Editor's note: The excerpt accompanying today's Chart of the Day is from CEO Keith McCullough's Morning Newsletter this morning.

Obviously times, technologies, and mostly everything other than the Old Wall have changed. But the very basic difference between what I’ll call good vs. bad #deflation has not.

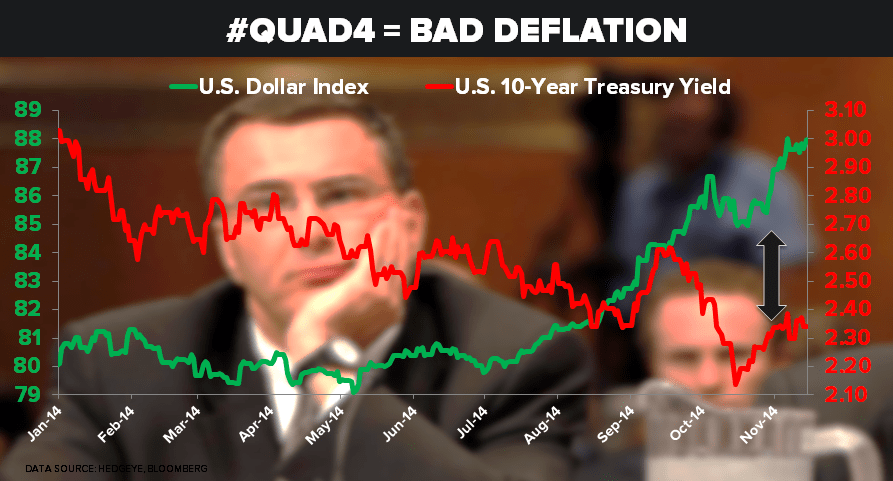

Here’s the difference:

- Good #Deflation = #StrongDollar + #RatesRising (signal that real, inflation adjusted US growth is accelerating)

- Bad #Deflation = #StrongDollar + #RatesCrashing (signal that both US and Global growth are slowing)