Tickers: HLT, NCLH, CCL

EVENTS

- Dec 1: 8:30 am IKGH Q3 earnings

- Dec 2: 11 am ISLE Q2 2015 earnings

- Dec 8: 10:30 MTN Q1 2015 earnings

- Dec 12: Trump Taj Mahal Closing

- Dec 17: Upstate NY casino decision

COMPANY NEWS

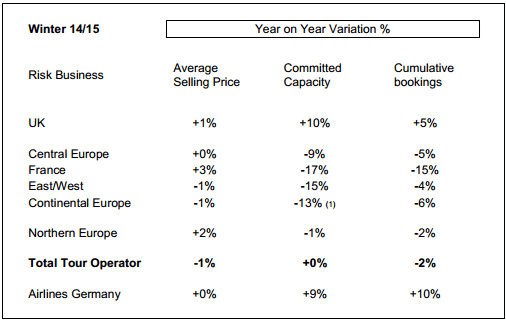

TCG.LN – Thomas Cook offered a less optimistic outlook for its forward bookings for 2015. Winter bookings are now expected to be down 2%. However, Thomas Cook is more encouraged about its Summer 2015 booking cycle, led by its UK business (UK: bookings up 8%, prices +1%). Thomas Cook also announced that its CEO, Harriet Green, has stepped down from the business and will be replaced by COO, Peter Fankhauser, who will take over with immediate effect.

Takeaway: Thomas Cook's lowered outlook is an indication of weaker demand leisure trends in Europe particularly in the next 3-6 months. It seems that the UK, and only the UK, is leading the growth in Europe. This news does not bode well for the European business for the cruisers and lodgers in the near-term.

HLT – Hilton Worldwide Middle East and Africa has launched its annual Winter Sale, offering travelers an opportunity to save up to 33% on their stays throughout 2015.

HLT – The Maui Lu Resort, a hotel development in Hawaii, sold to Japan-based Capbridge Group for an estimated $60 million. Once complete, the property will become a Hilton Grand Vacations Timeshare with 388 vacation villas on a 28-acre property. Capbridge Group, which announced plans to buy the property in October, will tackle the final development phase in 2015. The property will come online in 2017.

Article HERE

Takeaway: Hilton Hotels continuing to pursue a capital light timeshare strategy.

NCLH – announced an agreement with Princess Cruises, Ltd. to purchase the 684-passenger ship Ocean Princess for its newly acquired Oceania Cruises brand. The new addition will be named Sirena. Upon delivery in March 2016, Sirena will immediately undergo a 35-day, $40 million refurbishment in Marseille, France to elevate the ship to the Oceania Cruises' standard of elegance. The ship will welcome her first guests in late April 2016.

Takeaway: NCL paid $82m for the 15-yr old Ocean Princess or ~$120k per berth. Including the $40m investment in Ocean Princess, that translates to $178k per berth. For comparability, the recently launched Regal Princess cost ~$201k per berth and the NCL Escape/Bliss cost $225k per berth. From Norwegian's perspective, they remain committed to growth and buying this older ship may generate a higher ROIC than if they built a new one.

CCL – When ms Koningsdam debuts in 2016, the ship will feature Holland America Line's first-ever purpose-built staterooms for families as well as single staterooms among its 1,331 guest accommodations (total capacity is 2,650). In addition, many familiar stateroom categories such as Neptune, Signature and Vista suites will be available in a wider range of sizes and different configurations to choose from.

Article HERE

CCL – Princess Thanksgiving Cyber Week Sale

Guests can save up to 50% off short cruise Getaways and weekend cruise vacations and bring along their friends and family with third and fourth guests as low as $50 per person. In addition to low fares, guests can book their stateroom with deposits of only $1 per person for getaway cruises shorter than five days.

INDUSTRY NEWS

Mainland Corruption Crackdown, Tycoons in Hiding – Many Mainland Chinese tycoons are hiding out at the five-star Four Seasons in Hong Kong to avoid being investigated or questioned by officials as part of China's anti-corruption campaign. While in residence, the tycoons turned guests are kept informed of the progress of their graft cases by visitors from the mainland.

Article HERE

Takeaway: A clear indication that business people are taking the corruption seriously.

Macau Urged to Diversify Its Investment Away From China – The 2003 winner of the Nobel Prize in Economics Robert F. Engle advised Macau Government Officials to invest more money abroad in order to diversify its investment portfolio. “If the biggest risk to the Macau economy is the Chinese economy, then you do not want to invest all your money in the Chinese economy. You should invest in other assets around the world”, he said. According to Mr. Engle, such investment strategy would have limited impact but would make the Macau economy more resilient against downturns in the Chinese economy.

Article HERE

The King of Gambling Celebrated 93rd Birthday – Macau casino mogul Stanley Ho Hung Sun celebrated his 93rd birthday on Tuesday. Mr Ho and members of his family celebrated by giving HKD2 million (US$258,000) to the Community Chest of Hong Kong charity fund.

Article HERE

Macau MICE Booming – The latest data from the Statistics and Census Service indicates 240 MICE events were held in 3Q 2014, an increase of 14 events versus the same period last year. Receipts from these exhibitions exceeded MOP37 million (US$4.6 million) in the quarter, up 81% compared to MOP21 million in receipts during the same period last year. During 3Q 2014, the total number of participants and attendees to MICE events reached 724,800, up 16% compared to the same period of last year. Some 214 of the total events, or almost 90%, were meetings, which nevertheless only attracted 4% of total participants and attendees. The other 96%, totaling 695,456 individuals, joined the 26 exhibitions instead.

Article HERE

Takeaway: Non-gaming is certainly doing better than gaming in Macau.

Hengqin Residential Sales Increasing – Over the last month, the pre-sale of apartments planned in Hengqin have been gaining in popularity. According to a local sales data, more than two hundred pre-development flats sold out within three weeks. Sales data indicates, about 70% to 80% of buyers are local residents, and most of them are young people below the age of 30.

Article HERE

Takeaway: Newly developed, larger flats at a lower price with better air quality and a shorter commute making Hengqin Island real estate more appealing for workers commuting to Cotai than the Macau peninsula.

Mainland China Crackdown on Indoor Smoking – China is considering fining smokers who light up indoors as much as 500 yuan (USD81) and penalizing operators who don’t stop them, a sign of rising political willingness to curb an industry that brings in billions in tax revenue. If implemented, the changes would mark a reversal in the world’s most populous country, which so far hasn’t succeeded in eliminating smoking in public indoor places such as bars and restaurants. China is home to about 300 million tobacco users, and cheap cigarettes are often exchanged as a social courtesy – almost like a handshake. Surging health-care costs are now forcing China to follow other parts of the world in restricting such public smoking.

Article HERE

Takeaway: Smoking-related matters is getting more attention in China too

Foxwoods Casino to Shrink– Foxwoods Casino, the largest casino resort in North America, is getting rid of 1,000 slots and 120 table games to free up space for nightclubs and other new attractions as it adapts to fierce competition.

Article HERE

Takeaway: Similar to the the Las Vegas Strip properties, Foxwoods is now looking to stronger food and beverage offerings as a way to drive revenues.

UK Hotel Chains Listed – KSL Capital Partners, a private equity firm based in Denver, Colorado, has appointed the investment bank UBS to conduct a full review of strategic options for Malmaison Group including Malmaison Hotels and Hotel du Vin Hotels. KSL acquired Malmaison for £200m takeover in March 2013. Malmaison operates 13 hotels throughout the United Kingdom with a brand premise of "Hotels that dare to be different". While Hotel du Vin is a luxury boutique hotel chain that has fifteen hotels throughout the United Kingdom.

Article HERE

Takeaway: Might Starwood Capital be interested?

MACRO

Macau inflation increased by 6.18% YoY and 0.49% MoM.

Hedgeye Macro Team remains negative Europe, their bottom-up, qualitative analysis (Growth/Inflation/Policy framework) indicates that the Eurozone is setting up to enter the ugly Quad4 in Q4 (equating to growth decelerates and inflation decelerates) = Europe Slowing.

Takeaway: European pricing has been a tailwind for CCL and RCL but a negative pivot here looks increasingly likely in 2015. Following CCL's F3Q 2014 earnings release, we recently turned negative on those stocks based on the negative European thesis.

Hedgeye Macro Team remains negative on consumer spending and believes in muted inflation, a Quad4 set-up. Following a great call on rising housing prices, the Hedgeye Macro/Financials team is decidedly less positive.

Takeaway: We’ve found housing prices to be the single most significant factor in driving gaming revenues over the past 20 years in virtually all gaming markets across the US.