TODAY’S S&P 500 SET-UP – November 19, 2014

As we look at today's setup for the S&P 500, the range is 53 points or 2.43% downside to 2002 and 0.16% upside to 2055.

SECTOR PERFORMANCE

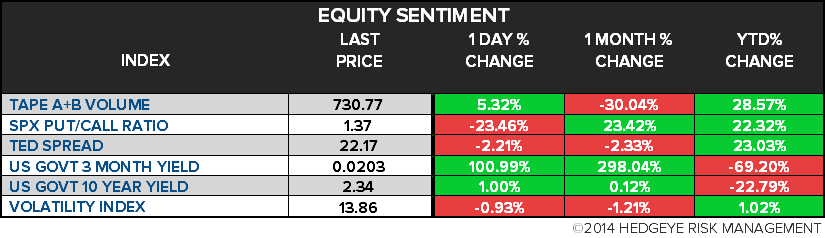

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.82 from 1.81

- VIX closed at 13.86 1 day percent change of -0.93%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Nov. 14 (prior -0.9%)

- 8:30am: Housing Starts, Oct., est. 1.025m (prior 1.017m)

- 10:30am: DOE Energy Inventories

- 2pm: FOMC minutes released

GOVERNMENT:

- 10am: Senate Banking Cmte hears from FHFA Director Mel Watt on balancing stability, growth, affordability in mortgage mkt

- 10am: SEC open meeting on adopting Regulation SCI standards that would require exchanges to improve technology systems

- 10am: Senate Homeland Security Cmte hears from CDC Director Tom Frieden on Ebola response

- 10am: House Energy and Commerce Cmte hearing on development of medical products in wake of Ebola

- 1pm: CFTC media briefing to unveil national consumer protection campaign

- 5pm: Permanent Subcmte on Investigations releases information in advance of hearing on Wall St bank involvement with physical commodities

WHAT TO WATCH:

- Obama Said to Include Tech Visa Expansion in Immigration Plan

- FOMC Minutes Guide: From Job Mkt Gains to ‘Considerable Time’

- Ackman Said to See Need for Significant Cost Cuts at Zoetis

- Paramount Raises $2.3b in Record IPO for U.S. REIT

- KKR, CD&R Said Preparing PetSmart Bid of >$7.5b: Reuters

- Wells Fargo, U.S. Said No Longer Hopeful About Mortgage Pact

- Wells Fargo to Start Europe Infrastructure Fund: Reuters

- Buffett Creates Company to Buy Homes in Spain: El Economista

- FTC May Need Dollar General to Divest Over 4k Stores: NYP

- New Takata Air-Bag Case Prompts U.S. Demand for Natl. Recall

- Ford, GM Demand Seen Buoying Takata Amid Congress Probe

- Apple Sticking With Arizona Jobs Plan After GT Advanced Falters

- Amazon Warehouse Worker Forces Changes as Labor Board Settles

- Darden Executives to Retire Amid Cost Savings and Job Cuts

- Music Mogul Azoff Demands YouTube Drop Pharrell, Eagles Songs

- Hilton Said to Seek A$400m From Sale of Sydney Hotel

- Netflix to Expand in Australia, New Zealand From March 2015

- Senate Rejection of Keystone XL Measure Sets Up 2015 Showdown

- United, Orbitz Sue Travel Site Over ‘Hidden City’ Ticketing

- CBS Says Dish May Black Out Network at Contract End Nov. 20

- WhatsApp Encrypts User Messages, Following Google, Apple

- Putin Said to Back War on Corruption as Sanctions Bite

- India Quarantines Man Cured of Ebola as Semen Contains Virus

AM EARNS:

- E-House China (EJ) 6:25am, $0.17

- JM Smucker (SJM) 7am, $1.53

- Lowe’s (LOW) 6am, $0.58 - Preview

- Mallinckrodt (MNK) 7am, $1.41 - Preview

- Metro (MRU CN) 7am, C$1.27

- Stage Stores (SSI) 6am, ($0.21)

- Staples (SPLS) 6am, $0.36 - Preview

- Target (TGT) 8am, $0.47 - Preview

PM EARNS:

- Copa (CPA) 4:43pm, $2.00

- Hillenbrand (HI) 4:24pm, $0.61

- Keurig Green Mountain (GMCR) 4pm, $0.77

- L Brands (LB) 4:30pm, $0.40

- Real Goods Solar (RGSE) 4:04pm, ($0.13)

- Salesforce.com (CRM) 4:05pm, $0.13

- Semtech (SMTC) 4:30pm, $0.44

- Williams-Sonoma (WSM) 4:10pm, $0.63

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Brent Oil Rises Most in Three Days on Car Bomb in Kurdish City

- Iron Ore’s Rout Seen Relentless by SocGen as Miners’ Stocks Drop

- Brace for Thanksgiving Traffic as Car-to-Plane Gap Grows: Energy

- Gold Trades Below 2-Week High as Dollar Gains Before Fed Minutes

- Nickel Advances as Indonesia Adheres to Ban on Exports of Ore

- Cocoa Seen Extending Drop on Signs of Ebbing Chocolate Demand

- Copper Prices Seen Rising as Mining Costs Increase: Codelco CEO

- Europe-U.S. Oil-Product Cargo Flow Rises 67% in Broker Survey

- Arabica Coffee Futures Rise for Second Day; Cocoa Also Gains

- ICAP in Talks to Combine Shipbroking Unit With Howe Robinson

- EUROPE OIL PRODUCTS: Gasoline Crack at 7-Week High; Gasoil Gains

- Six Feet of Snow Buries Upstate New York a Month Before Winter

- Senate Rejection of Keystone XL Measure Sets Up 2015 Showdown

- Corn Drops to One-Week Low as U.S. Farmers Harvest Record Crop

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team