TODAY’S S&P 500 SET-UP – November 28, 2014

As we look at today's setup for the S&P 500, the range is 45 points or 1.87% downside to 2034 and 0.30% upside to 2079.

SECTOR PERFORMANCE

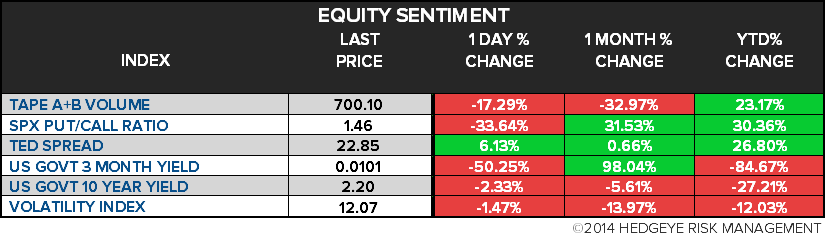

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.70 from 1.73

- VIX closed at 12.07 1 day percent change of -1.47%

MACRO DATA POINTS (Bloomberg Estimates):

- No major economic reports scheduled

GOVERNMENT:

- House, Senate not in session

- No events of note expected

WHAT TO WATCH:

- OPEC Takes No Action to Ease Supply Glut as Crude Oil Slumps

- Crude Oil Heads for Biggest Weekly Tumble Since 2011

- Thanksgiving Deal Hunt Draws Millions Away From Dinner in U.S.

- Wal-Mart Says >22m Customers Visited Its Stores on Thanksgiving

- Tokyo Electron, Applied Materials Merger Date Delayed to March

- Enbridge to Buy 80% of E.On U.S. Wind Portfolio

- Pfizer, Astra Deal May Have Failed on Tax, Soriot Says: CNBC

- Euro Inflation Slows to 0.3% as ECB Poised to Discuss Stimulus

- U.S. Jobs, Services, ECB, BOE, NATO: Week Ahead Nov. 29-Dec. 6

- U.S. equity markets close at 1pm, bond markets close at 2pm

EARNINGS:

- No earnings expected from S&P 500

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Oil Seen in New Era as OPEC Won’t Yield to U.S. Shale: Energy

- Oil Steadies After OPEC Triggers Biggest Slump in Three Years

- Iron on ‘Fast Forward’ as Goldman Sees Risk of Price Outlook Cut

- Commodities Slump to Five-Year Low as Crude Oil Drops on OPEC

- OPEC Inaction Signals Pain for Refiners With Costly Oil in Tanks

- Iron Ore Climbs 1.9% to $71.32/Dry Ton, Highest Since Nov. 18

- Oil Price Drop After OPEC Decision Is ‘Terrible’: Iraq Minister

- Platinum, Palladium Price Fixings Make Way for Electronic System

- CARBON: EU Benchmark Allowances Head for Biggest Gain Since June

- Indonesia’s ‘Toothless’ Policy for Biofuel Seen Hurting Palm Oil

- Copper Traders Are Bullish on Expectation Stimulus to Aid Demand

- Wheat in France at Risk of Yellow Rust Outbreak in 2015: Arvalis

- Palm Drops to One-Month Low as Crude Slump Curbs Biofuel Demand

- China Said to Order Companies to Check Risks in Commodity Trades

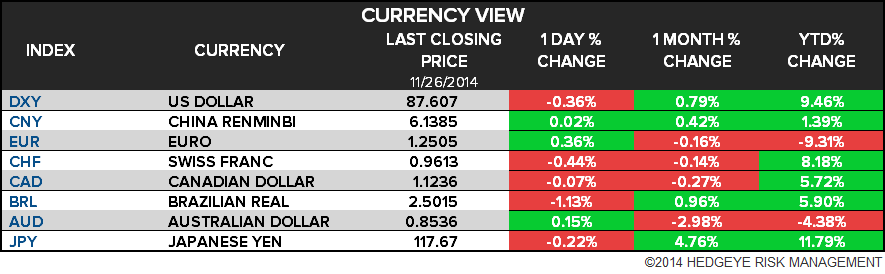

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

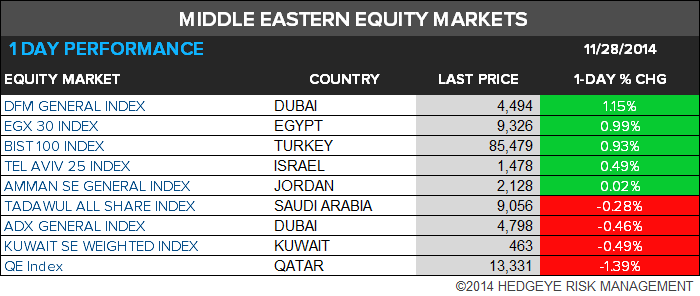

MIDDLE EAST

The Hedgeye Macro Team