“Certainty is the mother of quiet and repose; uncertainty the cause of variance and contentions.”

-Edward Coke

Edward Coke was Chief Justice of the King’s Bench in the early 17th century. His aforementioned quote is dead on when I think about it in the context of modern central planning ideology.

Many want un-elected bureaucrats and benches (like the Federal Reserve) to deliver them the elixir of certainty, quiet, and repose. Unfortunately, markets and economies can’t be centrally planned that way. They are grounded in uncertainty and contention.

“Variance” was a thoughtful word for a judge to be using way back then. It’s too bad that the Fed doesn’t talk in these terms. Variance (how far a set of numbers spread out) and correlation risks are at the heart of what modern Macro Risk Managers think about every day.

Back to the Global Macro Grind…

The variance between how political types talk about market risks and how practitioners on the buy-side explain them continues to widen.

That’s not a good thing. With time, humans aren’t supposed to get dumber.

That said, into both the almighty central planning decision tomorrow (Fed meeting) and Q3 GDP report this week, “should I be turned into a vegetable or a happy imbecile?” (Taleb, pg 61 of Antifragile)

Great question! I actually get asked some version of that question, a lot. Bob Brooke, Darius Dale, and I spent all of yesterday meeting with Institutional Investors in Boston. And one of the underlying questions remains – ‘what if it’s different this time?’

A: It’s not.

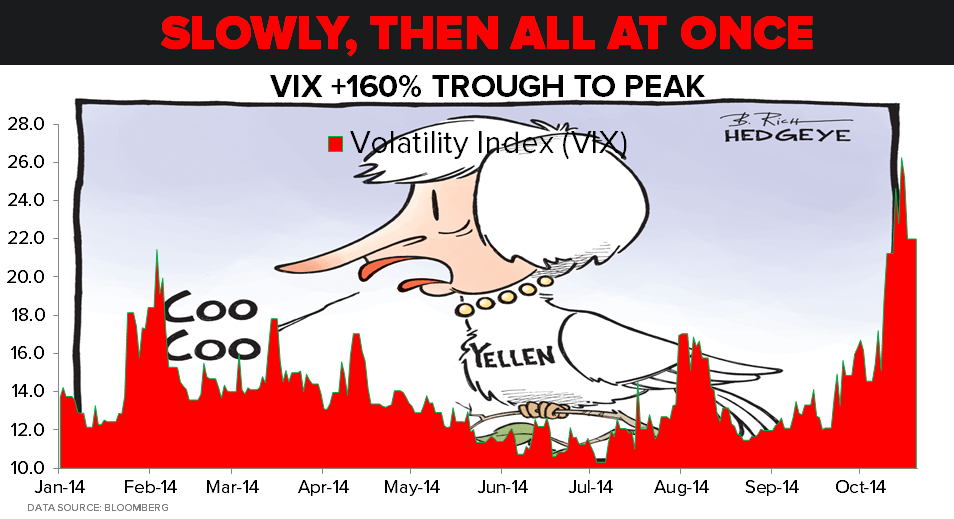

What we call #Quad4 deflation is like gravity – it occurs slowly, then all at once.

One of the best ways to observe which “Quad” the market is trending towards is through what modern day risk managers call Sector Style Factors (the variance of the stock market’s sector returns):

- When Sector Variance is LOW (like all-time lows in 2013) a monkey can be right on the long side (every sector goes up)

- When Sector Variance is RISING (like now), sector returns diverge, and momentum monkeys fall from the trees

Low-variance is the birth-child of compressed (low) volatility. And, to a large extent, that’s what the Fed is trying to promise you, in perpetuity. How else could an un-elected ideology live, unless it delivered political “certainty”, forever!

Then, non-linear market risks do what they do, and volatility rips +160% to the upside in 3-4 months (from the all-time #RussellBubble high of July 7th, 2014 to mid-0ctober) and the Fed needs to “smooth” that with the next central plan.

Or so they think…

And what happens when the next central plan loses credibility in delivering the one thing every political animal who has empowered the Fed is whining about when they stump about “inequality” (with the one thing being inflation)?

Oh, the #deflation.

Look at yesterday’s market action, in Sector Variance terms:

- Energy Stocks (XLE) down another -2.1% on the day to -7.53% for OCT to-date

- Basic Material Stocks (XLB) down another -2.1% to -4.68% for OCT to-date

- Healthcare Stocks (XLV) up another +0.1% to +2.14% for OCT to-date

Yep, since Healthcare (XLV) and Consumer Staples (XLP) are the only Sector Styles you’d be really net long of in Hedgeye #Quad4 terms right now (versus short the commodity #deflation sectors), it looks like Mr. Market is confirming a loss of the Policy To Inflate’s credibility.

And what happens after all 3 of the major central planning committees (Fed, BOJ, and ECB) have already cut to zero? Oh, it looks like Sweden is cutting to 0.00% (from 0.25% prior) this morning. Maybe European stocks can go up for another 4 hours on that.

As both volatility and variance risks are rising, the other big market risk that develops is called mean reversion risk.

In other words, now that Healthcare stocks (XLV) are +17.8% YTD (versus Energy -5.3%), prudent Portfolio Managers starts to ask themselves how much more they can pay up to chase Healthcare stocks.

Unless it’s different this time (it’s not), there are historical precedents for what people are willing to pay for things too. Enter the contentiousness of the “valuation” debate. How much are you willing to pay to not lose money?

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 2.12-2.31%

SPX 1

RUT 1057-1127

Nikkei 149

VIX 14.34-28.05

WTI Oil 79.79-81.84

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer