Overview

The next major data point for CAT shareholders is the January 2015 EPS guidance with the 4Q 2014 report. The 2015 sales guidance and other details in today’s release suggest we should see downward 2015 revisions. The drivers of the 3Q beat are unlikely to be sustainable.

A pre-buy in E&T ahead of 2015 emissions regulation on very large engines (e.g. gensets and locomotives) and a sizeable year-on-year inventory swing appear to have been major contributors. As for the E&T pre-buy, a 33% sales gain in North America, where the emissions regulations are pending, sticks out. Backlog was sequentially higher, but on an “early order” incentive program and reciprocating engines orders. Neither of those would be positive for 2015, as early order programs usually involve discounting and reciprocating engine orders may relate to the pre-buy, which pulls demand forward.

While the headlines for 3Q 2014 are positive and management has done a good job of delivering results this year, we expect CAT shares to trade on what happens with the 2015 outlook going forward. Management may be starting to nudge 2015 expectations lower.

Key Takeaways

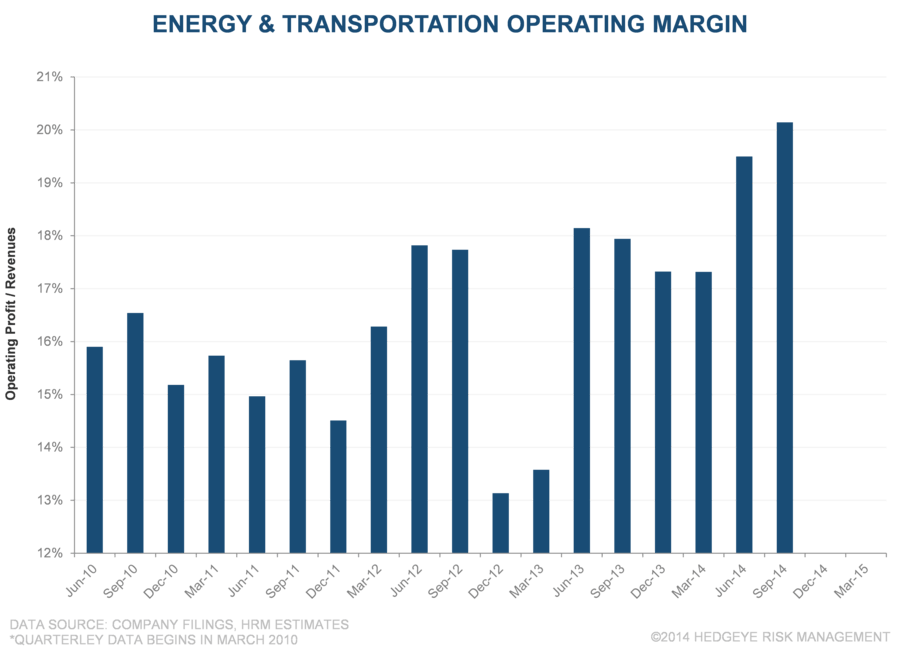

- E&T Pre-Buy Seems Pretty Obvious: Should investors extrapolate Energy & Transportation (E&T) segment’s performance into 2015? We think it is partly related to a pre-buy ahead of 2015 Tier 4 Final emissions regulations. North America’s rapid sales growth is a noteworthy hint, since that is the geographic region with new emissions regulations in 2015. Record margins also match a pre-buy, and are unlikely to be sustained in 2015. 2015 looks set to have a post pre-buy bust in North America, potentially amid weaker oil & gas demand.

- Sequential CAT Inventory Build: At the company level, CAT built inventory from 2Q 2014 to 3Q 2014 ($13,055 mil in 2Q 2014 to $13,328 mil in 3Q 2014) vs. a destock in the year ago period ($13,889 mil at 2Q 2013 to $13,392 mil in 3Q 2013). The comparison adds to the lower dealer destock, which was $200 million less of a draw vs. the year ago period. In total, dealer and company inventories had a combined swing of nearly $1 billion vs. 3Q 2013, by our estimates, which likely had a meaningful impact on production costs.

- Resource Industries Competitive Pricing: RI continued to struggle in 3Q 2014, largely consistent with expectations. Two comments in the release are worth noting, however. First, CAT noted that “Price realization was unfavorable primarily due to an increasingly competitive pricing environment.” The language suggests pricing pressure is ongoing, which is consistent with our understanding. Second, we would also note that dealer inventory was a “less significant” headwind that in the year-ago period. Combined with what may have been CAT level inventory gains, underproduction may have been less of a headwind. The cessation of underproduction has been expected to improve RI margins, but didn’t seem to matter this quarter.

- Construction Industries (CI) Margins Trending Lower From Record Levels: While we expect CI to remain a relatively strong performer for CAT in 2015, margins have trended lower without large dealer inventory builds. We suspect margins vs. the year ago period benefited from CAT’s own sequential inventory build.

Upshot

CAT investors should increasingly focus on 2015 expectations, which management seems to be pushing lower. Initial 2015 sales guidance and evidence of a Tier 4 pre-buy is not a favorable set-up, 3Q 2014 beat or not.