Current Ideas:

Key Takeaway:

Russia remains a major area of global risk exposure. Russia's largest bank, Sberbank, which holds roughly half of all retail deposits for the country, is now trading at over 400 bps on its credit default swaps. The "danger zone" is generally regarded as anything north of 300 bps. With oil continuing to plunge following OPEC's move to drive marginal shale producers out of business, the embedded risk in Russia's banking system is growing quickly. Consider this simple example. Energy still accounts for 20-25% of Russia's GDP, and energy prices have fallen ~30% in the last two months. Multiplying those two weightings would imply that Russia's economy is at risk of suffering a decline of 6-7.5%. Compare that with the 8.2% decline experienced by the US Economy in 4Q08 during the height of the US Great Recession.

The XLF rose 0.78% last week, as stocks rose globally, outperforming the S&P 500, which rose 0.2%. The Global Dow rose 0.07%. Financials are performing well in 2014 at +11.6%, right in the middle of sector performance with Healthcare the highest (+25.6%) and Energy the lowest (-9.8%).

Financial Risk Monitor Summary

• Short-term(WoW): Positive / 6 of 12 improved / 1 out of 12 worsened / 5 of 12 unchanged

• Intermediate-term(WoW): Positive / 5 of 12 improved / 3 out of 12 worsened / 4 of 12 unchanged

• Long-term(WoW): Positive / 2 of 12 improved / 0 out of 12 worsened / 10 of 12 unchanged

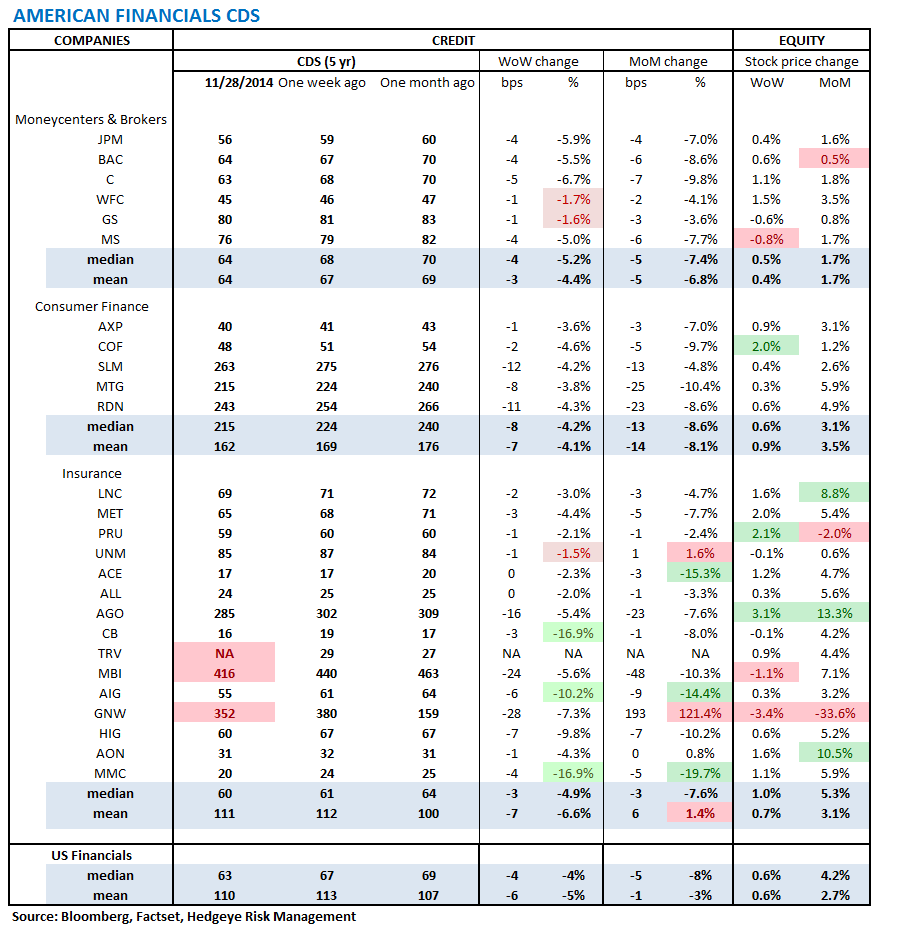

1. U.S. Financial CDS - Swaps showed broad tightening last week with CDS for 25 out of 27 domestic financial institutions tightening.

Tightened the most WoW: CB, MMC, AIG

Widened the most/ tightened the least WoW: UNM, GS, WFC

Tightened the most MoW: MMC, ACE, AIG

Widened the most MoM: GNW, TRV, UNM

2. European Financial CDS - Swaps also were mostly tighter in Europe last week. At the median, European swaps tightened by -8.5%. Only Greek and Russian bank CDS widened modestly: Greece by about 3.1% and Russia by 2.5%. We would call out Russia's Sberbank, which is now north of 400 bps, reflecting the rising risk in the Russian economy.

3. Asian Financial CDS, similar to other global markets, tightened last week. The Chinese stock market had its best week in four years, and the Bank of China showed the second biggest tightening in the Asian market.

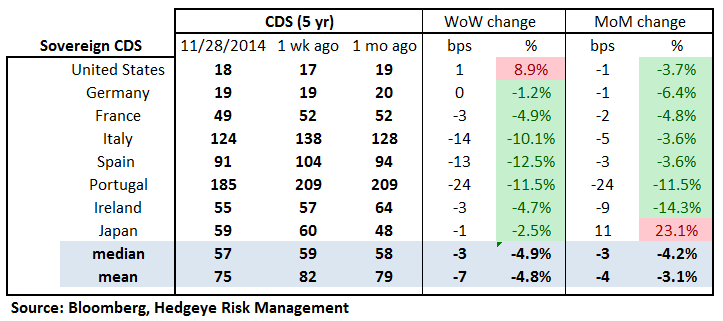

4. Sovereign CDS – Sovereign swaps mostly tightened over last week. Spanish sovereign swaps tightened by -12.5% (-13 bps to 91 ) and American sovereign swaps widened by 8.9% (1 bps to 18).

5. High Yield (YTM) Monitor – High Yield rates rose 3.4 bps last week, ending the week at 6.14% versus 6.10% the prior week.

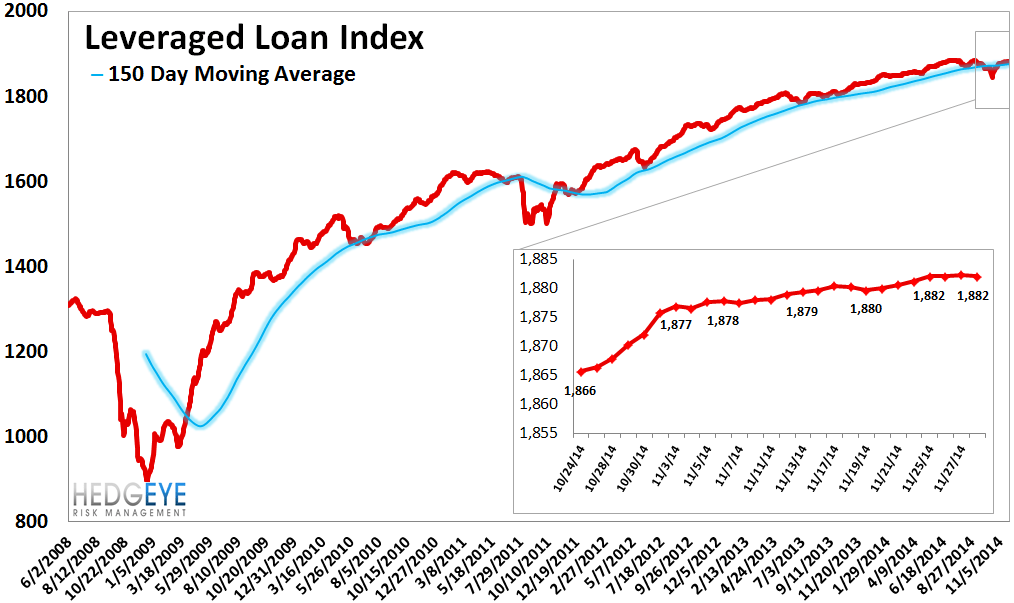

6. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 1.0 points last week, ending at 1882.

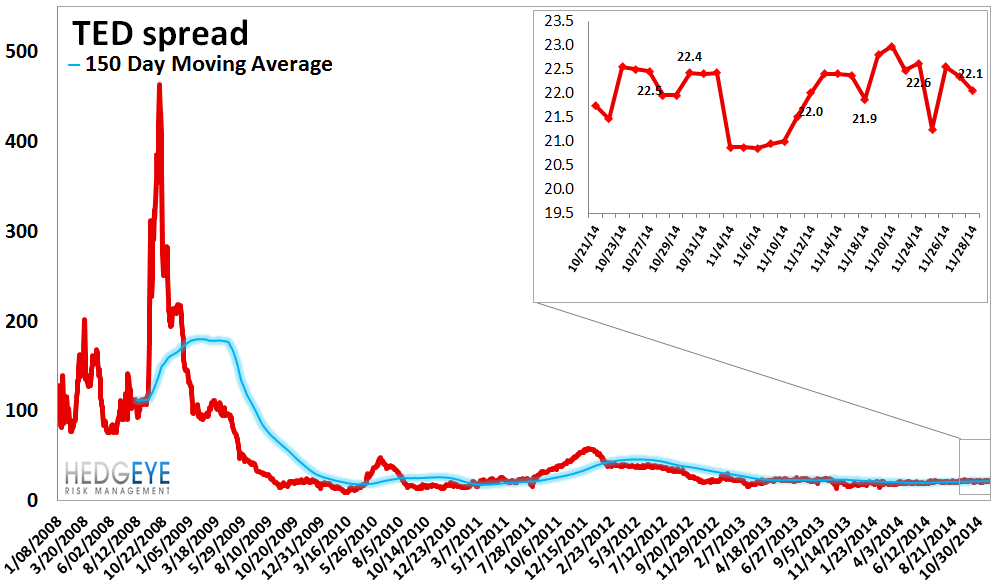

7. TED Spread Monitor – The TED spread fell 0.4 basis points last week, ending the week at 22.1 bps this week versus last week’s print of 22.49 bps.

8. CRB Commodity Price Index – The CRB index fell -4.5%, ending the week at 254 versus 266 the prior week. As compared with the prior month, commodity prices have decreased -6.7% We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

9. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 2 bps to 8 bps.

10. Chinese Interbank Rate (Shifon Index) – The Shifon Index fell less than 1 basis point last week, ending the week at 2.58%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

11. Chinese Steel – Steel prices in China fell 0.6% last week, or 17 yuan/ton, to 2948 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity, and, by extension, the health of the Chinese economy.

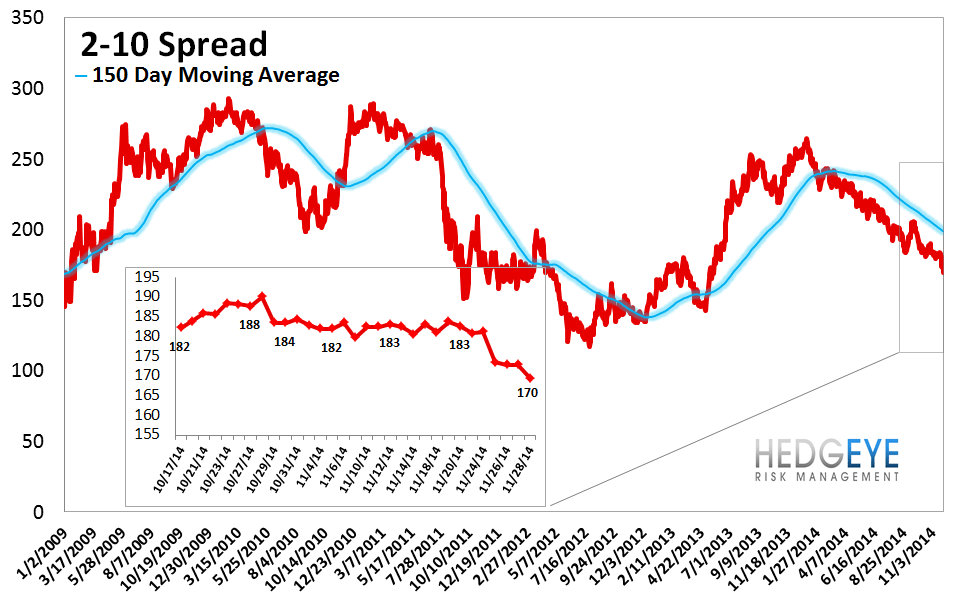

12. 2-10 Spread – Last week the 2-10 spread tightened to 170 bps, -11 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

13. XLF Macro Quantitative Setup – Our Macro team’s quantitative setup in the XLF shows 0.5% upside to TRADE resistance and 0.9% downside to TRADE support.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT