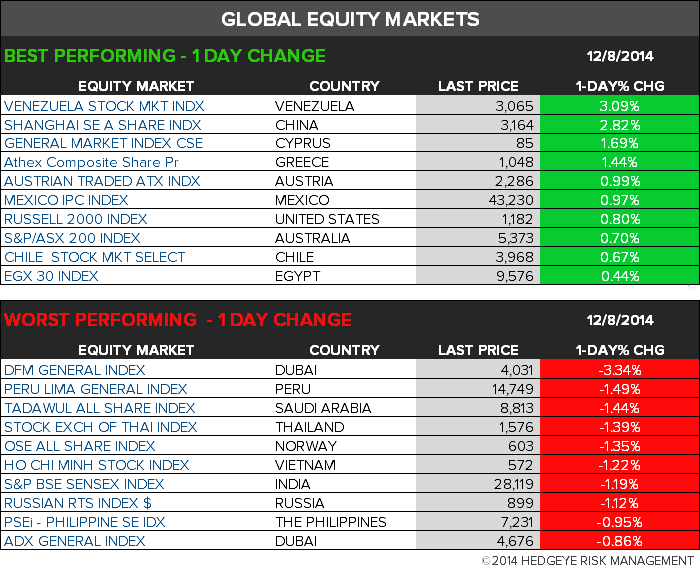

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team