This note was originally published at 8am on October 17, 2014 for Hedgeye subscribers.

“Didn’t I ever tell you? Bumbles Bounce!”

-Yukon Cornelius

Bounce that bumble! Oh yeah. I am going to go all Cornelius Yukon on you this morning! “The greatest stock picker (prospector) in the world!” VIDEO: https://www.youtube.com/watch?v=nsY2EeUuLj8#t=17

GenX kids like me loved this guy (so did our baby booming parents – just stick us in front of the TV and they were all set). For those of you who didn’t see Rudolph The Red Nosed Reindeer (initially released in 1964), Cornelius is a beauty.

After a rough week of dancing with the bear, here are some “high-conviction” Cornelius “picks”, I mean quotes:

“Terrible weather we’re havin’!”

“Open up! It isn’t a fit night out for man or beast”

“This is my land. And you know it’s rich with gold. Gooooollldddd!”

Back to the Global Macro Grind…

Ok. Maybe Captain Stock Picker didn’t think that was funny. Getting caught long in “the land” of levered bullish market beta wasn’t funny either. “So”, on this Bumble Bounce, do me a favor and recognize that the oncoming red light isn’t Rudolph – it’s a train.

Yep, open it up! Let this bounce rip to the high heavens of hope and sell-the-bumble-bounce #STBB. Because hope (that “everyone is bearish now”) is not a risk management process.

Neither is calling tops and bottoms. Remember, both are processes, not points. We’ll review the #process that got us bearish on both growth and inflation in the first place (before October’s “terrible weather”), on a Flash Call today at 1PM EST (email sales@hedgeye.com if you’d like access).

I’ll keep the call to 15 mins, then take the most important part of the call (your questions). Here are some levels to consider selling into as you “observe the bumbles one weakness (the bumble sinks! Ha ha!)”:

- UST 10yr Yield – immediate-term TRADE resistance zone of 2.22-2.31%

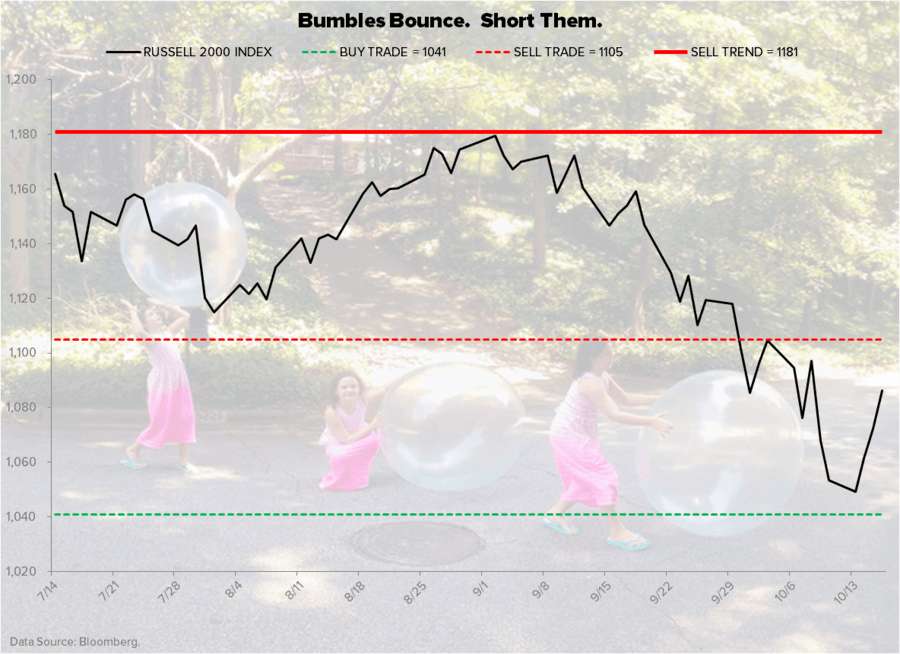

- Russell 2000 – immediate-term TRADE resistance = 1105

- SP500 – immediate-term TRADE resistance = 1889

*Note: I am not using the 200-day moving monkey as “resistance” – our #process is built to front-run that.

Don’t worry, I get it. You get it too. We are both allowed to change our minds in real-time. This is a dynamic and non-linear system of risk we are dealing with. Being wed to a chart, ice pick, and a moving monkey isn’t the answer.

While yesterday’s gap down open in both the Russell and SP500 recovered faster than I would have thought it could. Who cares what I thought? Mr. Market certainly doesn’t.

What we need to care about is where marked-to-market risk is right here and now. Then make the best risk management decisions we can make on the bounce. Chase or sell?

That’s why I show every move I’d be making if I was back in your seat (Real-Time Alerts). If you can think of a better way for me to show what I really think in the moment, let me know. But I’m thinking the #timestamp is the best I can do.

No, that doesn’t mean my #timestamps are always right. They’re not always wrong either. But I have been arguably dumber than Cornelius in showing you, literally, every move I’d have made (over 2,800 of them, long and short) since 2008.

Back to risk managing the bounce – some of the more interesting ones will come within risk ranges that are #crashing:

- Including this morning’s bounce to 2.18%, the 10yr UST Yield is still crashing, -28% YTD

- Including this morning’s whopping +0.5% bounce to $82.89, WTI Crude Oil is still crashing, -25% since June

- Including Europe’s bounce, both Greek and Portguese stocks are still crashing, -21-22% YTD

And why are these ex-ebola items #crashing?

- Bond Yields crash when growth expectations do

- Oil crashes in #Quad4, when both global growth and inflation expectations do

- Illiquid European stocks crash, well, every time they remind you the central plan didn’t work

Oh, then there’s the crash within the Russell itself. Over 62% of stocks in the Russell 2000 have crashed (-20% peak to trough drawdowns). By my math, that is a lot of pain that was not proactively prepared for.

But everyone is going to strike it rich with their small cap peppermint stock “picks”, on the bounce, right? “Peppermint! What I’ve been searching for all my life! I’ve struck it rich! I’ve got peppermint! Wahooooo!” (Cornelius again, sorry – couldn’t resist).

Right. Right. After very few prepared for the avalanche of small cap beta risk, everyone is going to triple-down on the bounce, and the bumbles will never sink again.

Roger that. And it really is different this time. It’s Rudolph, remember (not a train on globally interconnected #GrowthSlowing and deflation risk).

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.09-2.22%

SPX 1831-1889

RUT 1041-1105

DAX 8454-8895

VIX 20.74-28.92

Gold 1205-1251

Best of luck out there today,

KM