TODAY’S S&P 500 SET-UP – October 29, 2014

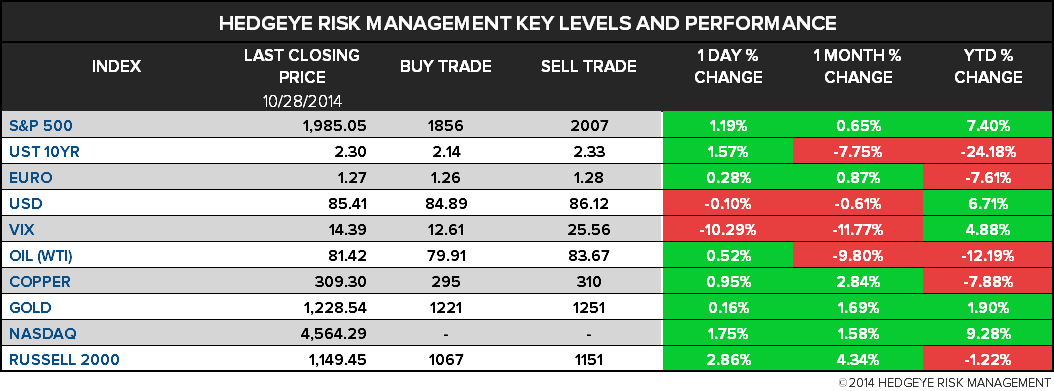

As we look at today's setup for the S&P 500, the range is 151 points or 6.50% downside to 1856 and 1.11% upside to 2007.

SECTOR PERFORMANCE

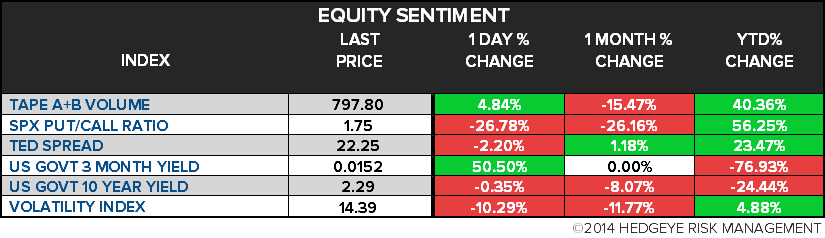

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.86 from 1.90

- VIX closed at 14.39 1 day percent change of -10.29%

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, Oct. 24 (prior 11.6%)

- 10:30am: DOE Energy Inventories

- 1pm: U.S. to sell $35b 5Y notes

- 2pm: Fed seen maintaining overnight bank lending rate 0%-0.25%; seen ending QE program

GOVERNMENT:

- Senate, House out of session

- Deadline for replies to FCC on $45.2b Comcast-Time Warner Cable deal

- 9am: Iraqi Ambassador to U.S. Luqman Abd al-Rahim Fayli delivers remarks on “Iraq-U.S. Relations: A View from Baghdad” at Arab-U.S. Policymakers Conf.

- U.S. ELECTION WRAP: Senate Races; Alaska Polls; McConnell Humor

WHAT TO WATCH:

- Fed Decision Day Guide: FOMC Seen Focusing on Too-Low Inflation

- Sanofi Chief Ousted After Tensions With Board Members

- Facebook Projects ‘More Difficult’ Quarter as CEO Spends

- Gilead Misses Profit Est. on Obamacare Fee, Lower Drug Sales

- Aflac Profit Climbs on Japan Bets in Dollar-Denominated Assets

- Tesla Owners Get $12,000 License Plates in Shanghai for Free

- Deutsche Bank Sinks to 3Q Loss on Provisions for Legal Costs

- Ares-Backed Floor & Decor Outlets Said to Plan $100 Million IPO

- Pimco Is Replaced by BlackRock at $6.16 Billion Prudential Fund

- Prudential Takes Stake in AFP Habitat After MetLife’s Chile Bet

- NASA Vows to Continue Commercial Rocket Program After Explosion

- Medicare Agency Said Focus of Insider Trading Probe: WSJ

- Obama Warns of Fear Hindering Ebola Fight as Quarantines Stick

AM EARNS:

- Alkermes (ALKS) 7am, $0.02

- Arrow Electronics (ARW) 8am, $1.31

- Automatic Data Processing (ADP) 7:30am, $0.60

- Booz Allen Hamilton (BAH) 7am, $0.41

- Cameco (CCO CN) 8:30am, C$0.21 - Preview

- Capitol Federal Finl (CFFN) 9am, $0.14

- Carlyle (CG) 6:30am, $0.52

- Commercial Metals (CMC) 7am, $0.25

- Dentsply Intl (XRAY) 7am, $0.60

- Eaton (ETN) 6:30am, $1.24

- Exelon (EXC) 7am, $0.72

- Garmin (GRMN) 7am, $0.71

- Goodyear Tire & Rubber (GT) 8:30am, $0.70

- Hershey (HSY) 7am, $1.08

- Hess (HES) 7:30am, $1.07 - Preview

- Hyatt Hotels (H) 7:30am, $0.26

- IAC (IACI) 7:30am, $0.66

- McGraw Hill (MHFI) 7:15am, $0.94

- Phillips 66 (PSX) 8am, $1.75 - Preview

- Praxair (PX) 6:02am, $1.62

- Prosperity Bancshares (PB) 6:04am, $1.07

- Ralph Lauren (RL) 8am, $2.05 - Preview

- Revlon (REV) 7:30am, $0.45

- Sealed Air (SEE) 7am, $0.45

- Sherritt (S CN) 7am, (C$0.07) - Preview

- SodaStream (SODA) 7:30am, $0.35

- Southern Co (SO) 7:30am, $1.07

- SPX (SPW) 6:30am, $1.38

- TE Connectivity (TEL) 6am, $1.00

- Valley National (VLY) 7:30am, $0.14

- Waste Management (WM) 7:30am, $0.68

- WellPoint (WLP) 6am, $2.26 - Preview

- Wisconsin Energy (WEC) 7am, $0.52

PM EARNS:

- Agnico Eagle Mines (AEM CN) 5:15pm, $0.15

- Akamai Technologies (AKAM) 4:01pm, $0.57

- Allstate (ALL) 4:05pm, $1.34

- Arch Capital (ACGL) 4:11pm, $0.98

- Arris (ARRS) 4:01pm, $0.72

- Assurant (AIZ) 4:05pm, $1.61 - Preview

- Atmel (ATML) 4:05pm, $0.12

- Avis Budget (CAR) 4:30pm, $1.80

- Axis Capital (AXS) 4:32pm, $1.21

- Baidu (BIDU) 4:30pm, $10.37

- Barrick Gold (ABX CN) 5pm, $0.17

- CBRE (CBG) 4:05pm, $0.35

- Cirrus Logic (CRUS) 4pm, $0.56

- Cloud Peak Energy (CLD) 4:10pm, $0.03

- DreamWorks Animation (DWA) 4:02pm, $0.05

- Duke Realty (DRE) 4:07pm, ($0.02)

- Equinix (EQIX) 4:01pm, $0.90

- F5 Networks (FFIV) 4:05pm, $1.48

- Flextronics Intl (FLEX) 4:01pm, $0.24

- FMC (FMC) 4:30pm, $0.96

- FNF (FNF) 4:04pm, $0.54

- Fortune Brands (FBHS) 4:01pm, $0.56

- Hanesbrands (HBI) 4:01pm, $1.68

- HudBay Minerals (HBM CN) 5:11pm, C$0.06

- Intersil (ISIL) 4:05pm, $0.20

- JDS Uniphase (JDSU) 4:05pm, $0.10

- KapStone Paper (KS) 4:15pm, $0.66

- Kraft Foods (KRFT) 4pm, $0.74 - Preview

- LifeLock (LOCK) 4:05pm, $0.15

- Lincoln National (LNC) 4:10pm, $1.43 - Preview

- Lundin Mining (LUN CN) 5:30pm, $0.07 - Preview

- MetLife (MET) 4:05pm, $1.38 - Preview

- Moelis (MC) 4:05pm, $0.39

- Murphy Oil (MUR) 5:32pm, $0.99

- Noble (NE) 5pm, $0.55

- Norwegian Cruise Line (NCLH) 4pm, $1.08

- Oceaneering Intl (OII) 5:02pm, $1.13

- Penn Virginia (PVA) 4:10pm, ($0.09)

- Pilgrim’s Pride (PPC) 4:45pm, $0.79

- Qiagen (QGEN) 4pm, $0.27

- Questar (STR) 4:14pm, $0.18

- Range Resources (RRC) 5:01pm, $0.33

- Raymond James Finl (RJF) 4:16pm, $0.85

- Realty Income (O) Aft-mkt, $0.23

- RF Micro Devices (RFMD) 4pm, $0.27

- Service Intl (SCI) 4:05pm, $0.24

- Suncor Energy (SU CN) 10pm, C$0.77 - Preview

- SunPower (SPWR) 4:05pm, $0.23 - Preview

- Superior Energy Services (SPN) 4:15pm, $0.54

- Take-Two Interactive (TTWO) 4:05pm, ($0.59)

- Terex (TEX) 5:17pm, $0.61

- Trulia (TRLA) 4:01pm, ($0.09)

- Unum (UNM) 4:05pm, $0.90 - Preview

- US Silica (SLCA) 5:31pm, $0.69

- Validus (VR) 4:15pm, $1.12

- Visa (V) 4:05pm, $2.10 - Preview

- Weight Watchers (WTW) 4:05pm, $0.48

- Whiting Petroleum (WLL) 4pm, $1.21

- Williams Cos (WMB) 4:15pm, $0.19

- Yamana Gold (YRI CN) 4:20pm, $0.06

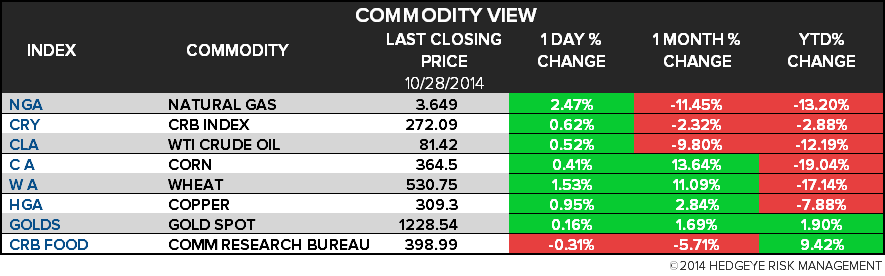

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Pirates Target Oil Tankers in Asia Trade Route as Attacks Climb

- OPEC Says Shale Producers First to Suffer From Oil-Price Plunge

- Mistry Predicts Palm Oil Rally as ‘Worst Over’ on Falling Output

- ADM Investing $3 Billion to Make Food Taste Better: Commodities

- Russia Adds Gold to Reserves in Sept. as Mexico Cuts: IMF Data

- MORE: Indonesia Seeks to Mediate Freeport, Labor Union Meeting

- Palm Area in Indonesia Seen Jumping 18% to 11m Hectares by 2020

- Soybeans Gain on Brazil Drought as Wheat Rises on Russia Concern

- OPEC Discounts Shunned by Algeria as Crude Goes to Venezuela

- China Oil Trader in Record Mideast Crude Haul as Prices Drop

- Breathing Cleaner Air Has Cost as Utility Bills to Surge in U.S.

- Shanghai Rebar Rises as Mills Seen Cutting Output During APEC

- Freeport Copper Output Falls at Grasberg After Workers Protest

- WTI Crude Rises to Four-Day High as Fuel Demand Seen Expanding

CURRENCIES

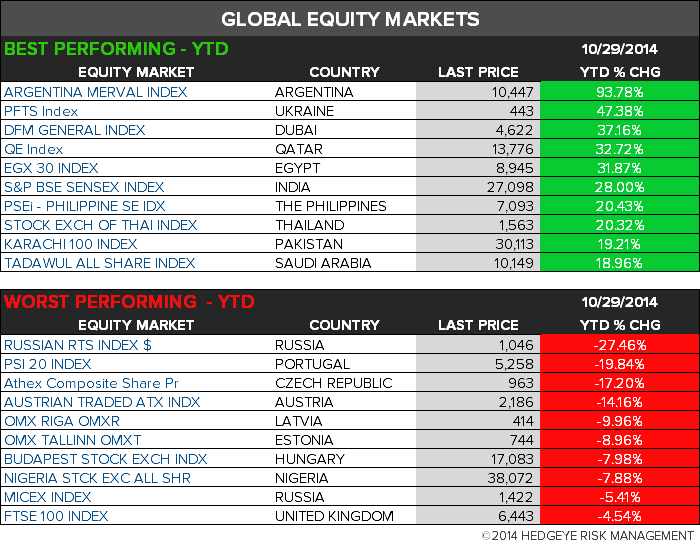

GLOBAL PERFORMANCE

EUROPEAN MARKETS

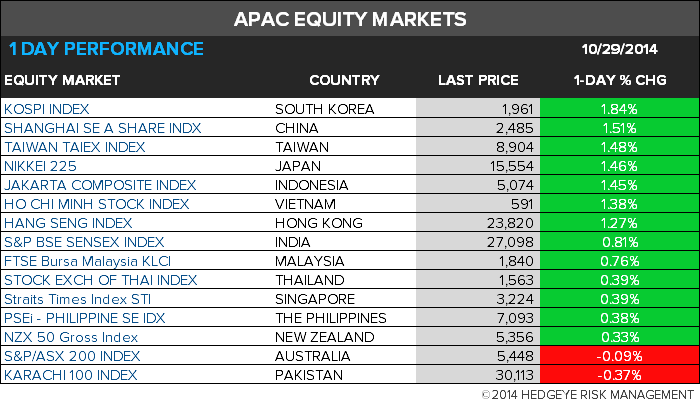

ASIAN MARKETS

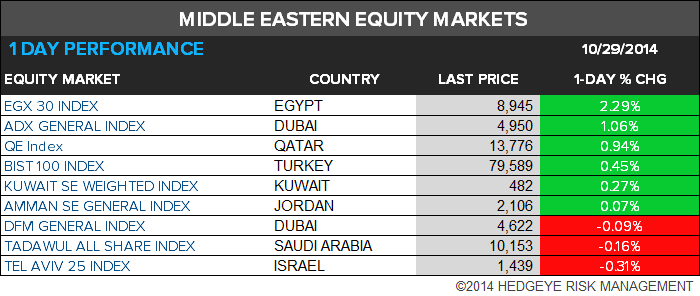

MIDDLE EAST

The Hedgeye Macro Team