Below are Hedgeye analysts’ latest updates on our six current high-conviction long investing ideas and CEO Keith McCullough’s updated levels for each.

*We also feature two pieces of content from our research team at the bottom.

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

CARTOON OF THE WEEK

IDEAS UPDATES

TLT | EDV | XLP | MUB

Labor Market, Is That All You Got?

Today was nothing shy of a historic day in the domestic labor market. November’s +321k MoM gain in Non-Farm Payrolls represented the fastest sequential pace of net job growth since January 2012. Underneath the hood, the report was solid as well:

- Growth in Average Hourly Earnings accelerated +10bps to +2.1% YoY.

- Average Weekly Hours edged up to 34.6 from 34.5 prior; per Bloomberg economists: “…a one-tenth increase in the workweek is the worker-hour equivalent of about 250k additional jobs. In other words, if the workweek was unchanged, to have the same income-effect the payroll number would have had to be 571k”.

- Growth in Total US Employees on Nonfarm Payrolls accelerated to a new cycle-high of +1.99% YoY from +1.96% prior.

Clearly the November Jobs Report was very strong and the fixed income market reacted as such, with the 10Y Treasury bond yield shooting up from 2.24% to 2.33% immediately following the release. It closed the day at 2.30%. 2Y Treasury note yields also shot up around ~10bps immediately following the release of the employment figures, closing just shy of its highs of the day at 0.64%.

The movement in the 10Y yield coincided with a -0.58% DoD return for the TLT and -0.38% return for the EDV. Considering today’s massive rip in employment growth, these moves seem quite a bit muted.

In fact, these returns are only in the 22nd and 34th percentiles of daily returns on a trailing 3Y basis, respectively; one would think they’d be in the bottom-10 percent given this major step forward in the domestic labor market. The fact that both ETFs closed UP on the week (+0.2% and +0.4%, respectively) is actually quite stunning in the context of the aforementioned labor data.

So what gives?

We think this golf clap of a return for Consensus Macro bond bears is the market effectively trying to communicate that the Fed isn’t going to hike interest rates anytime soon – or quite possibly ever under the tenure of Janet Yellen!

That’s certainly what our proprietary G3 Monetary Policy Model is suggesting. In fact, this model actually suggests there’s a fairly high probability that the Fed gets easier over the next 3-6 months, given that its score is similar to the ECB’s, which continues to set the table for open-ended LSAP.

At a bare minimum, this implies ZIRP is likely to remain in place for longer than most investors currently expect. And the longer we hang out at 0-25bps on the Fed Funds Rate, the higher the likelihood that we enter a economic downturn. As this late-cycle labor market strength ominously implies, the clock is ticking on this economic recovery, which is slightly long in the tooth by historical standards. Moreover, the labor market actually tends to peak about ~7 months prior to the start of the recession, effectively forestalling an easier Fed along the path towards economic gravity.

All told, while we do not think it’s appropriate to make the “recession” call just yet, we still think the path of least resistance for interest rates remains lower over the intermediate-term. That’s a favorable setup for long-term Treasuries, munis and for investors seeking yield pickup in the equity market (healthcare, consumer staples, utilities and REITs).

HCA

Hospital Corporation of America hit a new 52-week high this week and is up approximately +12% since we added it to Investing Ideas on 11/7.

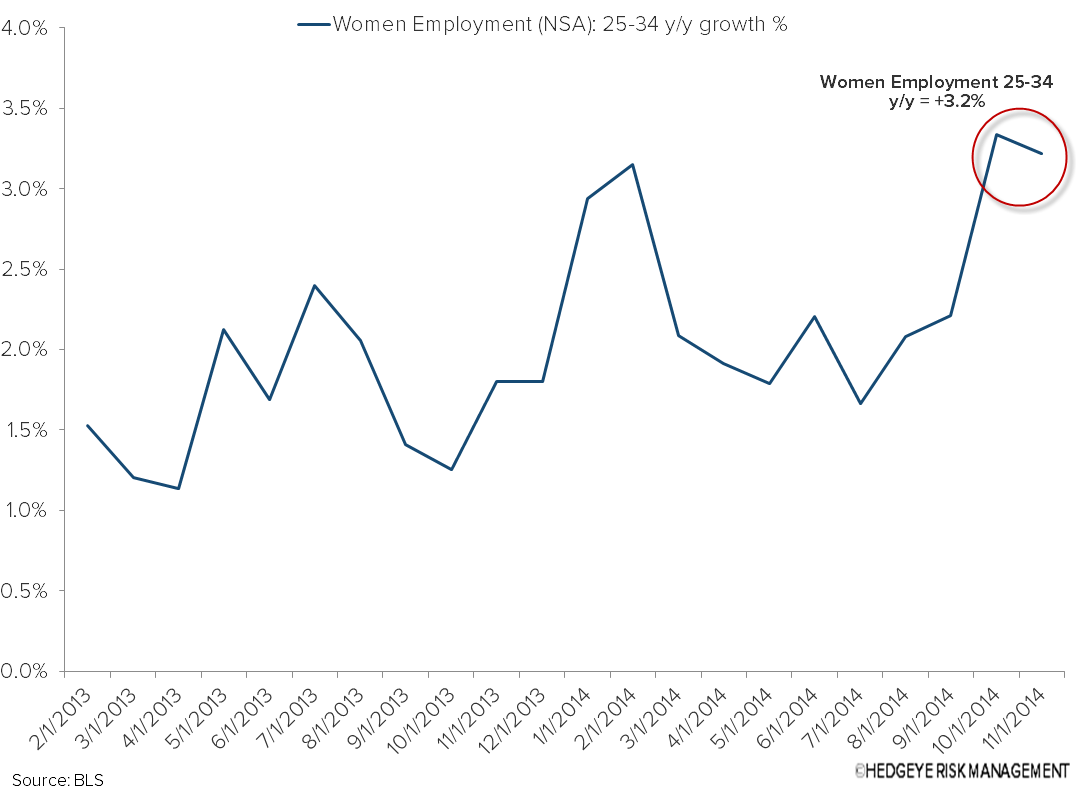

We track 25+ data series that drive the fundamentals of HCA in our Hospital Monitor (see below). Three of those series were updated today with the release of the November Jobs report. Women Employment Age 25-34 continues to trend positively y/y, despite slowing in rate of change terms from the October release. This series is important because it has a high correlation with births, as an increase in employment corresponds to greater insured population (more women can afford to have a child).

Meanwhile, Hospital Employment was strong and continues to accelerate y/y, which correlates well to same store metrics. Results of our November OB/GYN survey will be in next week and provide us with an update in utilization trends.

RH

Restoration Hardware is set to report earnings on Wednesday December 10. We’re comfortable with our above-consensus estimate of $0.52 versus the Street at $0.46.

We think that the top line will be particularly important this quarter given the miss we saw in 2Q when sales only grew at 13.5%, due to problems that RH had with consolidating its 13 Sourcebooks (catalogs) into one colossal 3300 page shrink-wrapped mailing. We’re looking for an acceleration of about 1,000bp in sales growth in this quarter alone.

The company will be switching it up this quarter in a way that we think is a positive. Once its 8K is filed, they’ll post a video presentation highlighting the Company’s ‘continued evolution and recent performance’ on the RH Investor Relations website (approximately 1:30 pm Pacific/4:30 pm Eastern). Then they’ll host a live Q&A session at 2:30 pm Pacific/5:30 pm Eastern.

This one should be a winner.

* * * * * * * * * *

ADDITIONAL RESEARCH CONTENT BELOW

the clock is ticking for bob evans (bobe)

We continue to believe BOBE represents an under-the-radar special situation story.

ici fund flow survey: a closer eye on etfs

Mutual fund activity during the past 5 days continued to be subdued, giving way to more robust trends in exchange traded funds.