TODAY’S S&P 500 SET-UP – October 24, 2014

As we look at today's setup for the S&P 500, the range is 128 points or 5.94% downside to 1835 and 0.62% upside to 1963.

SECTOR PERFORMANCE

EQUITY SENTIMENT:

CREDIT/ECONOMIC MARKET LOOK:

- YIELD CURVE: 1.87 from 1.89

- VIX closed at 16.53 1 day percent change of -7.50%

MACRO DATA POINTS (Bloomberg Estimates):

- 10am: New Home Sales, Sept., est. 470k (prior 504k)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Senate, House out of session

- 9:30am: House Oversight hearing led by Chairman Darrell Issa, R-Calif., on U.S. response to Ebola

- 9:40am: EPA Administratior Gina McCarthy delivers keynote remarks on “The Future of Energy & Our Environment”

- U.S. ELECTION WRAP: N.C. ‘Political Hate’; Outlook in Arkansas

WHAT TO WATCH:

- New York Man Diagnosed With Ebola as Authorities Track Movements

- Amazon Faces Season of Worsts as Losses Mount Before Holidays

- Sony, Apple to Introduce Large Tablets in 1Q 2015: DigiTimes

- Google Said to Buy Six Silicon Valley Buildings for $585m

- Toyota Sells Tesla Shares as Joint Electric RAV4 Project Ending

- Lockheed, Pentagon Reach $4b Deal on F-35 Jets: Reuters

- AMC Networks Pays $200m for 49.9% BBC America Stake

- Occidental CEO Sees Lower Drilling Fees If Oil Slump Continues

- RealPage Approached by at Least 2 PE Groups, FT Says

- Amtrak Weighs Selling Land for Development in 5 U.S. Cities

- Goldman, Inner Circle Hired by NBA’s Atlanta Hawks to Sell Team

- Regulators Ramp Up Bond Fund Exams in Response to Price Swings

- Swiss Banks Urge U.S. to Amend Demands in Tax Amnesty Deals

- ECB Vies for Third Time Lucky on Stress Tests as New Role Dawns

- U.K. Economic Growth Slows as Headwinds to Recovery Increase

- Actavis CEO Saunders Has $70b in Deals From Which to Choose

- Billionaire Fredriksen to Make Mandatory Bid for Flex LNG

- BASF Cuts 2015 Goals as Delayed European Growth Hurts Demand

- Chiquita Brands holds special shareholder meeting

- Fed, ECB Tests, U.S. GDP, Facebook: Week Ahead Oct. 25-Nov. 1

EARNINGS:

- Aaron’s (AAN) 7am, $0.37

- Avery Dennison (AVY) 8:30am, $0.74

- Bristol-Myers Squibb (BMY) 7:30am, $0.42 - Preview

- Cabot Oil & Gas (COG) 7:30am, $0.21 - Preview

- Colgate-Palmolive (CL) 7am, $0.75 - Preview

- Delphi Automotive (DLPH) 7am, $1.13

- DTE Energy (DTE) 7:15am, $1.05

- First Niagara Finl (FNFG) 7:15am, $0.18

- FLIR Systems (FLIR) 7:30am, $0.35

- Ford Motor (F) 7am, $0.19 - Preview

- IDEXX Laboratories (IDXX) 7am, $0.86

- ImmunoGen (IMGN) 6:30am, ($0.15)

- Lear Corp (LEA) 7am, $1.88

- LifePoint Hospitals (LPNT) 7am, $0.74

- LyondellBasell (LYB) 6:50am, $2.30

- Moody’s Corp (MCO) 7am, $0.90

- NASDAQ OMX (NDAQ) 7am, $0.70

- National Penn Bancshares (NPBC) 6:38am, $0.18

- Omnicare (OCR) 7:30am, $0.92

- Procter & Gamble (PG) 7am, $1.07 - Preview

- State Street (STT) 7:12am, $1.21

- TCF Financial (TCB) 8am, $0.30

- United Parcel Service (UPS) 7:45am, $1.28 - Preview

- Ventas (VTR) 7:15am, $0.45 - Preview

- WABCO Holdings (WBC) 6:30am, $1.41

- Wyndham Worldwide (WYN) 6:30am, $1.63

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- WTI Set for Fourth Weekly Drop as Saudi Policy Seen Unchanged

- Iron Ore Glut Spurring Slump in China Output, Goldman Sachs Says

- Gold Trades Near One-Week Low as Investors Assess U.S. Economy

- Aluminum Leads Metals Declines as China House-Price Drop Widens

- Glasenberg’s Iron Barbs Blunted by Coal Expansion: Commodities

- Soybeans Rise on Signs of Increasing Demand for U.S. Exports

- Romania’s Farmland Costing Fraction of U.K. Attracts Investments

- Rebar Pares Weekly Loss on Bets Mills to Cut Output During APEC

- Wheat Crop Seen Falling Short in Australia on Frost, Hail Damage

- Weak El Nino Seen Evolving by Year-End as Sea Warmer Than Usual

- Don’t Assume Saudi Supply Drop Was Move to Bolster Oil Price

- Vale Coming of Age as a Nickel Heavyweight Just as Prices Plunge

- Gold Traders Bullish a Fourth Week on Physical Demand to Economy

- MORE: China’s Copper Output Climbs to Record High in September

CURRENCIES

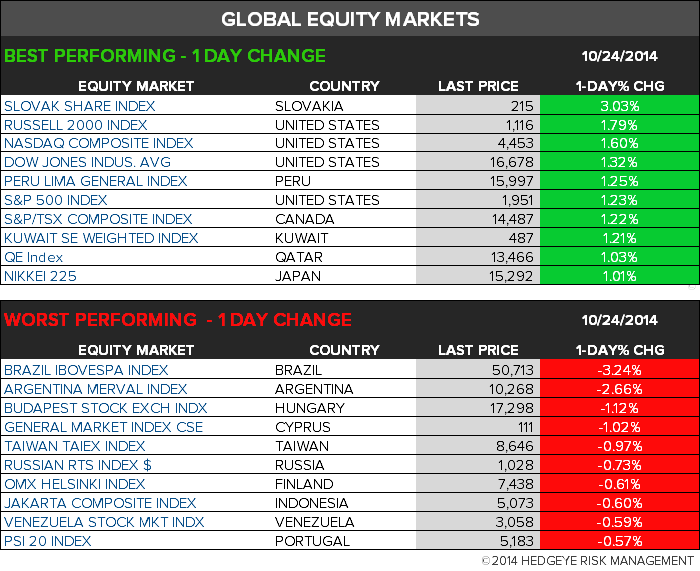

GLOBAL PERFORMANCE

EUROPEAN MARKETS

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team