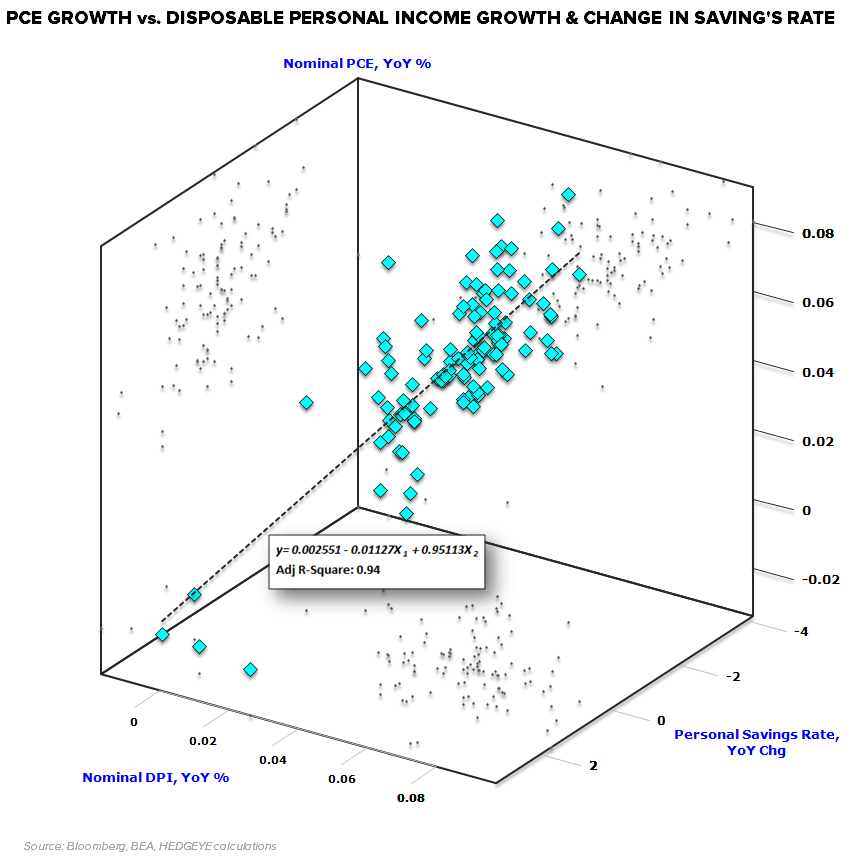

As the 3-D scatterplot below shows, the multiple regression between Disposable Personal Income growth and the change in the Savings Rate (independent variables) vs. the change in Consumer Spending (dependent variable) has an R-square of 0.95 across decades of data. More simply, growth in Disposable Income and the change in the Savings Rate explains ~95% of the change in aggregate household spending.

As we distilled it in our institutional note on Friday:

If ya don’t have it (no savings), ya ain’t gettin it (wages), and ya ain’t borrowing it (credit)…ya can’t spend it (PCE).