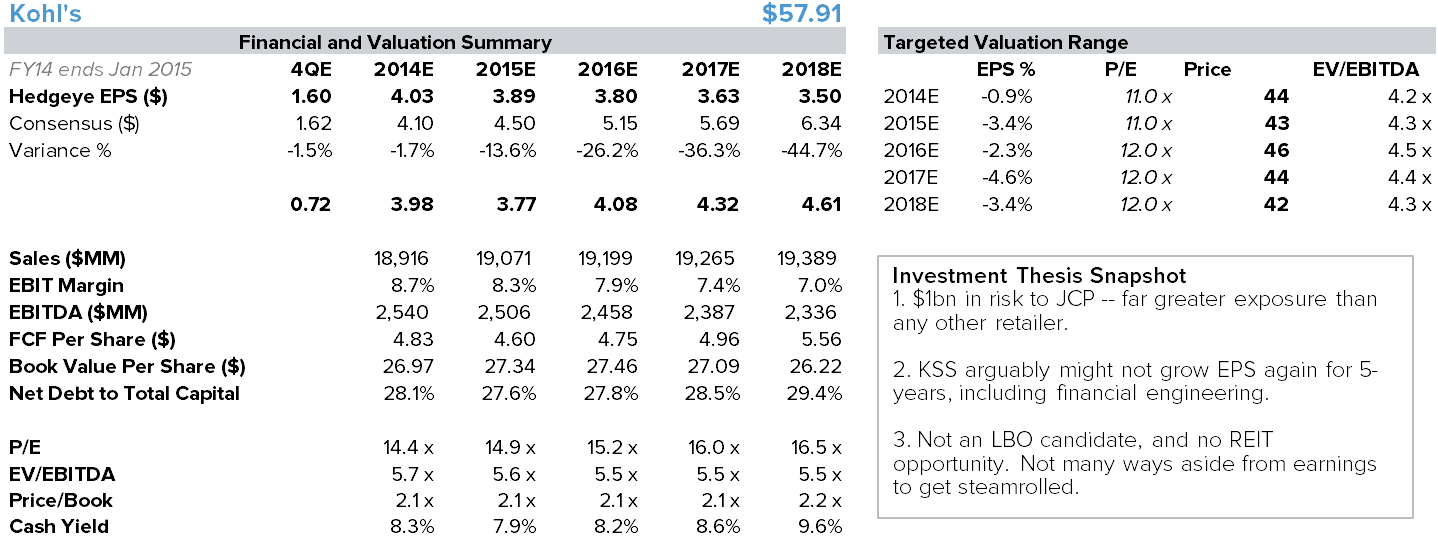

We’d short KSS today – still our favorite name on the short side. We think that the company’s earnings power is currently about as good as it’s going to get, and that once KSS closes out 2014, it won’t see better than $4 again before the end of the decade – if ever. We have earnings shrinking down to a base of $3.50 at the same time the Street has it growing to over $6. We think that best case, there’s upside to $65 (13 x $5.00 in 2-years), but if we’re right the stock has downside to $35 (10 x $3.50). Importantly, the free cash flow profile should allow it to get that low before a DDS-esque FCF yield support valuation case creeps into the equation. That’s about $8 upside, and $22 downside. We’ll take those odds any day on a name like KSS.

We actually figured that this print would be a non-event given that KSS just preannounced at its Analyst Event on 10/29. But lo and behold, the company managed to miss the number it gave to the Street when there was only three days left in its quarter. If there was any company in retail that should have hit estimates this quarter it is KSS. But no. KSS missed comp by 40bps (-1.8% vs preannouncement of -1.4%) and missed EPS by $0.04.

We outline our full short call in our Best Idea slide deck – the link to the presentation and materials are below.

Replay Link: CLICK HERE

Materials: CLICK HERE

Let’s look at it like this. We’ll assume for -- just a minute -- that KSS internal financial reporting is acceptable. Let’s assume that the final three days of the quarter represents 4% of the quarter’s sales. That’s about $175mm. Those days would have had to gap down about 10% immediately following the analyst meeting. Either a) it’s unlikely, and management’s forecast accuracy is simply horrendous, or b) the business volatility is significant. It’s probably a little of both.

4Q Sales Considerations

Now KSS expects us to believe that it can comp 2-3% in the fourth quarter. To get that range we need to assume dot.com growth of 25% and a store comp between -1% and flat which is predicated on flat traffic. KSS hasn't put up a positive store comp in over 3 years. But, it is comping against the -9% three year stack comp it put up in 4Q13.

For the quarter we shake out at 25% DTC growth and a -1% store comp which equates to a 2% consolidated comp. We'll give the company the benefit of the doubt on the sales line and take it away on gross margin. The biggest headwind on this line item is shipping cost (somewhat muted given fulfillment issues in 2013), followed by national brands and loyalty dilution, plus the 'promotional environment'.

The sales waterfall the company built for the 4th quarter revenue number was probably the best disclosure the company gave during the call. If they would have presented a slide of this and only this during the analyst day it would have received a much better reception. Here are the building blocks to a 2.5% comp.

- -4% growth in the base business = ($195)mm

- 25% growth from e-commerce = $180mm

- Extra day between Thanksgiving and Christmas = $100mm

- Loyalty = $60mm

- Personalization = $50mm

- Beauty = $10mm

The Beauty contribution is so interesting. Every Bull we talk to highlights the upside from Beauty. But most of them don’t seem to realize that it is only about 1% of sales. Alas, this big sales driver is accounting for $10mm on a base of $6.1bn. Yes, that’s only 0.16% sales accretion in the quarter. We call that a rounding error.

We should also note the impact of Izod and Juicy Coture, something we’ve been hearing about all year. Izod performed well, but Juicy was decidedly mixed. Our point has been that the company launches new brands EVERY year. Some work, and some don’t – it’s part of being in the department store business.

Margins Considerations

No material changes to our model. By year 5 we have gross margins coming down 100bps from 36.5% in 2013, with SG&A growing steadily at 1% per year. Management reiterated that there weren't many levers to pull on either line outside of payroll. Perhaps more troubling was the talk about ship from store. We'd flagged it as a benefit to the overall profitability of the dot.com channel, but based on the commentary we heard today that doesn't appear to be the case.

In the near term, we can’t reconcile SG&A guidance. McDonald guided the year to the low end of the 1.5%-2.5% range. Implying 5% growth in 4Q. But that’s unlikely to happen. We’re at 1%. If his guidance holds, then it costs the company about $0.16 per share, or 1,000bp of earnings ‘growth’.

10/30/14 06:40 AM EDT

KSS – ‘SHORT'NESS AGENDA

Takeaway: The Greatness Agenda is neither investable nor believable. 35% EPS downside. Stock downside/upside is 3 to 1. We’d press this one here.

Conclusion: We went into this meeting expecting to hear at least a few points that would go toe-to-toe with our Short call. But management spent the better part of seven hours articulating (despite its intentions) why it has Zero competitive advantage. We still don't think there's a viable financial plan, and if there is one, we have less confidence today in the company's ability to execute on it. What we do know is that this management team comes across as being extremely comfortable being very mediocre. Guidance implies 2017 EPS of $5.30, which our analysis suggests is a pipe dream. Our math gets us to $3.50. This should be a $35 stock -- a level that does not provide meaningful cash flow yield support relative to where other names in this space have traded. With at least 3 to 1 downside upside, this remains our top short in retail.

DETAILS

Well...if you were wondering why KSS does not regularly host analyst meetings, now you know. While Hedgeye was not physically present at the event (having a short call and 60 page slide deck doesn’t get you a seat in the room with KSS) it was still easy to hear the oxygen get sucked out of the room on a number of occasions via webcast. Yes, it was that bad.

We went into this one looking for areas that could challenge our bear case, but could not find a single one. Though we found a few of the presenters to be high quality (Logistics, Digital, Marketing) the collective message was extremely unconvincing and unimpressive. In fact, we are not really clear as to what the message was. What we do know is that this management team comes across as being extremely comfortable being very mediocre.

We think the company’s financial targets are entirely unbelievable. The company basically guided to about $5.30 in EPS in 2017 ($21bn revs and 9% margins). So you need to believe that KSS can comp nearly 3% for three years. The last time it did this was 13 years ago when it had a base of only 350 stores, had nearly a fifth of its square footage base entering the peak part of the maturation curve, and as a kicker, was bouncing back after a recession. But the company’s targets today assume that the industry goes nine years without a major correction/reset in sales/margins. That’s never happened. Not even close. We’ve never seen a cycle go more than six years (and we’re still in it). We think that’s extremely poor risk management on the part of the team steering this ship. We think earnings will be $3.50 in 2017 – that’s 35% below guidance. And if we had to pick an over/under on our estimate, we’d say closer to $3.

Let’s say – just for a minute – that the company is right. You’re playing for a ‘goal’ of sub-3% growth and $5.30 in earnings in 3.5 years. At best that’s worth a 12x p/e, or $64 – in 3-years. Discount that back by 10% annually, and you get to $48 today – for a best-case scenario. If we’re right, then we’re looking at about 10x $3.50 in EPS. The bulls would point to the company’s cash flow as support, and that’s fair. But as the P&L gets hit, cash flow comes down as well. A $35 stock suggests about a 12% free cash flow yield on our model. That’s high, but far from egregious. Dillard’s, for example, has traded in recent years at a free cash flow yield as high as 25%.

The bottom line is that we think this name is still very shortable today with at least 3 to 1 downside/upside. It remains our top short in retail.

Here are a few things that stood out for us at the meeting (in no particular order).

1. Is This Really A Goal. The overreaching goal was “To Become the Most Engaging Retailer in America”. Didn’t Ron Johnson have some iteration of that mantra when he killed JC Penney and replaced it with jcp? We like setting goals that are quantifiably achievable. Nike couldn't even achieve this goal if it tried (which it's not).

2. Greatness Redux. Initially we gave Kevin Mansell (CEO) credit as he started off by talking about the challenges they have faced (share too high in categories that consumers are shifting away from, and share too low in categories consumers are embracing, and relevancy of real estate). Then he flashed a slide that said “Time to Evolve” That was pretty exciting, as KSS does not evolve very well. We held our breath and thought we’d get some cool new insightful strategy. But no. We got the good ‘ol “Greatness Agenda”. It’s the same thing we hear about every conference call.

3. Numbers are Not Believable. We said this above, but it's worth repeating. In fact, Mansell openly said that he did not want to give financial targets – he wanted to qualitatively show that KSS “has the right team in place to take the company into the new era of retailing”. Wes McDonald (CFO) did the right thing and put his foot down by handing out at least a few numbers, even though there’s no evidence that these targets fully address the substantial risks that KSS will increasingly face.

4. Who Were They Talking To? Our sense is that the numbers that KSS targeted -- $21bn in sales in 2017 and flattish margins – represent a statement to employees more than to the financial community. They can’t get up there on stage and tell the rank and file (who are all listening in) that sales and profits will be flat to down over the next few years.

5. JCP Won The Battle of the Analyst Meetings. For what it’s worth, last month JCP gave the Street 10x as much information in just three hours (whether you choose to believe it or not), while it took Kohl’s seven hours to say almost nothing.

6. Nothing Unique. We can't recall hearing about a single initiative all day – whether it be product, marketing, or customer engagement -- that other retailers are not already doing.

7. Stores Too Big? Kevin Mansell actually said something to the tune of “Yeah, many of our stores are probably too big. I wish they were smaller.” We think we got those words right – but if we’re off (transcript not out yet), they’re at least in the ballpark. His somewhat cavalier attitude toward the whole issue was quite off-putting.

8. Unlikely to Close Stores. The worst performing stores are ‘only losing a few hundred thousand dollars each.’ That’s pretty bearish as it suggests that there’s not exactly a few hundred stores they can close to meaningfully boost profitability.

9. Acquisitions. They actually started talking about acquisitions. That’s just baffling. What they’re basically saying is that (and these are our words, not theirs) “we don’t have opportunities to reinvest in our own business, and are less interested in buying our own company (stock repo), so we’ll try buying other business for the first time in our history." People hanging their hat on the free cash flow yield should consider how fast the cash could go away when it’s spent on an off-price apparel chain or luxury flash-sale site.

10. Frozen Love. We wish we could make our own word cloud from this analyst day, but unfortunately the transcript isn't out yet. We think the words "Love", and "Frozen" would take center stage (let’s say 24 size font) and the key words like margins, earnings, and cash flow maybe about a 6 font. Seriously, Michelle Gass, the Chief Customer Officer, literally said “Love will drive our business”. We understand that a) it's her job to talk like this, and b) she meant it in the context of caring for customers. But this was over the top.

11. JCP/Share. The fact that JC Penney was not uttered all day is bothersome. That’s a consistent miss we see in Kohl’s strategy to deal with a competitor that lost $90/foot in sales over three years, and is clearly on the rebound. All of our research (including several consumer surveys) shows that KSS won (fair and square) about $1bn in revenue from KSS – half of which was online. JCP will take it back. Our surveys suggest that consumers want to go back to JCP with the right product/promotions. JCP will get the sales back, whether it earns it, or buys it. Either way it's bad for KSS.

12. E-commerce is not margin accretive on the Gross or EBIT level. Management wouldn't quantify, but did characterize it as worse than in store. Plus it cannibalizes sales from its brick and mortar business. The company validated our survey research. 96% of shoppers who don't visit the store will not shop online. With a fully extended store base how do they attract new customers? We don’t think the answer is personalization. We did a lot of work on this one in our recent report.

13. Loyalty Math. Initial loyalty sign up numbers are impressive with 5mm added in new markets over the past 21 days. 58% of the now 15.5 million members are non-credit users. But, take into consideration that there are 30mm active credit card members. That implies that 21.7% of active credit card users are now card carrying members of the Y2Y. Credit accounts for 57% of purchases and offset SG&A by $407mm in 2013. Any shift by the customer away from the Credit program to loyalty (they get basically the same deals without a 24% APR) would be a significant margin headwind.

14. Two Conflicting Initiatives. ‘Buy-online and pick-up in-store’ and ‘store vs. same day ship’. Our research on buy-online, pick-up in-store (See our Department Store deck from last week) indicates that the #1 reason for choosing this option is free shipping. #2 and #3 on that list, faster fulfillment and convenience, are solved by same day delivery. Shipping costs are already below the rest of the industry average at $75 and we think that goes lower before it goes higher. Which offsets the incentive to pick up items in store.

September 29, 2014

KSS – WHY WE THINK IT’S A SHORT

Takeaway: Here are some of the more controversial slides from our 60-slide deck from last week on why we think KSS is a structural short. Last week we hosted a conference call to review our 60-page slide deck as to why we think KSS is a short. If you’d like to listen to a replay of the call and download the full materials, please click the link below. We picked out eight slides below that are among the more controversial.

Point #1: Expectations Too High

Yes, near-term numbers look doable given several tailwinds facing all retailers. But one we get past this year (only four months away) we think KSS numbers will start to come down materially. The consensus has earnings growing 10% next year, while we think they will be down nearly 10%. Then they’ll be down again, and again, and again. Ultimately, once we’re past 2014, we don’t think that KSS will earn $4 again until the tail end of the next economic cycle.

Point 2: Losing Share At A Faster Rate

It’s no secret that department stores are losing share of wallet (3.5% of Retail Sales vs 10% a decade ago), but KSS is losing share within that context. The blue line in the chart below shows KSS’ share gain of the department store space. The first big bubble – from 1Q09 to 4Q10 – came about 3-years after a meaningful square footage growth spurt. That’s when the stores began to hit the sweet spot of the maturation curve. Then the next bubble came a little over a year later when KSS gained what we think (based on our surveys) is $1bn in share from JCP. Our latest survey shows that about $150mm has shifted back to JCP – but that still leaves $850mm at risk for KSS. The punchline is that after gaining share of this space every single quarter since its inception, KSS is now a net share loser.

Point 3: This Model Is Broken

There’s no square footage growth – at all. Productivity of $210/ft in brick and mortar stores is trending down. E-commerce is the only growth engine, but unfortunately it is the lowest margin business at KSS by a country mile. As such, gross margins are structurally headed lower. SG&A can’t be cut in line with the gross profit erosion. D&A was just lowered from $950mm to $900mm – which is stunning in itself. That’s not likely to go down much further. Cash flow still remains healthy enough to buy back 7% of the stock this year. Buy with lower net income, we think that repo/financial engineering gets cut by better than 50% for the duration of the model. EBIT should be down 5-8% each year, with share count making up about 3% of the gap. Net/net = EPS declining every year.

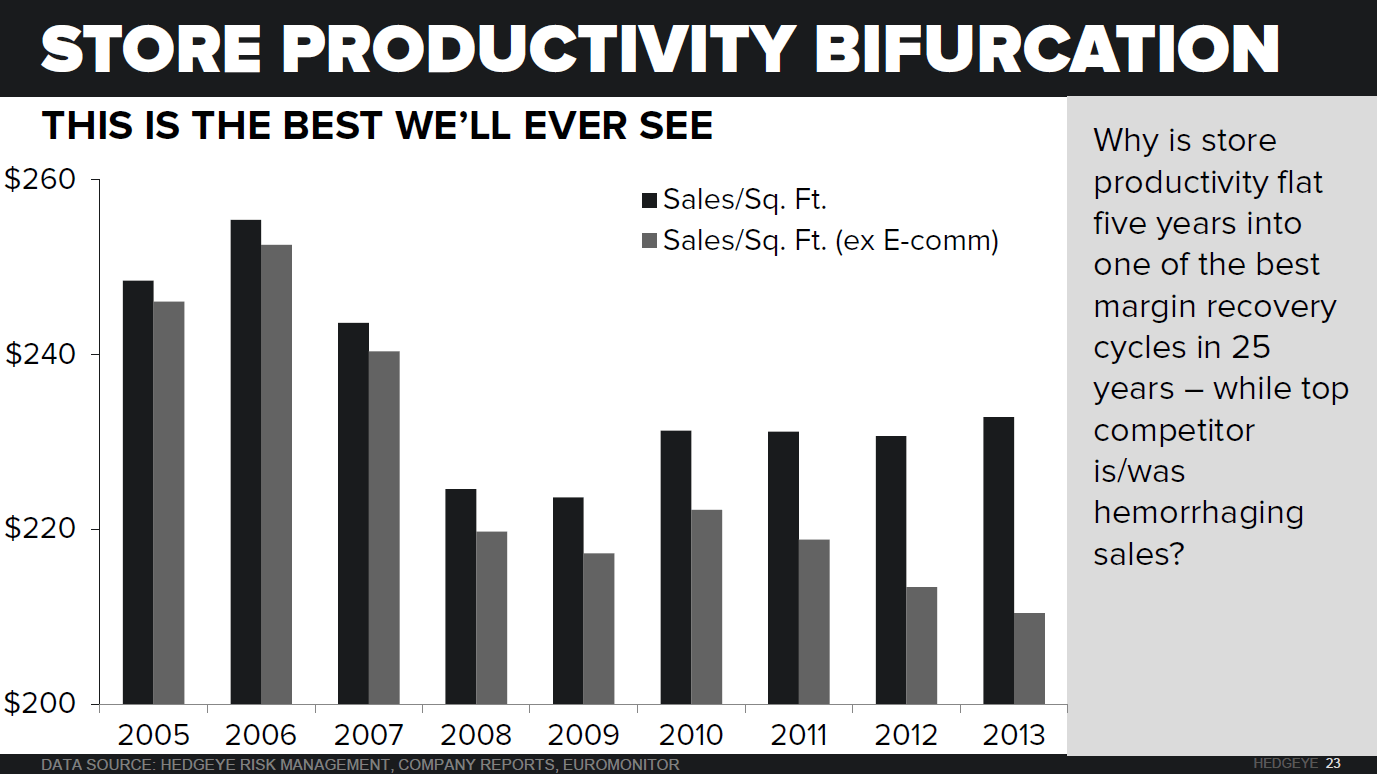

Point 4: Store Productivity Bifurcation

Sales per square foot have been flat for the past four years, but that is only if you include e-commerce. Brick & Mortar productivity is $210, and is at the lowest rate we have ever seen it. There is absolutely no valid argument we can find that this turns around – particularly given that JCP is sitting at just $108 in productivity and has KSS right in its sights. We think those two will converge over time.

Point 5: New Brands – Juicy and Izod

This topic absolutely dominates the information flow around KSS. We all know that Juicy Couture and Izod are now available at KSS. That said, our consumer survey shows Kohl’s purchase intent is down year/year, while retailers like JC Penney and Macy’s are up meaningfully. So we know about the brands – but consumers might not know, or might not care. Nonetheless, let’s keep in mind that there’s noise around new brands EVERY year at Kohl’s. Take a look at the graphic below. Could this years’ additions be better than last years? Possibly. But keep in mind that Izod and Juicy are not exclusive. Izod is all over Macy’s and JC Penney’s. Juicy is in the process of growing distribution through new owner Authentic Brands. To get a good read you need to quantify the impact (see next exhibit).

Point 5b: Quantifying Juicy and Izod

We know that these brands occupy 525 sq ft and 700 sq ft, respectively, inside the average KSS box. That’s 1.42% of KSS’ total square footage. Now…it can’t just create space out of nowhere, which means that it needs to take out product that is underperforming – but is still productive. Assuming that these brands generate $225/ft in productivity, and that it is replacing private label brands that are doing $110 per foot in the same space, we build up to about $250mm in incremental sales in another two years. That’s about 1.3% accretion to sales, but it comes at a lower margin as these national brands carry lower profitability than the portfolio as a whole. The bottom line = it’s going to take a lot more than a couple of mediocre brands to salvage KSS’ top line.

Point 6: Structural Margin Decline

Gross margins on KSS’ e-commerce business run about 1,200bp below the store-level margins. Some people are hoping/banking on a margin rebound as KSS did not seemingly benefit from the same tailwind the rest of the group has over the past five years. The truth is that it has. Without that tailwind we’d be looking at KSS with margins near 5-6% today. The industry tailwind was masked by the massive growth in KSS’ e-commerce business. In fact, from ’05-’13 KSS put up the highest growth rate of any ecommerce business in the US throughout all of retail. But as this business continues to grow 15-20% annually (the only line item to grow aside from SG&A) it naturally depresses aggregate GM% by 30bps per year. Those are margin points that this model can’t afford to lose.

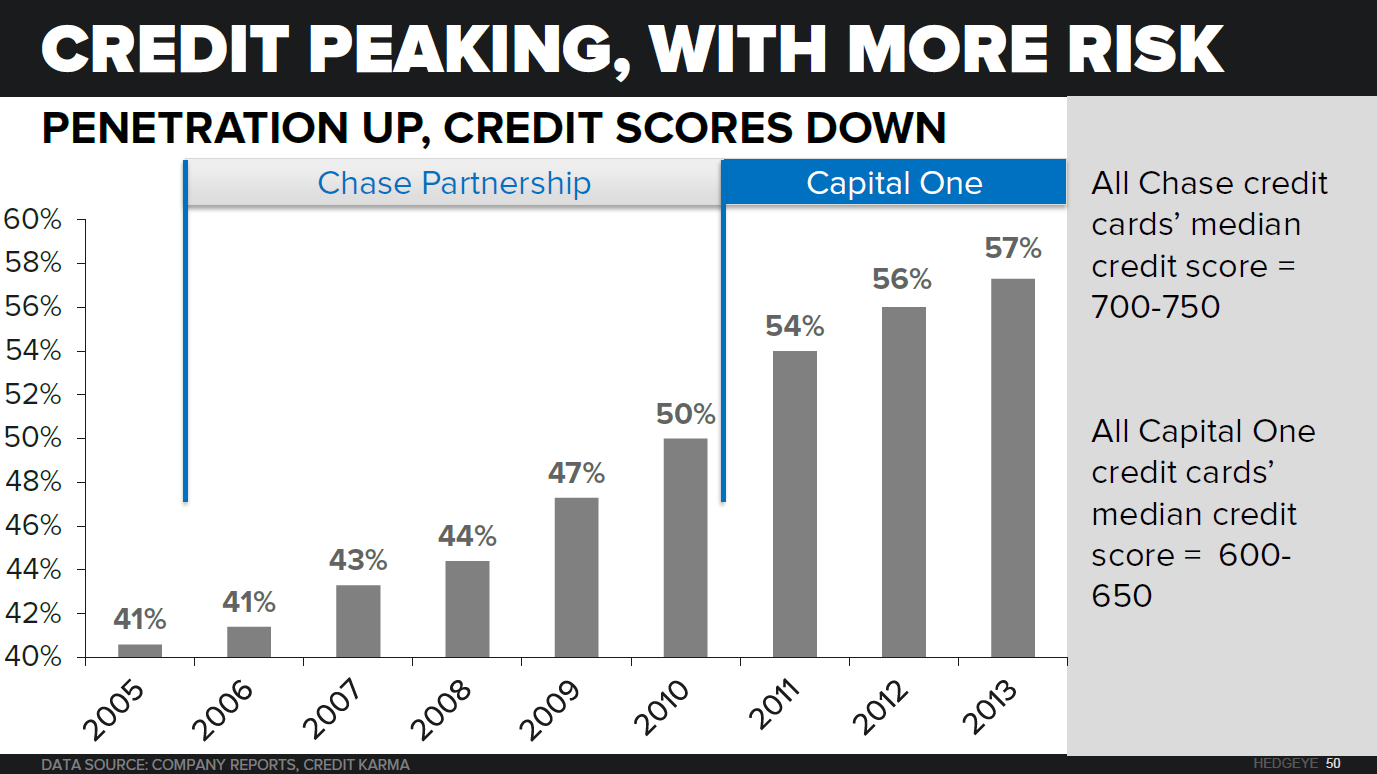

Point 7: Keep An Eye On KSS Credit

Many retailers have, or maintain, credit cards. It’s a solid tool to keep customers and incentivize them to spend more. But our consumer survey suggests that 18% of KSS shoppers have a rewards card. But more importantly, we know that 57% of purchases are made by that card. That is a simply staggering figure from where we sit. Three years ago KSS shifted its partnership from Chase to Capital One. But median credit scores for Chase customers range between 700-750, which are optimal for a mid-tier retailer. But the 700bps in card penetration that KSS saw under Capital One came at a median credit score of 600-650. Basically, this tells us that incremental sales growth is likely coming from more marginal consumers. This is not exactly a smoking gun on the short side, but taken in context with the other pressures we see to the model, it certainly does not bode well.