TODAY’S S&P 500 SET-UP – November 10, 2014

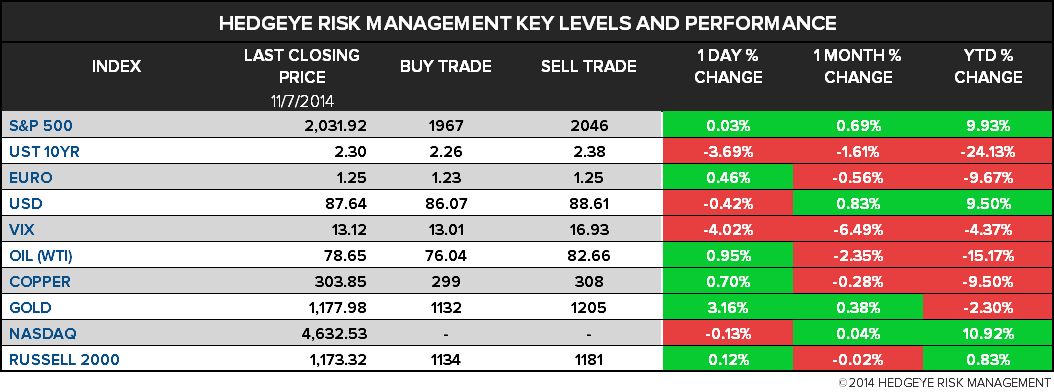

As we look at today's setup for the S&P 500, the range is 79 points or 3.20% downside to 1967 and 0.69% upside to 2046.

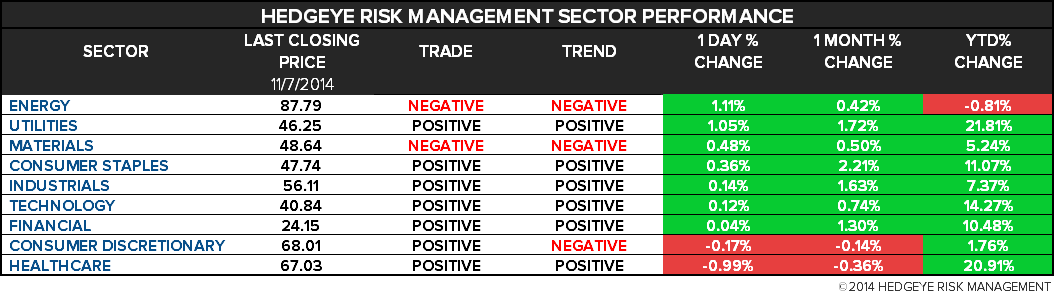

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.79 from 1.80

- VIX closed at 13.12 1 day percent change of -4.02%

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: Fed Labor Mkt Conditions Index, Oct.

- 11am: U.S. to announce plans for auction of 4W bills

- 11:30am: U.S. to sell $24b 3M bills, $28b 6M bills

- 1pm: U.S. to sell $26b 3Y notes

- 5:10pm: Fed’s Rosengren speaks at Washington and Lee University, Lexington, Va.

GOVERNMENT:

- President Obama travels to China, Myanmar, Australia through Nov. 16

- Sec. of State John Kerry meets with former EU High Representative Catherine Ashton, Iranian Foreign Minister Javad Zarif in Oman ahead of Nov. 24 deadline to reach deal preventing Iran from developing weapons

- Sifma conference: SEC Chairman Mary Jo White, 8:40am; Stephen Luparello, director SEC’s trading and markets division, 2:15pm

- 9:30am: Supreme Court issues orders on pending cases

WHAT TO WATCH:

- Boeing Wins $8.5b SMBC Aviation Order on Asian Jet Demand

- Dendreon Starts Voluntary Chapter 11 Proceedings

- Berkshire Profit Slips After Buffett’s Tesco Investment Falters

- Obama Accepts Blame for Results of U.S. Midterm Elections

- Obama Administration Offers Preview for 2015 Health Plans

- Obama Faulted for Having Fewer Experts Guiding China Policy

- Paulson Event Fund Said to Plunge 14% in October as Loss Worsens

- Merck’s 4-Week Hepatitis C Regimen Fails to Beat Gilead Drug

- American Attendants Reject Contract in Defeat for Merged Airline

- Takata Falls to Five-Year Low After Calls for Criminal Probe

- Time Warner Approached Ten About Potential Takeover: AFR

- Uber Said in Early Talks to Raise $1 Billion to Fund Growth

- U.S. Gasoline Falls to $2.9421 a Gallon in Lundberg Survey

- Bank of Russia Cuts 2015 Economic Forecast to Show No Growth

- China Factory-Gate Prices Decline for Record 32nd Month

- Disney’s ‘Big Hero 6’ Outdraws ‘Interstellar’ at Box Office

- SHV Raises Nutreco Takeover Bid to Fend Off Cargill Interest

- Transocean Posts Qtr Net Loss $6.12/Shr on Goodwill Impairment

- GM Ordered New Switches Before Recall, E-Mails Show: WSJ

- BARRON’S ROUNDUP: Telecom Fight, J.C. Penney, Leucadia, Kellogg

AM EARNS:

- 3D Systems (DDD) 8:30am, $0.17

- Dean Foods (DF) 8am, ($0.13)

- Gogo (GOGO) 7:30am, ($0.26)

- Quicksilver (KWK) 7:30am, ($0.09)

- Rayonier (RYN) 8am, $0.19

- Sotheby’s (BID) 8am, ($0.35)

- Turquoise Hill (TRQ CN) Bef-mkt, $0.02

- WhiteWave Foods (WWAV) 8am, $0.26

PM EARNS:

- Acadia Pharmaceuticals (ACAD) 4:01pm, ($0.22)

- Atwood Oceanics (ATW) 4:49pm, $1.55

- Caesars Entertainment (CZR) 4:01pm, ($1.47)

- Cumulus Media (CMLS) 4pm, $0.07

- Forest Oil (FST) 5:08pm, ($0.06)

- Halcon Resources (HK) 4:15pm, $0.06

- Halozyme Therapeutics (HALO) 4:15pm, ($0.14)

- Inter Parfums (IPAR) 4:05pm, $0.36

- Legacy Oil + Gas (LEG CN) Aft-Mkt, C$0.09

- NPS Pharmaceuticals (NPSP) 4:30pm, $0.02

- ParkerVision (PRKR) 4:01pm, $0.01

- PDL BioPharma (PDLI) 4:09pm, $0.56

- PRA (PRAA) 4pm, $1.11

- Rackspace (RAX) 4pm, $0.16

- Resolute Energy (REN) Aft-Mkt, ($0.06)

- Towerstream (TWER) 4:01pm, ($0.10)

- Wayfair (W) Aft-Mkt, ($0.37)

- Woodward (WWD) 4:05pm, $0.78

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Gold Declines After Biggest Advance Since June on U.S. Outlook

- Brent Oil Reaches One-Week High as China Exports Exceed Forecast

- Kuwait Oil Minister Sees No OPEC Output Cut at Next Meeting

- Gold Bulls Trim Bull Wagers at Fastest Pace of Year: Commodities

- Rebar Climbs by Most in a Week Amid Output Cuts, Record Exports

- Corn to Soybean Price Forecasts Cut by Morgan Stanley on Supply

- Iron Ore Seen Extending Declines by ANZ as Global Glut to Double

- Port Hedland Officers, Deckhands Settle as Engineers to Strike

- Bullish Oil Bets Cut in Sign of Growing OPEC Skepticism: Energy

- Kuwait Oil Minister Sees No Decrease in OPEC Crude Output

- Global Oil Market Oversupplied by as Much as 1.5m B/D: PIRA CEO

- Corn Extends Decline Before USDA Report Set to Show Ample Supply

- Rayonier Cuts Dividend, Restates Earnings on ‘Material Weakness’

- Kashagan Oil Field Seen by Total Producing by 2017 at the Latest

- Zinc Climbs for Third Day as Chinese Exports Exceed Estimates

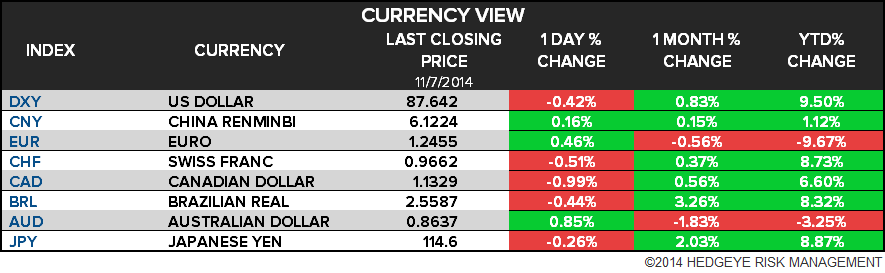

CURRENCIES

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team