Although Outback Steakhouse is out of the public eye, it does not mean that what it is doing is not important. We know that business is tough for Outback Steakhouse, as the company reported last month that same-store sales at the Outback dropped 10.4% in the second quarter ended June 30. Clearly, the company needs to do something to change the perception of the concept, outside of just lowering menu prices.

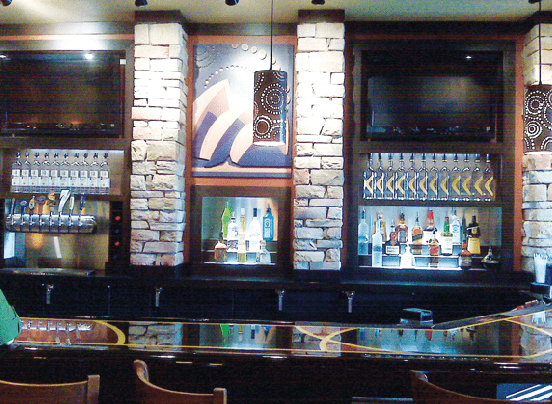

The following are a few pictures of the remodels the company has done in Florida and Virginia. With 900 units in the US, Outback is a competitor that should not be forgotten. Just something to keep in mind as it relates to the other steakhouse competitors.