Dusting off our PCE analysis from last year and it’s even scarier now. Could regression to the mean be playing out for national casino revenues?

Prior to the consumer downturn beginning in the fall 2008, personal consumption expenditures were on a steep twenty-year incline. The consumer accounts for roughly 70% of GDP, but gaming was even more levered to the upturn than other consumer sectors. The higher one goes, the more pertinent gravity becomes. While the downside for many gaming stocks has been swift, in terms of where the American consumer spends his/her cash, there could be more downside in store.

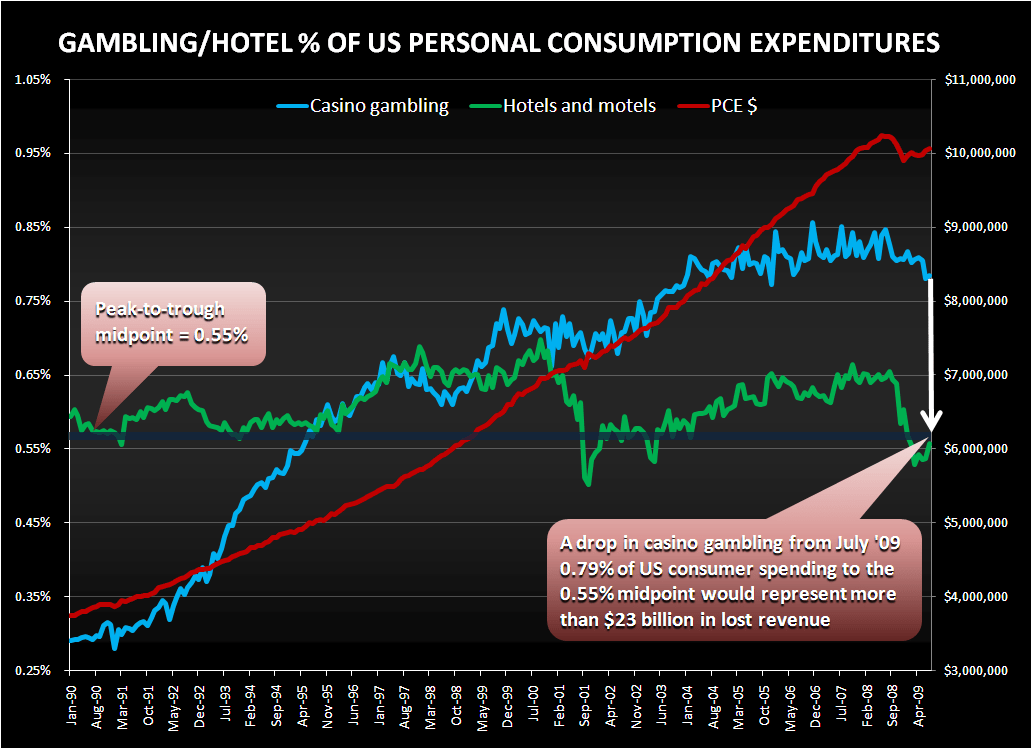

For the gaming industry, in our opinion, mean reversion is a highly relevant factor. As the chart below shows, gambling spend accounted for 0.8% of PCE in July 2009. The level peaked several times at around 0.85%, most recently in mid-2008. Mean reversion may already be occurring, as can be seen by the downward sloping blue line in the chart below. Why should 0.8% be the right number? Why couldn’t gambling expenditures fall to the 20 year mean of 0.55%? Or even go below that? After all, we are talking about discretionary spending that has proven to be highly tied to the economy, much to the surprise of many analysts.

Assuming mean reversion occurs, that would translate into a $23 billion annual loss for the industry or 30-35% from the current revenue level. I’m not making that prediction but I am saying that domestic gaming faces the potential double hurdle of a tight consumer and a smaller allocation of that consumer’s wallet.