Tickers: GTK.IM, MGM, RCL

EVENTS

- Dec 1: 8:30 am IKGH Q3 earnings

- Dec 17: Upstate NY casino decision

COMPANY NEWS

GTK.IM – The GTECH-led Northstar Consortium managing the New Jersey Lottery fell short of its revenue target by $24 million in the year ended June 30 and lottery collections, New Jersey's fourth-largest revenue source, were down 9.2% from July 1 through Oct. 31 versus a forecast for annual growth of 7.4%.

Article HERE

Takeaway: Statewide lottery results are down for most States (notably Illinois and Indiana) on a year-over-year basis.

MGM – completed its $1.25 billion 6% Senior notes unsecured notes due 2023. $1.15 billion was issued at par, while an additional $100 million was issued at 100.75%.

Takeaway: MGM attributes the raised offering from $1.15 billion previously to 'strong demand' from the investment community.

RCL – Celebrity Cruises canceled two port stops on Celebrity Millennium in Indonesia this week due to an undisclosed 'dispute' with Indonesian authorities. The line has canceled a two-night stay in Bali scheduled for this Thursday and a port call in Komodo Island on Sunday November 30 on Celebrity Millennium. Instead, the sailing will call in at Ho Chi Minh City and Bangkok. Millennium is on a 14-night cruise round-trip cruise from Singapore that had been scheduled to call in Indonesia, Thailand and Malaysia.

Article HERE

MSC– MSC Cruises has started a fleetwide optimization enabled by Marlink to improve shipboard Very Small Aperture Terminal (VSAT) connectivity. MSC Cruises is the first cruise line to use the iDX 3.2 software and X7 modem from iDirect for enhanced service delivery and performance.

Article HERE

Takeaway: WiFi has become an essential onboard offering for potential cruisers. MSC doesn't want to be left behind.

INDUSTRY NEWS

Macau VIP Junket Operator Seeks HKSE Listing– Sing Hou Entertainment Group Ltd is seeking to list its shares at the Hong Kong Stock Exchange. The company’s draft application for listing says it wishes to expand its customer base and market share. Sing Hou Entertainment runs a VIP gaming room in the StarWorld casino, but intends to reduce its dependence on Galaxy Entertainment Group Ltd by operating junkets to casinos run by other gaming companies.

Article HERE

Takeaway: Junkets seeking other capital markets solutions to their liquidity constraints.

Macau Political Reform – Comments delivered by lawmaker Ng Kuok Cheong sparked further debate on Macau’s political reform, but it remains clear that, for some, democracy is not a priority. The government reiterated the stance that democracy is not only about introducing universal suffrage. A large number of legislators said that there are rather more pressing matters needing the administration’s attention, namely housing and public transportation. Ng believes that the electoral system is not being developed taking into account Macau’s reality. As only 14 lawmakers have been directly elected by Macau’s citizens, it’s not enough to represent the local population.

Article HERE

Takeaway: Thus far, Macau has not experienced the public protests against the the Mainland China SAR system. While the upcoming visit by Chinese President Xi Jinping to Macau around December 20 could present potential for protests, Macau is not Hong Kong.

Macau Public Transit Criticized – There are simply not enough buses. This topic reappeared, as lawmakers questioned the government on its policy to provide residents with an improved public bus system. Public commentary by legislator Au Kam San prompted debate as well as questions directed to the deputy director of the Transport Bureau (DSAT), Chiang Ngoc Vai, regarding the priority of this issue.

Article HERE

Takeaway: Worker transportation and housing remain key issues and may become tenants of gaming concession renewal discussions.

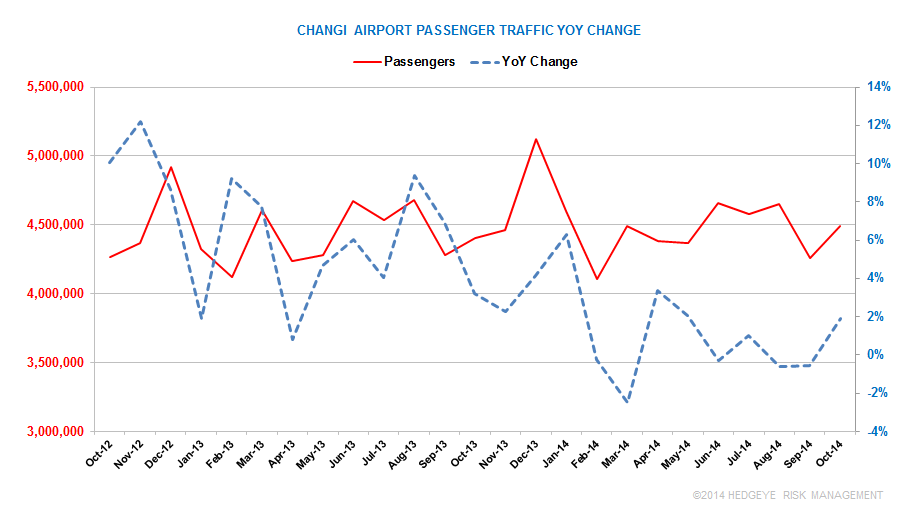

Singapore Changi Airport Traffic – Changi Airport handled 4.49 million passengers in October, a 1.9% YoY increase. Passenger movements between Singapore and China rose 5%.

Article HERE

Takeaway: Visitation at Changi have been flattish since June 2014

Hong Kong Police Begin Clearing Protest Barricades – Hong Kong police began removing protesters from a key road at a pro-democracy protest site in Mong Kok as hundreds continued to block Argyle Street hours after authorities began enforcing a court injunction to open the road. The main occupation area at Mong Kok, a densely populated working-class district that is a popular tourist and shopping area.

Article HERE

Massachusetts – The state gaming commission set January 30 as the deadline to apply for the southeastern region casino license. Only KG Urban (New Bedford project) has formally applied but the Mashpee Wampanoag (Taunton project) and Foxwoods may apply as well.

Global Hotel Rate Outlook for 2015 – American Express Global Business Travel released its 11th annual Business Travel Forecast for 2015 and highlights include:

- North America: hotel rates growth for mid-range hotels of 3% to 6% and upper-range hotels 3.5% to 7%.

- Latin America: hotel rate growth of 5% to 8% and upper-range hotels 5% to 7%.

- EMEA: hotel rate growth of 1% to 6% for mid-range hotels and 0% to 5% for upper-range properties.

- Asia Pacific: hotel rate growth ranges from 0.8% to 3.5% for mid-range hotels and 0.7% to 3.5% for upper-range hotels.

Article HERE

Takeaway: Solid rate growth projections from AMEX

MACRO

China Additional Interest Rate Reductions – the PBoC reduced 14-day repo rate to 3.2% from 3.4%, the third time in three months. Prior rate reductions include a cut to 3.4% from 3.5% on October 14 and from 3.7% to 3.5% on September 17.

Takeaway: More loosening policies

Singapore GDP Growth – the Singapore economy expanded 2.8% during Q3 2014, better than the consensus advance estimate of 2.4%. Despite the better growth, manufacturing and construction remained anemic. Singapore's Ministry of Trade and Industry expects full-year economic growth to come in at 3%.

Article HERE

Hedgeye Macro Team remains negative Europe, their bottom-up, qualitative analysis (Growth/Inflation/Policy framework) indicates that the Eurozone is setting up to enter the ugly Quad4 in Q4 (equating to growth decelerates and inflation decelerates) = Europe Slowing.

Takeaway: European pricing has been a tailwind for CCL and RCL but a negative pivot here looks increasingly likely in 2015. Following CCL's F3Q 2014 earnings release, we recently turned negative on those stocks based on the negative European thesis.

Hedgeye Macro Team remains negative on consumer spending and believes in muted inflation, a Quad4 set-up. Following a great call on rising housing prices, the Hedgeye Macro/Financials team is decidedly less positive.

Takeaway: We’ve found housing prices to be the single most significant factor in driving gaming revenues over the past 20 years in virtually all gaming markets across the US.