Our Hedgeye Housing Compendium table (below) aspires to present the state of the housing market in a visually-friendly format that takes about 30 seconds to consume.

*Note - to maintain cross-metric comparability, the purchase applications index shown in the table below represents the monthly average as opposed to the most recent weekly data point.

Today's Focus: MBA Mortgage Applications

The Mortgage Bankers Association today released its weekly mortgage applications survey data for the week ended November 28th.

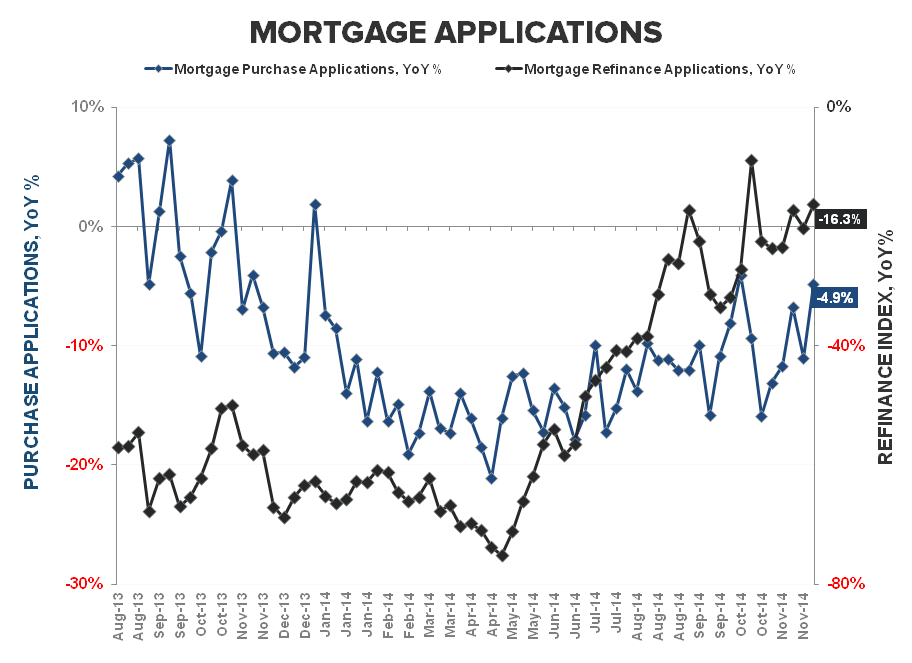

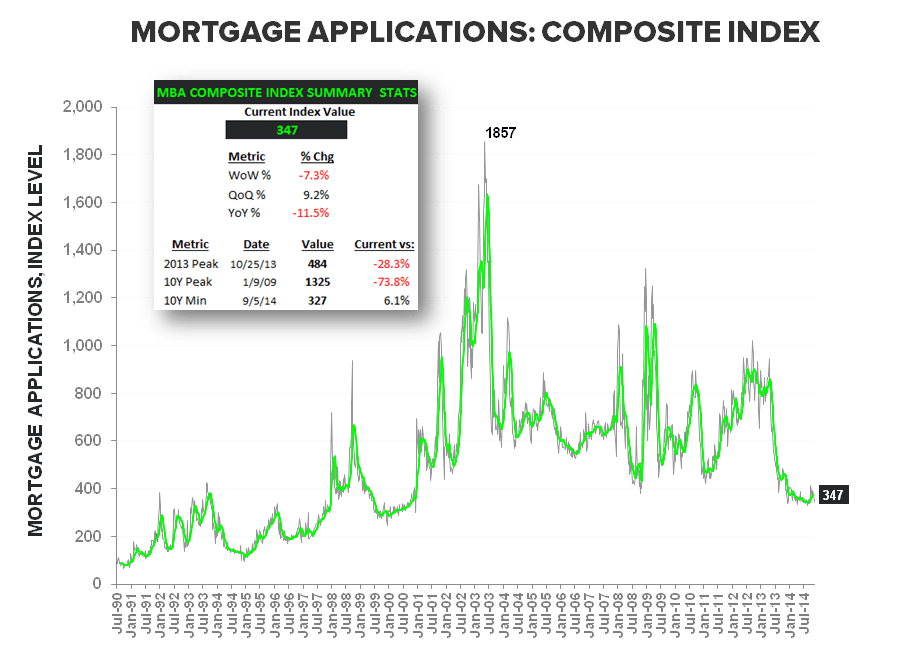

The -7.3% decline in the Composite Index belied more sanguine growth on the purchase side where demand rose +2.5% sequentially.

- Purchase demand rose +2.5% WoW and the YoY rate of decline improved to -4.9% from -11% prior as the index held above the 170-level for the 3rd straight week – the longest streak at that level since June. We don’t take a convicted view of holiday week data in isolation but the multi-week trend has been one of modest improvement. Compares ease further into the last few weeks of the year and take a second dive into the end of 1Q15.

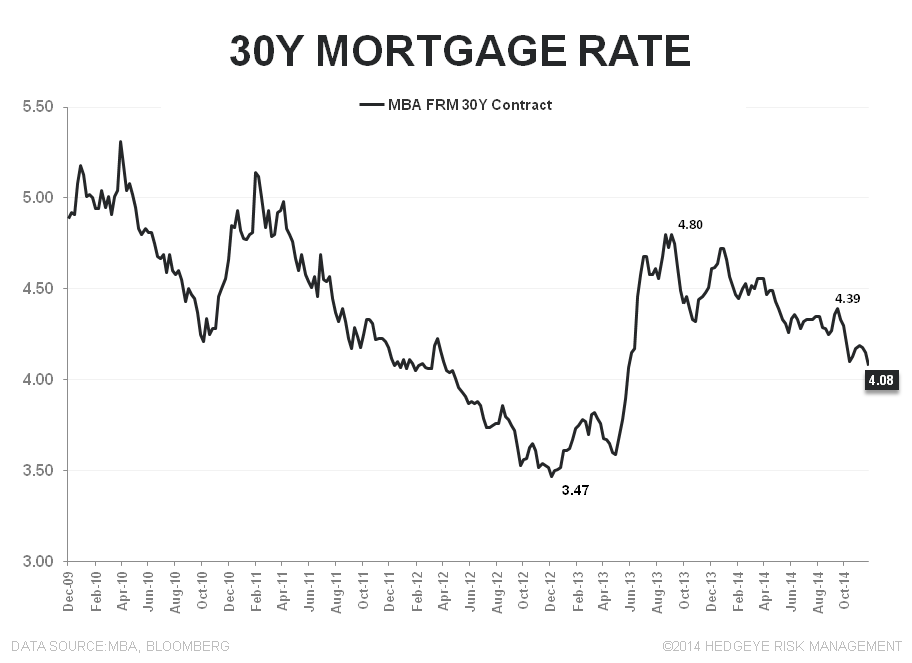

- Refi activity declined -13.4% sequentially despite the retreat in rates with the holiday/seasonals providing some measure of distortion. Rates on the 30Y FRM contract dropped -7bps to 4.08% - the lowest rate YTD and lowest since May of last year.

In short, “stabilization” remains the apt characterization for current HPI and purchase demand trends. Housing, like most things Macro, is more about better/worse than good/bad and while the data remains soft on an absolute basis, from a rate of change perspective, less bad is good.

About MBA Mortgage Applications:

The Mortgage Bankers’ Association’s mortgage applications index covers more than 75% of mortgage applications originated through retail and consumer direct channels. It does not include loans delivered through wholesale broker and correspondent channels. The MBA mortgage purchase applications index is considered a leading indicator of single-family home sales and construction. Moreover, it is the only housing index that is released on a weekly basis.

Frequency:

The MBA Purchase Apps index is released every Wednesday morning at 7 am EST.

Joshua Steiner, CFA

Christian B. Drake