Yesterday the Ministry of Finance announced that it would extend its support for Cinda Asset Management, one of the four primary AMCs set up to absorb bad loans from commercial bank books over the past decade, for 10 additional years. Cinda currently holds more than $36 billion in bad loans purchased from China Construction Bank, an amount equal to more than half CCB’s net assets. CCB officially has a non-performing loan ratio of 2% excluding “special mention” assets.

Although no one was surprised that the AMCs life will be extended rather than see massive mark downs hit the balance sheet of the financials they sprang from, the expectation of many observers has been that Beijing would rather see the companies take on new business as agencies which could ultimately allow the debt to be supported without direct government support. Instead the government appears to be signaling a willingness to allow these pools of zombie assets stagger on without any new plan for recouping losses on these troubled debt portfolios.

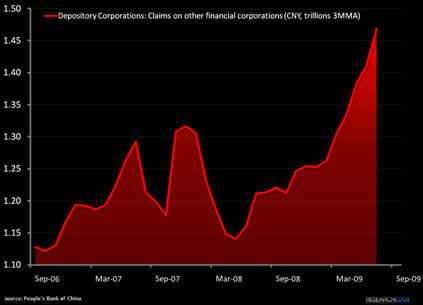

As the extension of credit between financial instructions continues to grow rapidly (see chart below) the expectation that the system will be able to support liquidity hinges heavily on government backing for the AMCs . As the Chinese become more acclimated to capitalism, they will have come to recognize that denial can have catastrophic consequences -with the policy makers and bankers in both the US and Japan providing cautionary examples.

Andrew Barber

Director