TODAY’S S&P 500 SET-UP – December 3, 2014

As we look at today's setup for the S&P 500, the range is 46 points or 1.67% downside to 2032 and 0.55% upside to 2078.

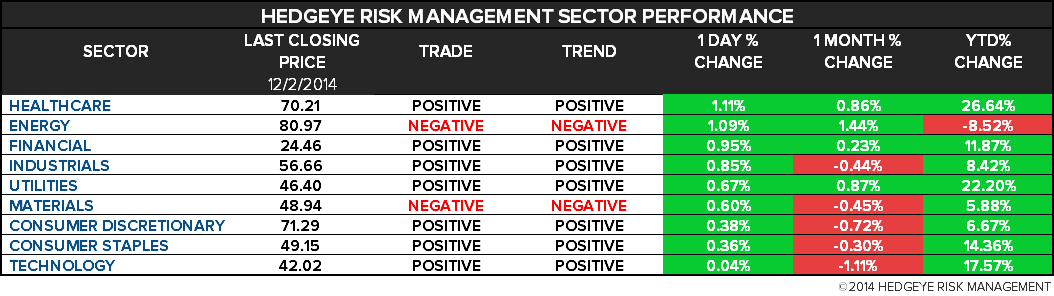

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.75 from 1.76

- VIX closed at 12.85 1 day percent change of -10.08%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Nov. 28 (prior -4.3%)

- 8:15am: ADP Employment Change, Nov., est. 222k (prior 230k)

- 8:30am: Nonfarm Productivity, 3Q final, est. 2.4% (prior 2%)

- 9:45am: Markit US Svcs PMI, Nov. final est. 56.5 (prior 56.3)

- 10am: ISM Non-Manf. Composite, Nov., est. 57.5 (prior 57.1)

- 10am: Bank of Canada seen maintaining 1% overnight lending rate

- 10:30am: DOE Energy Inventories

- 12:30pm: Fed’s Plosser speaks in Charlotte, N.C.

- 2pm: Federal Reserve releases Beige Book

- 2pm: Fed’s Brainard speaks in Washington

- 7:30pm: Fed’s Fisher speaks in Dallas

GOVERNMENT:

- President Obama to address Business Roundtable Forum

- 2:30pm: JPMorgan CEO Dimon, Exxon CEO Tillerson speak

- 9am: U.S. Chamber of Commerce event on future of financial reporting, auditing profession, w/ PCAOB Chairman James Doty; James Schnurr, SEC chief accountant

- 10am: House Energy and Commerce Cmte hearing on Takata airbag recalls, with testimony from Hiroshi Shimizu, Takata SVP of global quality assurance

- 10am: Supreme Court considers arguments in case over right of pregnant workers to be temporarily given new job duties

- 10am: Senate Environment and Public Works Cmte hearing on Nuclear Regulatory Commission’s implementation of Fukushima task force recommendations

WHAT TO WATCH:

- Fed Officials Stress Data Over Dates as Rate Rise Case Builds

- China Services Gauges Climb in Nov. in Support to Growth

- Euro-Area Economy Weakens as ECB Considers Stimulus Options

- Apple Pay Partner Stripe Valued at $3.5b in New Funding

- Cyber Monday Online Sales Rose 17% to $2b, ComScore Says

- Takata Poised for Clash in Congress After Rejecting U.S. Recall

- Chrysler-Led U.S. Auto Industry Gains to 17.2m Annual Pace

- Huntington Poised for $4b U.S. Aircraft Carrier Award in 2015

- Prudential Financial to Take $494m Charge, Buy Back Debt

- Sony’s Unreleased ‘Annie’ Said Pulled From Sharing Websites

- KKR, CJ Korea, XPO Said Shortlisted for NOL Logistics Unit

- N. Korea’s Fingerprints Said Found in Malware Crippling Sony

AM EARNS:

- Abercrombie & Fitch (ANF) 7am, $0.41

- Brown-Forman (BF/B) 8am, $1.04

- Leidos (LDOS) 6am, $0.53

- Royal Bank of Canada (RY CN) 6am, C$1.59 - Preview

PM EARNS:

- Aeropostale (ARO) 4:01pm, ($0.45)

- Avago Technologies (AVGO) 4:02pm, $1.70

- Canadian Western Bank (CWB CN) 7:30pm, C$0.68

- Guess? (GES) 4:03pm, $0.18

- Pacific Sunwear (PSUN) 4pm, ($0.04)

- PVH (PVH) 4:02pm, $2.48

- Seachange (SEAC) 4:01pm, ($0.08)

- Synopsys (SNPS) 4:05pm, $0.61

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Brent Crude Trades Near $70 as Traders Assess OPEC Decision

- ICE Targets Asia With Yuan, Crude Futures Set for Singapore

- Gold Volatility Reaches 9-Month High on Oil Whipsaw: Commodities

- Gold Climbs as Oil Gains and Physical Demand Picks Up in Asia

- Zinc Swings as Investors Weigh Dollar Against U.S. Auto Sales

- Citigroup Panicked Over Fraud at Chinese Ports, Mercuria Says

- Oil Price Plunge Lends Unexpected Hand to Ailing Southern Europe

- CME Delays Hong Kong Gold Futures Start to First Quarter of 2015

- Palm Oil Advances for Second Day as Crude Oil, Soybeans Rebound

- Rubber Declines as Lower Oil Reduces Costs for Synthetic Product

- Western Canadian Energy Regulators Unite Amid Pipeline Delays

- Cliffs Agrees to Sell West Virginia Coal Mines for $175 Million

- White Sugar Falls to 5-Year Low After Oil’s Drop; Coffee Rises

- Constitutional Court in Indonesia Upholds Mineral Ore Export Ban

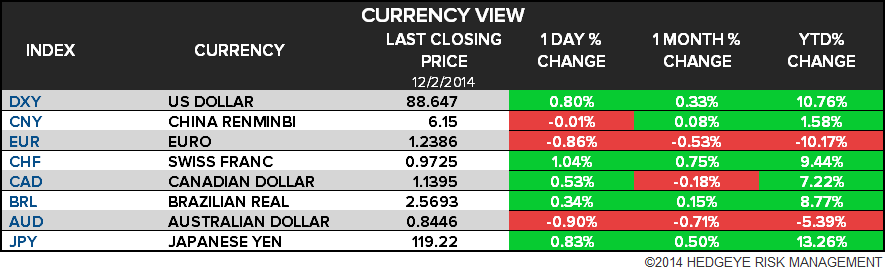

CURRENCIES

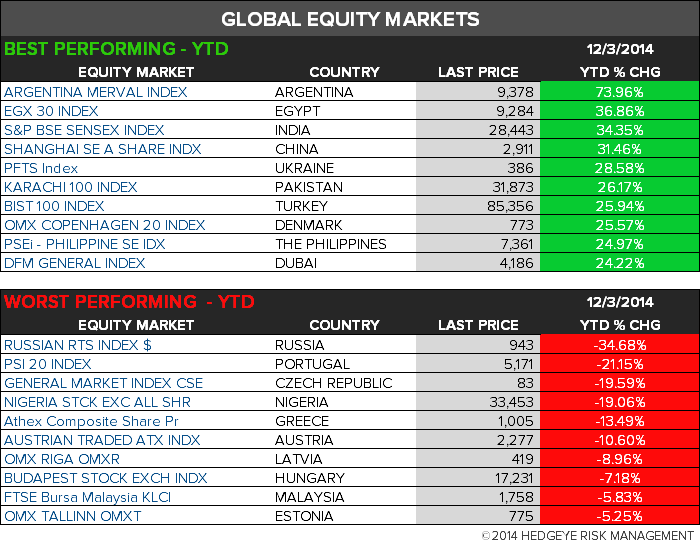

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team