HAIN in on the Hedgeye Best Ideas list as a SHORT.

HAIN reported earnings yesterday, and the quarter was less than natural. The company missed revenue estimates, while conveniently beating EPS estimates by $0.01. While the bulls will likely point to the success of its roll-up strategy, there are a number of cracks that are beginning to appear in management’s story. We believe these will manifest into bigger issues as we progress over the balance of FY2015.

While we attribute most of the stock’s hype to that surrounding organic food companies in general, we tend to believe the street has placed the CEO on a pedestal. This typically raises a red flag for us because, in our experience, it can lead to a number of issues, including:

- Management incentives are often short-term

- Significant insider selling

- Charismatic CEOs tend to stand above the company

- The more successful the CEO, the less he/she is held to account

- Symbiotic board/CEO relationship results in excessive compensation

- Management tends to overstate the growth it is seeing

Does any of this sound familiar to companies you’ve come across in the past? How did those stories end? HAIN certainly fits the bill. In our view, this is a classic bubble stock and the company is not being built to last.

The following are some of our thoughts about 1Q15:

INCREASING ADJUSTMENTS

We’ve never seen a company make such a large, and increasingly large, number of adjustments in their quarterly reports. Regarding 1Q15, the sheer size of the adjustments and the rate of growth on a year-over-year basis are staggering. How can any portfolio manager be okay with this? How can you not question the quality of earnings the company is producing? As we laid out above, charismatic, well-liked CEOs tend to have their word taken at face value because people want to believe in it.

IS HAIN OVERSTATING ITS ORGANIC GROWTH RATE?

Consistent with what you’d expect from a company that must adjust number to hit EPS estimates, we believe HAIN is overstating its true organic growth rate, which management said was 8% on a global basis in the quarter. Given the numbers they presented, it is very difficult for us to get to this 8% organic growth rate, particularly when considering that we estimate the organic growth rate in the US in 1Q15 was a mere 4.6%. Based on our math, this represents a 180bps sequential slowdown.

OPAQUE BUSINESS MODEL

HAIN operates a very opaque business for such a hyped up stock. Management wants you to believe they are disclosing everything you need to understand the underlying trends of the business, but this is far from the truth. In fact, in this regard, they virtually give you nothing beneficial. What they do give simply masks the real issues. To make matters worse, deceit and obfuscation are prevalent during quarterly earnings call.

MARGIN PRESSURE

In 1Q15, adjusted gross margin was 23.5% (down 156 bps y/y) due to the acquisition of Hain Pure Protein. Management has guided to a 150-160 bps gross margin decline for the full year. To offset this decline, the company cut SG&A by 170 bps and guided to another $50 million in SG&A cuts in FY15. How long can they push this line lower? It’s a trend that we believe is highly unsustainable and also one that suggests the company in underinvesting in its brands.

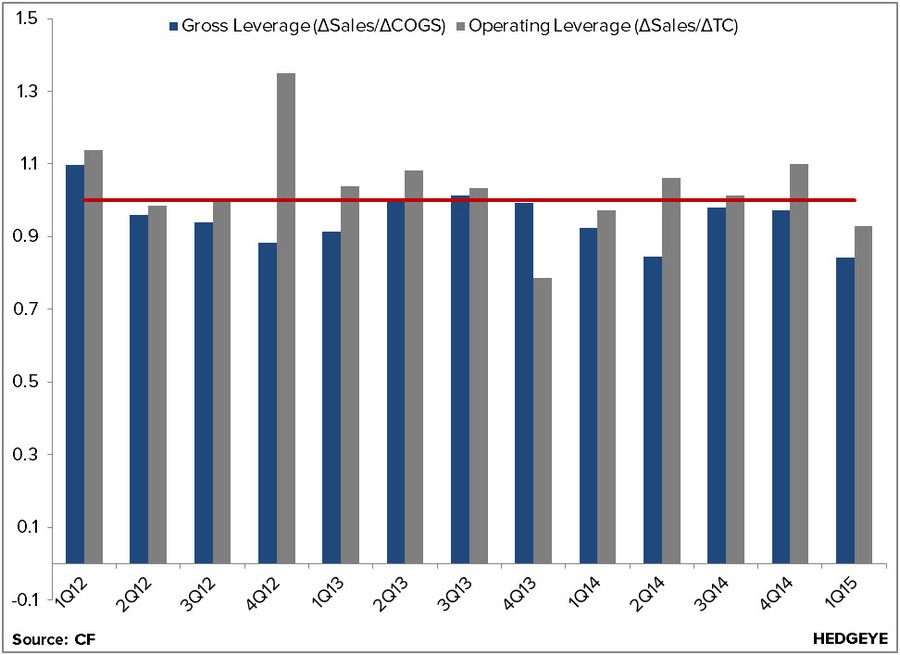

Roll-up strategies generally work so long as the company maintains positive economies of scale. As you can see below, this is precisely what HAIN is failing to do.

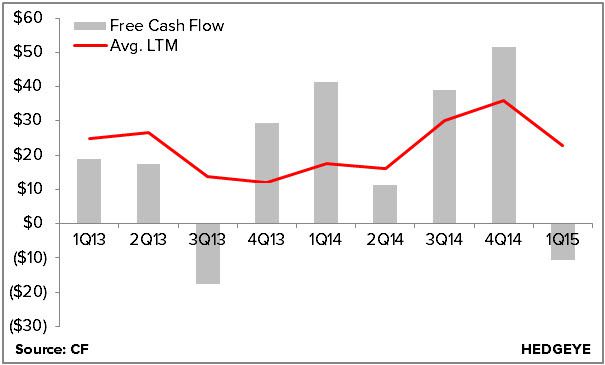

FREE CASH FLOW

The company did not generate any free cash flow in the quarter.

BALANCE SHEET

Inventories have been growing faster than sales for the past several quarters. This is consistent with a slowing core business.

OTHER ISSUES

Other issues are beginning to manifest, including:

- HAIN’s supply chain – MaraNatha could be the tip of the iceberg

- Private label competition is increasing

- Penetration

- Suspect financials

We believe this story is beginning to unravel.

Feel free to call, or email, with questions.

Howard Penney

Managing Director

Fred Masotta

Analyst