At around this time last week, we were staring at the associated market impact of the US Dollar being that Ball Underwater that was released to the upside. As the Buck broke-out, equities broke down (taking the SP500 down for a -3.5% correction in 4-days).

Today, we’re seeing quite the opposite. As global risk managers sell that Dollar back down to new YTD lows (down -0.93% to $77.30), the REFLATION trade is back! (Energy, XLE, and Basic Materials, XLB, are the 2 best performing sectors in our 9 S&P Sector study, trading +3% and 1.4% on the day, respectively).

Gold is trading > $1000/oz. Oil is trading straight back up above its immediate term TRADE line at $71.12/barrel. Copper is making new YTD highs.

Dollar down = Ball Underwater. As simple as this inverse correlation sounds is as simple as simple does.

After doing a lot of covering/buying on Wednesday of last week, I have been doing a lot of nothing for the last few days. Why? Well, A) I get the fundamental short case against the US Dollar (its once again broken across all 3 of our investment durations) and B) I’m happy watching one of the 24 stocks and/or ETFs we are long in the virtual portfolio find this last gasp of air.

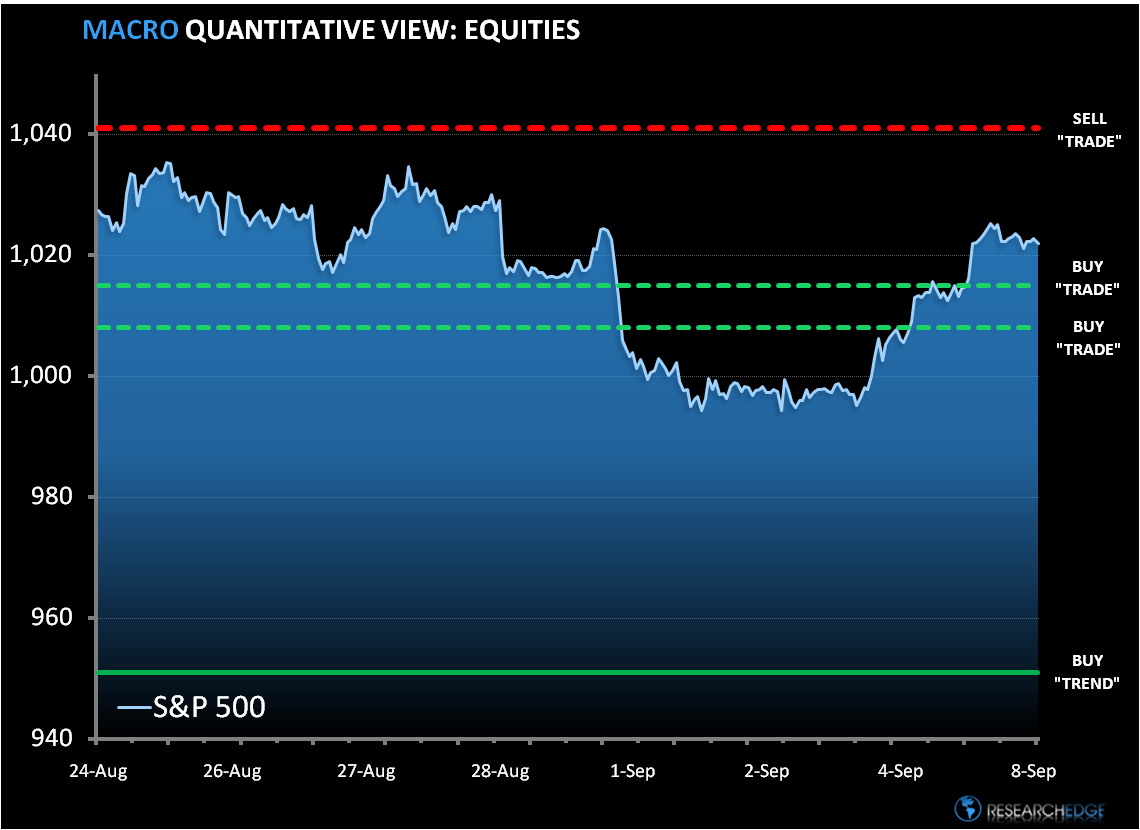

Where does the air run out of the REFLATION trade? I’m sticking with the high-side of what we called our Range Rover line (updated 5 weeks ago at 1041 on the SPX).

My newly established lines of immediate term support for the SP500 are 1015 and 1008 (dotted green lines in the chart below). Intermediate term TREND support is now 952.

KM

Keith R. McCullough

Chief Executive Officer