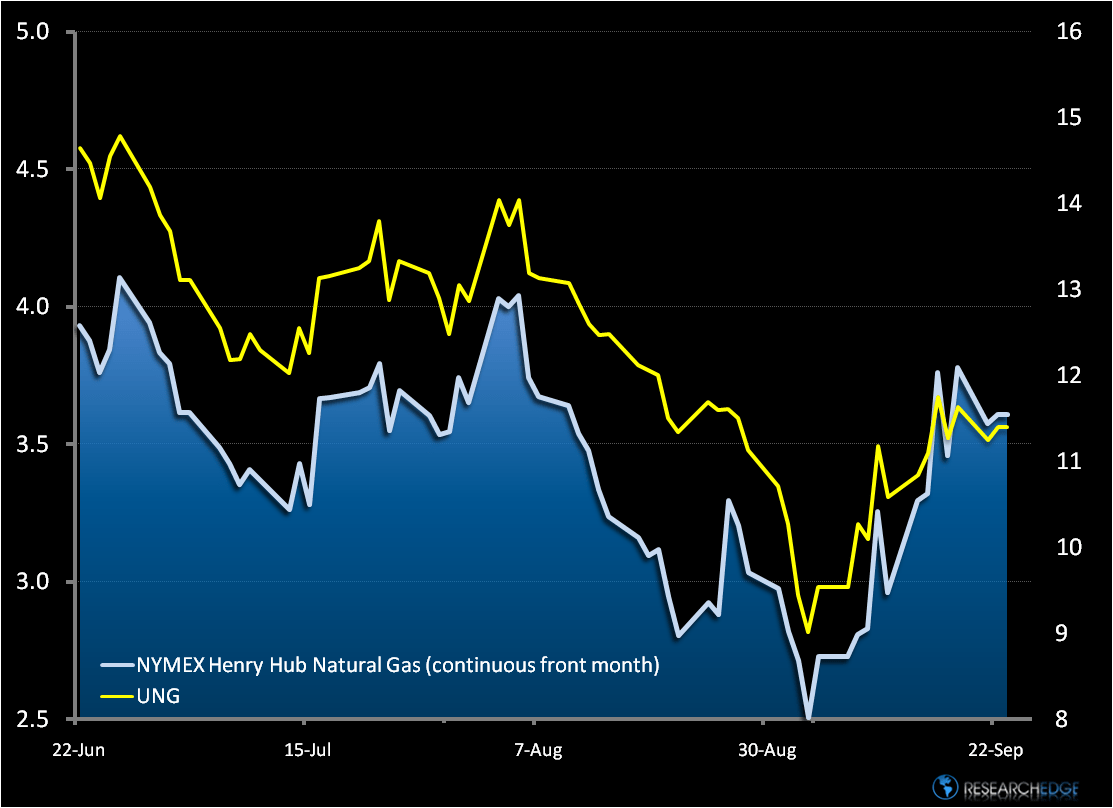

We have thankfully stayed on the sidelines of the natural gas market this year and used our commodity wherewithal to successfully trade the oil and gold markets. Broadly, commodities have been “ripping” this year on the back of U.S. dollar weakness and the perception of future inflation. As many of you know, natural gas has much different price drivers than its commodity peers. It is both a local commodity and very seasonal in nature.

I grew up in the heart of the Western Canadian Sedimentary Basis (“WCSB”) in a little prairie outpost called Bassano, which is in the Canadian province of Alberta. Only three things come out of Bassano – farmers, oil field workers, and hockey players. I was the latter. Despite the luck, or perhaps misfortune in inflationary times, of being better at playing hockey versus growing wheat or drilling for oil / natural gas, I still know a thing or two about those commodities. As it relates to natural gas, I can definitely tell you, supply matters.

Our Lead Desk Analyst Andrew Barber put together a chart below that outlines the supply of natural gas going back ten years. As we can see, inventories for natural gas have been building steadily since September 2008, which has led to the dramatic and steady decline we have seen in the price of natural gas.

Portfolio managers at commodity funds across the continent are chasing performance and natural gas is the most washed out commodity. Naturally, they are asking their analysts, “Should we buy? Should we buy? Should we buy?”. Everyone wants to call the bottom and natural gas does look washed out on many metrics. That said, the supply data is bearish and likely to get worse. So we have a classic game of chicken going on. The analysts know that fundamentals are bad, but the portfolio managers know that from a price perspective there is massive potential upside in “Natty”. So, who will budge first, the price or the fundamentals?

Admittedly, we’ve had the same scenario internally. Keith has hit me with his levels on the natural gas, and noted breakouts from a trade perspective, but I’ve had a hard time telling him I think he should pull the trigger. Currently, as of the month of September, natural gas inventories in the United States are 17.7% above their 10-year average (the September bar on the bottom chart).

Natural gas collapsed in August because storage levels were butting up against 80%, which is the max they can be prior to September, so excess natural gas was sold into the market, which depressed prices. Storage can now be filled to 100% of capacity, so excess natural gas has been going into storage in September versus sold into the market, which has been a key driver of the price of natural gas this month. Obviously, the commodity was also dramatically oversold and the economic outlook has improved, which have helped the rally.

Last week storage hit 88.9%, which is its highest level since 2006. This is noteworthy in that we are only halfway through the month and storage will likely be at 100%, or close to it, by the end of the September. The implication of this is that we may revisit the price dynamics of August in which no more gas could go into storage, so it was sold to the market which pushed prices down again. This is obviously a short term dynamic, but I have to be honest, high inventories and the potential reality of storage being filled by late September are making me a little . . . ummm . . . chicken.

Daryl G. Jones

Managing Director