The MGM lion is roaring. Is it justified? If I were management I’d issue a serious amount of stock and solve the balance sheet issues in one fell swoop.

The stock is up 72% in September alone. Thankfully, we haven’t been negative on the name but we weren’t pushing it as a long either. Shame on us. So is it time to take a stand?

A weak upgrade yesterday helped push the stock up another 7% and pushed me over the edge. I won’t dwell too much on the upgrade but 11x $1.5bn in 2010 in EBITDA gets me to about $8 per share, not $18. I’ve covered this industry a long time and an 11x multiple for mostly LV assets is about 2 turns higher than the average multiple over the last 10-15 years, and that’s for companies that were leveraged on average 4-5x, not 8x. I guess an 11x multiple makes sense if one assumes a sharp V-shaped recovery. The days of cost of borrowing being 3%, 20%+ annual increases in home prices, and negative savings rates are long gone. MGM won’t be approaching its peak EBITDA of $2.4bn in EBITDA for many, many years and there won’t be a v-shaped recovery. Oh and I think $1.5bn in 2010 EBITDA is too high.

We were in Las Vegas this past week and it’s clear that business has picked up. However, the improvement stems from: 1) seasonality and 2) easier comparisons. Neither of these provides much comfort that the underlying metrics are improving. Vegas seems to be bouncing along the bottom. I would argue that we are not even in recovery mode, never mind a V-shaped recovery as implied by MGM’s valuation.

CityCenter is obviously a big potential catalyst, positive or negative. We toured the construction site and I must admit that I was impressed. The big issue is whether or not CityCenter can grow the market. Does it have enough “special sauce” to drive visitation to the city to offset the huge capacity increase. We calculate CityCenter’s 6k rooms will raise high end Strip room supply by over 30%. Even if CityCenter does okay, cannibalization of MGM’s existing 32k Strip rooms is the big issue. See our 07/17/2009 note, “PLENTY OF ROOMS AVAILABLE AT THE STRIP INN IN 2010”.

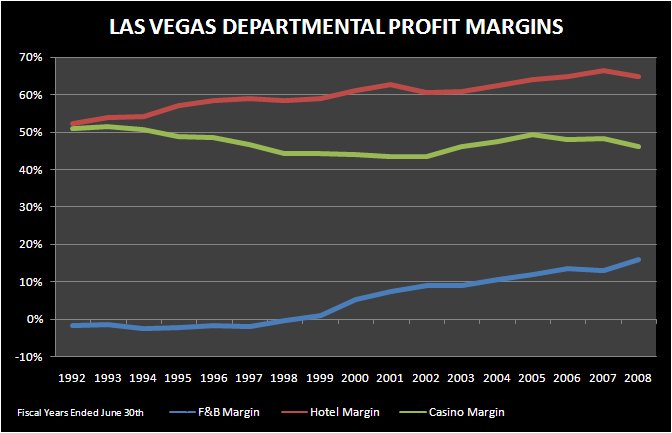

It’s all about room rates and maybe that’s why we are negative on Las Vegas next year and skeptical of a v-shaped recovery. We’ve written extensively on our view that Las Vegas was an exaggerated microcosm of the consumer bubble. National housing prices was statistically the most significant economic driver of Strip room rates over the last 15 years and drove almost all of the huge margin expansion experienced over that time period (see our updated Strip margin analysis, “FRAT BOYS AND LAS VEGAS” from 06/01/09). With housing plummeting, the savings rate climbing, and gaming’s share of the discretionary wallet declining, we are hard-pressed to believe that: a) a V-shaped recovery is forthcoming and b) room rates will approach their 2007/2008 peak any time soon.

The new Las Vegas is looking awfully similar to the old Las Vegas: low room rates keeping the gaming floor full. This model works, just not as well as the one that focused on 20%+ annual room rate increases.

With this thesis in mind, I would be issuing equity, straight or a convertible note. MGM is not out of the woods from a balance sheet perspective. As of 6/30/09, MGM was levered almost 8x. That’s high by any measure. Why not take the leverage risk off the table?