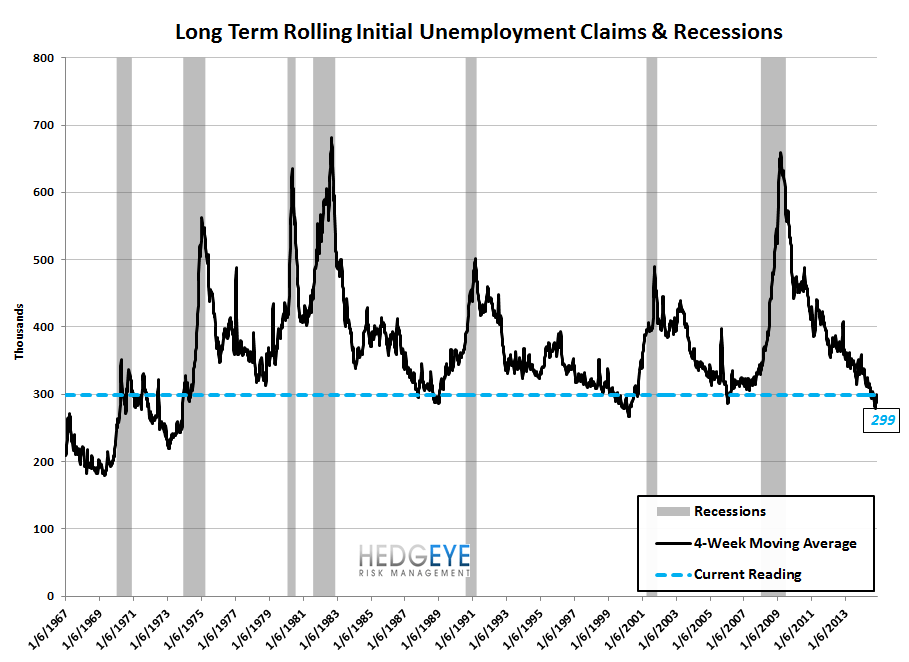

Steady

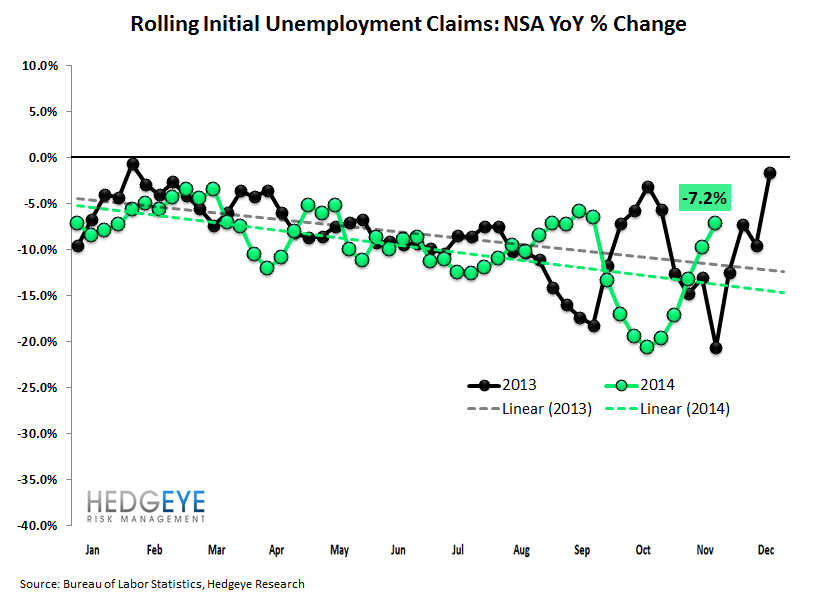

The main takeaways from this week's labor report are that the trend of sub-300k claims persists, further reducing the slack in the labor market. While the y/y rate of change is slowing, this is to be expected as that series will naturally converge toward zero since 300k is the frictional bottom for claims. In other words, the data is strong and consistent even thought the rate of positive change is slowing. What we're more interested in, at this point, is any signs of an unfavorable inflection. If the rate of change begins to turn positive (i.e. rising claims) or materially diverges from the trendline then all (long) bets are off.

The Data

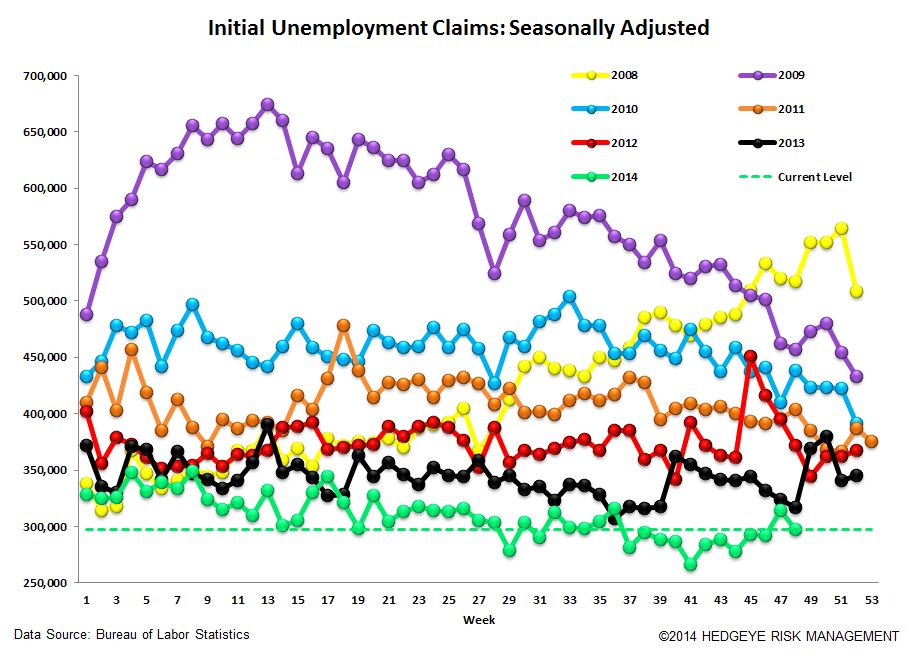

Prior to revision, initial jobless claims fell 16k to 297k from 313k WoW, as the prior week's number was revised up by 1k to 314k.

The headline (unrevised) number shows claims were lower by 17k WoW. Meanwhile, the 4-week rolling average of seasonally-adjusted claims rose 4.75k WoW to 299k.

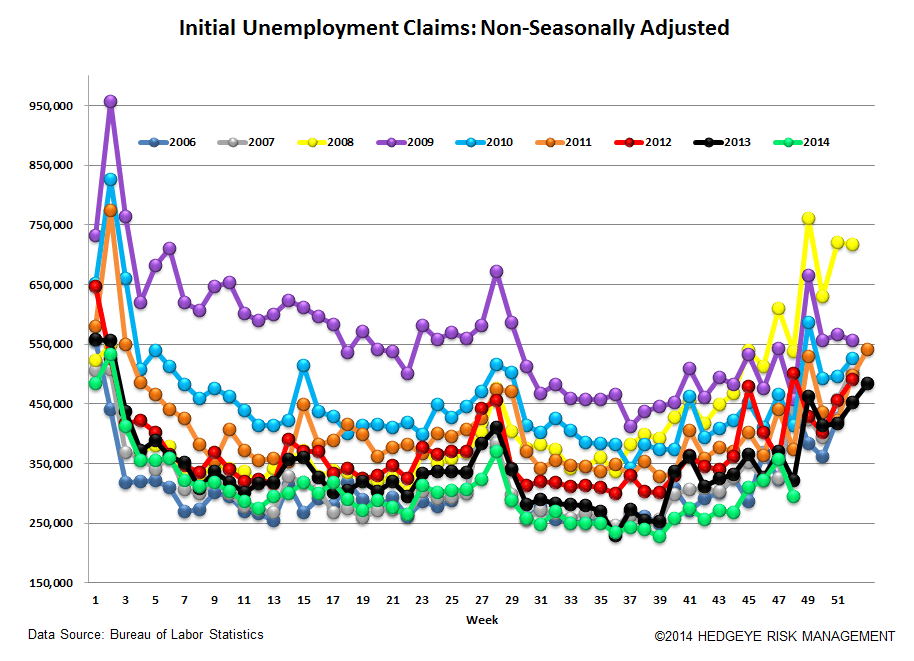

The 4-week rolling average of NSA claims, which we consider a more accurate representation of the underlying labor market trend, was -7.2% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -9.8%

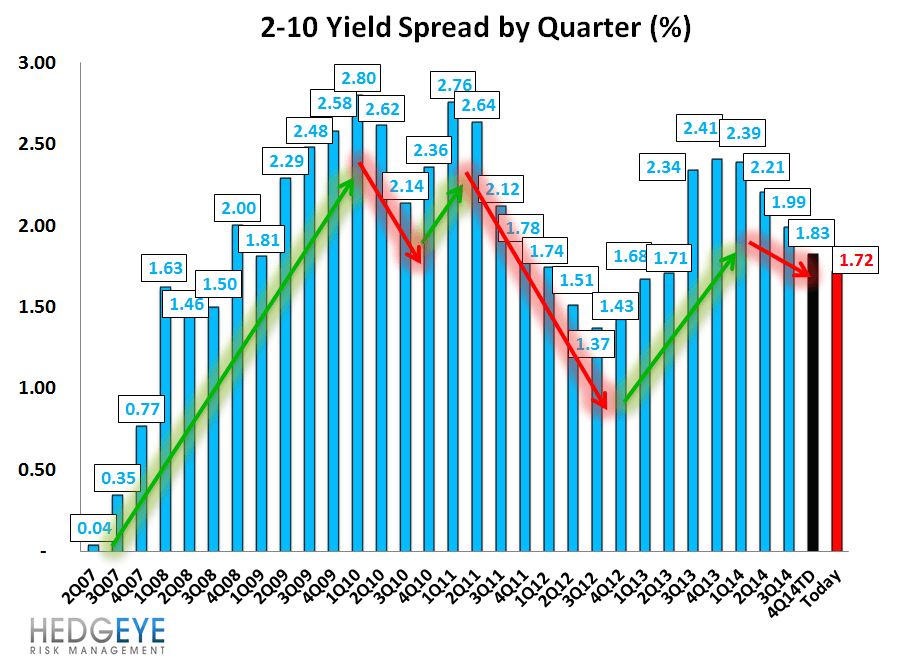

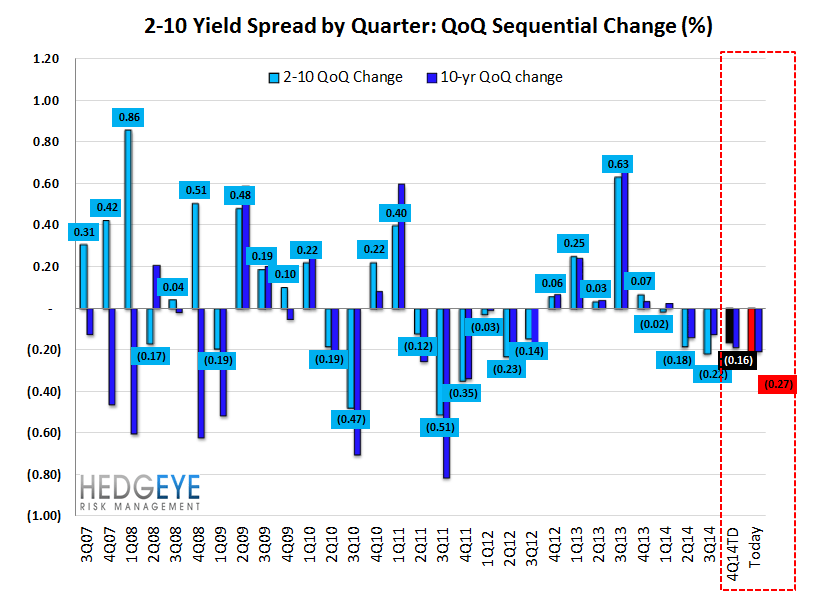

Yield Spreads

The 2-10 spread fell 0 basis points WoW to 172 bps. 4Q14TD, the 2-10 spread is averaging 183 bps, which is lower by -16 bps relative to 3Q14.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT