This note was originally published at 8am on October 30, 2014 for Hedgeye subscribers.

“How many a dispute could have been deflated into a single paragraph if the disputants had dared to define their terms?”

-Aristotle

Are you a central planning disputant? I am, big time. So, please, allow me to define my terms:

- The Fed’s QE was a Policy To Inflate asset prices

- After that inflation, you get the #deflation

That is all.

Back to the Global Macro Grind…

I know. So easy a Mucker can explain it.

If you’d like to have a dispute with me on these terms (or change the M in my nickname to an F like the 1997 Princeton Hockey Team did), I’m happy to have it as long as you define yours. Mr. Market has been pricing them in all year long.

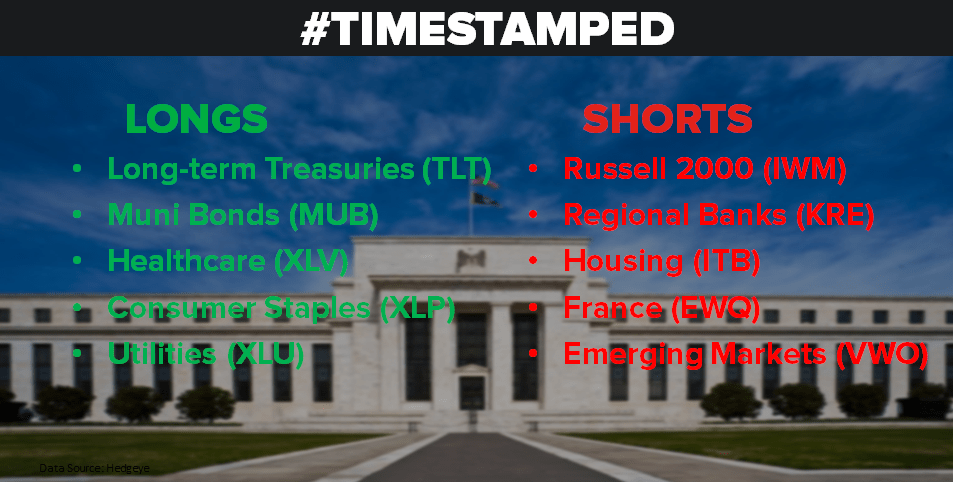

When our #process signals #Quad4 deflation (growth and inflation slowing, at the same time) here’s our asset allocation:

- Cash

- Long Term Treasuries (TLT, EDV, etc.)

- Municipal Bonds (MUB)

- Healthcare Stocks (XLV)

- Consumer Staple Stocks (XLP)

We #timestamped that in our Q4 Macro Themes deck on October 1st (pre-Oct 14th fetal position for the levered long beta portfolios) and we’ll reiterate that again, now that the Fed has done precisely what they said they’d do (ending the Policy To Inflate).

Now that that’s over, what I think happens next is where I’ll have many disputes. Here’s what I’m thinking:

- As both US and Global growth slows, the Fed will be under pressure to say that they can provide moarrr #cowbell

- Mean Reversions: classic late-cycle indicators (like employment and “confidence”) should roll over; Fed will freak out on that

- Long-term rates will continue to make a series of lower-highs and lower-lows, tracking lower growth and inflation expectations

Again, think like a Fed head. Define their terms – then front-run their proactively predictable behavior.

The main problem my disputants have with me is that I don’t think like they do. I am a dynamic counter-cyclical strategist and they are pro-cyclical linear economists. The economy is non-linear. It’s also one massive cyclical. You don’t buy a cyclical at the top of a cycle – you sell it.

The #1 question you should be asking Ed & Nancy (linear economists) has two parts:

A) After 65 straight months of US economic expansion, isn’t this an early-cycle slowdown, and

B) Now that everyone has cut to zero, where are we in the worldwide easing-cycle?

We know how they think about this. They’re making the same calls that they made at the top of prior cycles (that the cycle wasn’t slowing in 2H of 2007). They have defined their surveys and their terms. Those are pro-cyclical too.

What does being pro-cyclical mean?

- That you think late-cycle indicators being good is good

- That you don’t think in 2nd derivative terms (going from great to good is bad)

- And that once things are actually bad, you’re both late and getting bearish a lot lower

No, I’m not calling anyone names. I am not being “mean” either. Rather than drifting from bullish to bullish thesis on the economy (at the beginning of the year they said inflation and capex would drive the economy; now they are saying global slowing and deflation will), I am being a consistent disputant.

This morning I’ll list the Top 12 Big Macro Risk Ranges (and our TREND views in brackets) – they are in our Daily Trading Ranges product too:

UST 10yr yield 2.16-2.35% (bearish)

SPX 1871-2007 (neutral)

RUT 1071-1157 (bearish)

DAX 8709-9340 (bearish)

VIX 12.89-22.25 (bullish)

USD 85.34-86.24 (bullish)

EUR/USD 1.25-1.27 (bearish)

Yen 107.11-109.77 (bearish)

WTI Oil 79.98-83.05 (bearish)

Natural Gas 3.57-3.82 (bearish)

Gold 1194-1231 (neutral)

Copper 2.96-3.09 (bearish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer