“If we can get you a car in 5 minutes, we can get you anything in 5 minutes.”

-Travis Kalanick

Travis, how about a massage? Or some turkey day beers and, bonds?

Everyone who has created an anti-consensus company likes how the CEO of Uber, Travis Kalanick, rolls. If this morning’s headlines about T Rowe’s investment are right, it looks like Uber is going to price its final private round at a $35-40B valuation too!

That’s almost as bullish as I am in 2014… on the Long Bond (TLT). In less than 3 minutes, I can get you anything you need to explain the bull case. As growth and inflation expectations slow, globally, bond yields go lower. Ok, maybe that was less than 1 minute.

Back to the Global Macro Grind…

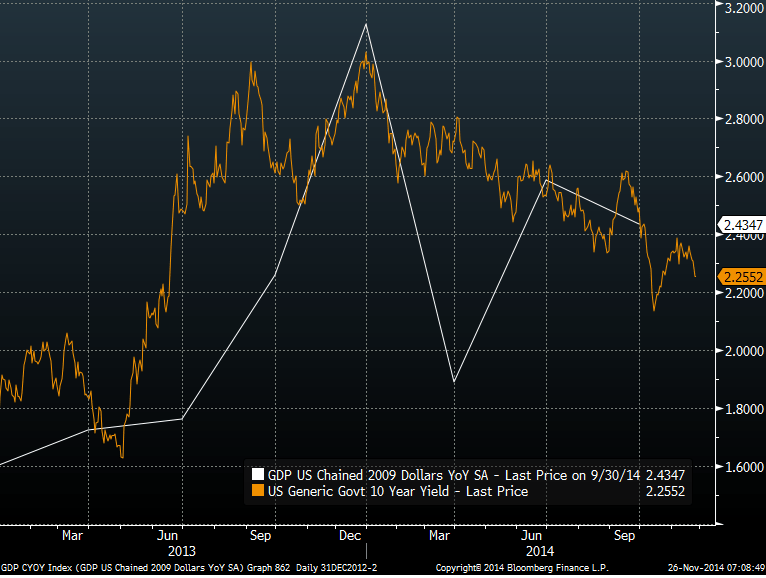

In less than 1 minute, I can get you a chart (see Chart of The Day) showing the Rate of Change in US growth versus the 10yr bond yield. Unless you are paid to navel gaze at the “Dow”, this macro relationship is obvious to all but the willfully blind.

To most of our “rate of change” fans, the year-over-year rate of change in growth and inflation are pretty basic concepts. To Consensus Macro (and the financial media that dotes on it), not so much…

Yesterday’s Consensus Media headlines on US GDP were classic. Sadly, Bloomberg (who we pay a lot of money to for rate of change data), continued down the all-time-CNBC-ratings-lows-perma-SPY-bull-spin-path by writing:

BREAKING: “SP500 Little Changed Near Record On GDP, Consumer Confidence”

In other real-world news yesterday, “Consumer Confidence” actually tanked (falling to 88.7 in NOV from 94.5 in OCT), and the rate of change in year-over-year US GDP growth slowed (again) to 2.4% in Q3 versus 2.6% in Q2.

#PermaBull says pardon?

Yes. Evolve your process, just a little, and stop staring at a next to useless GDP quarter-over-quarter SAAR (sequentially/seasonally adjusted) report and look at it how you look at the companies you invest in (i.e. on a year-over-year basis).

This isn’t rocket science. I can get you these numbers (and a whole lot more of them) in less than 3 minutes!

Again, to review why US bond yields continue to crash (10yr yield -26% YTD to 2.25% this morning):

- After topping at +3.1% year-over-year growth in Q4 of 2013, Q314 US GDP growth slowed to +2.4% and…

- While the +1.9% year-over-year growth report for Q1 was much uglier than the +3-4% “expected”…

- You can look forward to a Q4 GDP growth print in 2014 that is closer to +1.9% than Q3’s 2.4% was

Put another way, we still have US GDP growth (year-over-year dammit!) tracking to +2.2% for 2014 – and, magically, that’s exactly where the 10yr US Treasury Yield is trading this morning.

#Tah-dah! Get growth’s rate of change right – and you get bond yields right.

My inbox is fun. I often get forwarded other people’s macro work and, most of the time, I can’t particularly understand what it means. Mostly, I think that’s because I only care about rates of change. And most of that work doesn’t.

It’s not personal. It’s simply my perspective. And it’s this anti-consensus process and perspective that had us as bearish on the Long Bond in 2013 (when the rate of change in US growth was #accelerating) as we are Uber Bullish now.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.22%-2.33%

SPX 2020-2074

RUT 1154-1190

VIX 12.16-15.62

Yen 117.20-119.16

WTI Oil 73.03-77.04

Copper 2.94-3.01

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer