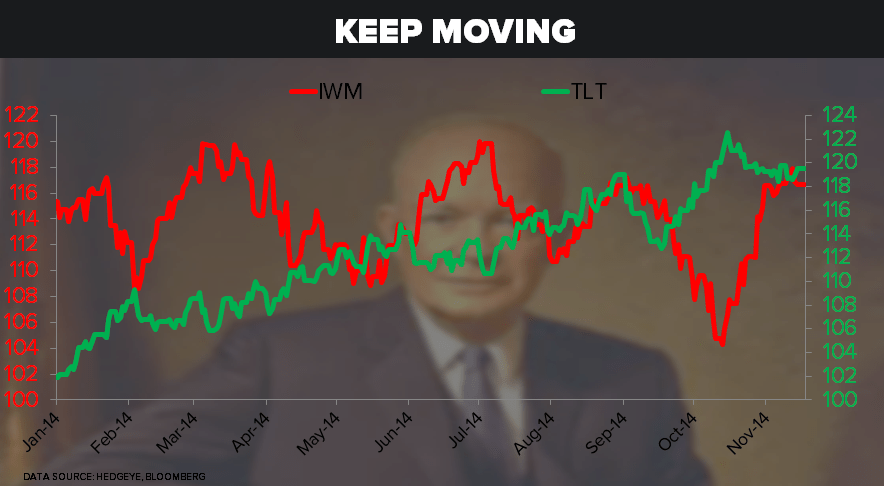

"While risk often moves slowly, then all at once… sometimes it doesn’t move at all," wrote CEO Keith McCullough in today's Morning Newsletter. "Last week, our least preferred of the major US stock market indices (Russell 2000) did absolutely nothing."

"Oh, and it was unchanged in the week before that too. I guess that’s what they call a 'bull market' - something that doesn’t go down! After going down hard (-15% from its all-time #bubble high in July, to its October low), the Russell is +0.9% YTD.

“So,” keep selling that (IWM) against The Perfect Idea during what we call #Quad4 Deflation = Long the Long Bond (in TLT, EDV, etc.). And de-stress yourself a little as the macro market stresses about both growth and inflation slowing."