The Q2/Q3 meltup in US stocks has been one of the most expedited in US stock market history. Where does the free money momentum ride associated with an easy Fed end? Well, when the ZERO rate policy does. And we’re closer to that date today, than we were yesterday…

See my Early Look titled “3-Some” for the why on this, but the reality is that if the Buck stops Burning in October, stocks will stop REFLATING. I call this Reflation’s Rotation.

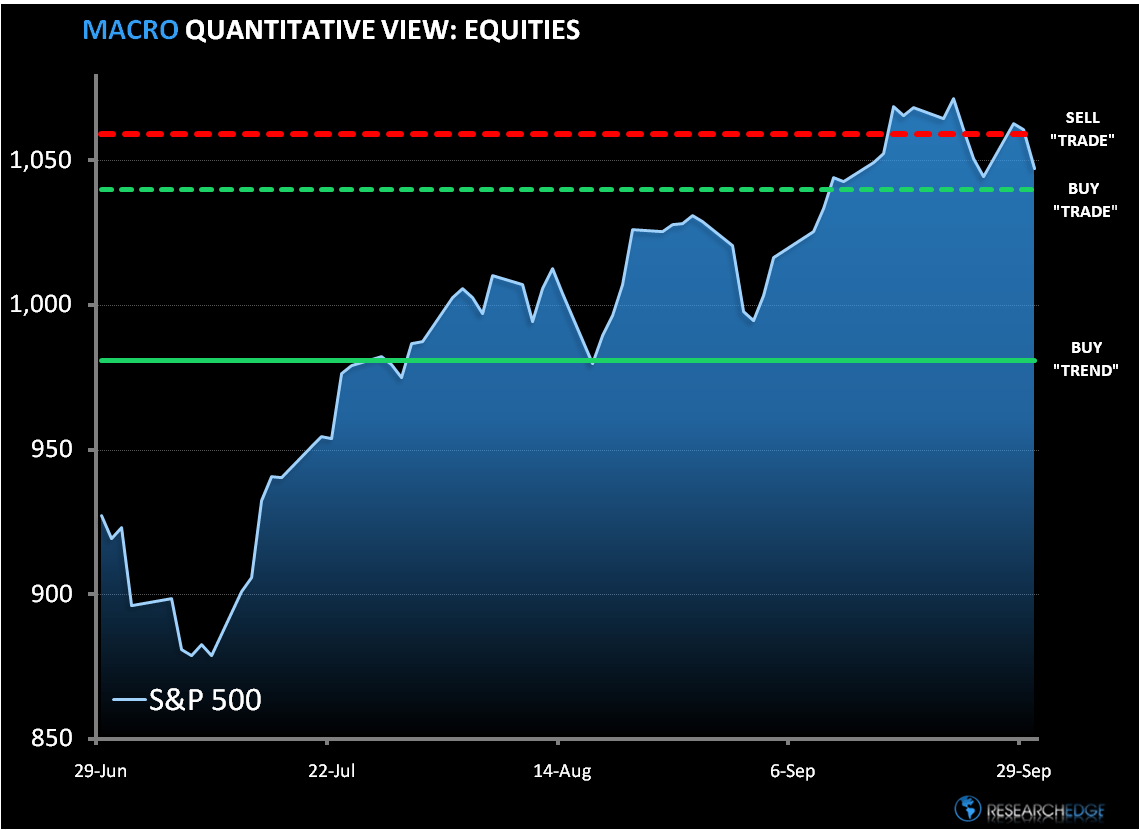

In terms of risk management levels, there is an important support line that needs to hold for the SP500’s positive price momentum to continue (1060, dotted red). That 1060 line just cracked. There is significant support at the immediate term TRADE line (1040, dotted green line), so don’t get in a heat about this, yet…

Given that today is quarter end, I think the large part of today’s move is behind us. Bullish formations need corrections in order to continue. A breakdown through 1040 combined with a breakout of the US Dollar above the $77.39 line is something that I’ll get in a heat about.

For now, this is simply a small crack in this Bullish Formation’s wall. Stay tuned.

KM

Keith R. McCullough

Chief Executive Officer